A war on the other side of the planet has been quietly setting the price of your next mortgage payment in DFW and this week the most important number in that whole equation finally moved. The United States and Iran reached a framework deal to end the war and reopen the Strait of Hormuz, with the signing scheduled for Friday, June 19 in Geneva, according to NBC News. The instant the news hit, oil fell more than four percent, with West Texas Intermediate sliding to roughly $80 and Brent to around $83, the lowest levels since early March. That drop is the first link in a chain that runs straight to your rate lock.

If this deal holds, it is the most realistic path to lower mortgage rates we have seen all year, and North Texas is positioned to capture that relief faster than almost any market in the country. The money is not made by reacting to the headline. It’s made by being positioned before the market finishes pricing it in. Most of the market saw the words “Iran deal” and scrolled right past them. I am going to show you why and what they missed.

Understand the deal before anyone tells you what it means

The agreement is a framework that extends the ceasefire sixty days and commits Iran to reopen the strait, with the U.S. naval blockade set to lift on signing, per CNN. Roughly twenty percent of the world’s oil moves through that one narrow waterway, according to the U.S. Energy Information Administration, so when the war effectively closed it, crude ran up more than forty percent on the year and Brent touched nearly $120 at the peak. Reopening it reverses the pressure that has been feeding U.S. inflation for months.

Here’s the caveat: The deal is a framework, not a guaranteed peace. The signing is only scheduled, it’s not done. Iran has already cast doubt on the timing. The ceasefire that came before this one was violated by both sides. Oil is still moving at roughly half of pre-war volume through escorted convoys, and the analysts who trade this for a living think the new normal may settle at sixty to seventy percent of where it was rather than a full return. Any one of those cracks can stall the relief, so we position around the opportunity. We don’t bet the house on it.

The Chain From Hormuz To Your Interest Rate

This is the part that lands in your living room, and it is the part the surface level news coverage never connects. Oil is an inflation input. When energy climbs, the cost of producing and moving nearly everything climbs with it, which is why May’s Consumer Price Index came in at 4.2 percent, the hottest reading in three years and more than double the Federal Reserve’s two percent target, per Bankrate’s reporting. Energy did most of that damage, accounting for more than sixty percent of the monthly jump. That inflation spike is the entire reason the rate cuts that looked likely back in the spring evaporated.

Let’s look at this a little deeper. Core inflation, the measure that strips out food and energy, rose just two-tenths of a percent on the month, per Kiplinger. The damage was almost entirely energy. A price shock built on oil can reverse as fast as oil does, while one baked into wages and rent does not. This was, thankfully, the kind of price shock that unwinds quickly, and the Iran deal is exactly the thing that can unwind it.

The mortgage math followed the news in lockstep. The thirty-year fixed touched a 2026 low near 6.09 percent earlier this year and briefly slipped under six percent, then climbed back above 6.5 percent as the war fed inflation, according to Bankrate. The Federal Reserve meets June 16 and 17 and is widely expected to hold, per U.S. News. It’s important to remember, The Fed does not set your mortgage rate directly. The bond market does, and the bond market moves on inflation expectations. The Federal Reserve’s own research puts the relationship at almost four-tenths of a percentage point on headline inflation for every ten percent move in the price of oil. Run that math in reverse on a sustained drop in crude, and the path back toward lower rates starts to open. Cooler inflation is the only door that leads there, and cheaper oil is the fastest way through it.

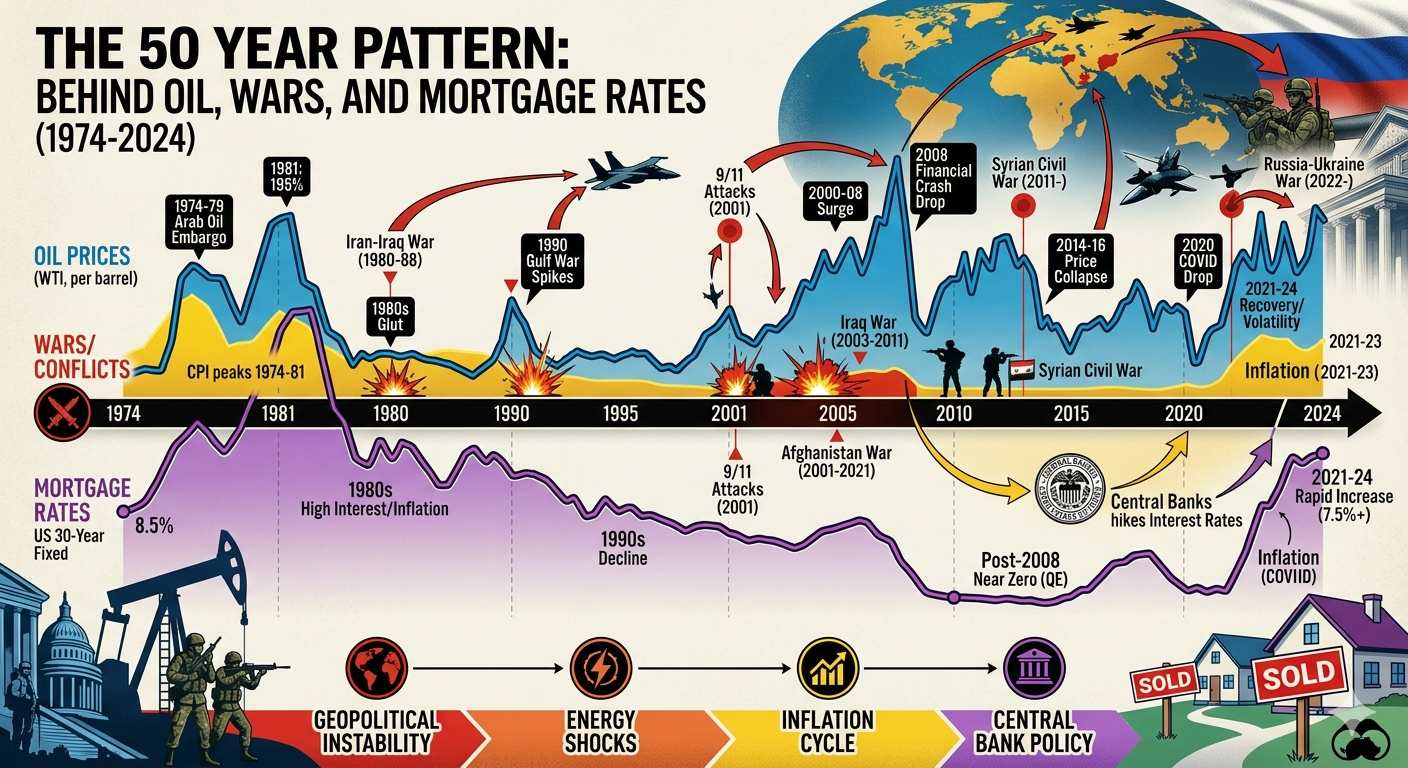

The Fifty-Year Pattern Behind Oil Wars And Mortgage Rates

If this all feels theoretical, history makes it concrete, because we have indeed run this experiment before. Every major oil shock of the last half century has moved through the same sequence, oil → inflation → the Fed → mortgage rates, and the housing market felt every one of them.

Start in 1973. When the Yom Kippur War triggered an Arab oil embargo and crude quadrupled, U.S. inflation climbed to 12.3 percent by 1974 from 3.4 percent two years earlier, and the Federal Reserve pushed its benchmark from under six percent to twelve. Mortgage rates tracked the damage, climbing from around 7.3 percent at the start of the decade to 12.9 percent by 1979. Then came the second hit. The 1979 Iranian Revolution pulled nearly seven percent of world oil production off the market, inflation reignited, and Paul Volcker drove rates to twenty percent by 1980. Thirty-year mortgages touched eighteen percent. A war in the Middle East priced a generation of Americans out of the homes they wanted.

You don’t have to reach very far back to see the pattern. In 2022, Russia’s invasion of Ukraine sent crude from $92.77 a barrel to a peak of $123.64 in twelve days, energy prices across developed economies jumped roughly eighteen percent, and inflation ran to a four-decade high. Mortgage rates did exactly what the chain predicts, more than doubling across the year from near three percent to above seven. Same sequence, fifty years apart.

Here is the part that matters for right now, and it is the reason I am not panicking and neither should you. The 1970s were brutal because the shocks were prolonged and supply stayed broken for years, made worse by loose policy that let inflation dig into wages. A shock that resolves quickly never gets the chance to do that kind of damage. The Iran deal, if the strait reopens on schedule, is the opposite of a 1970s embargo. It’s the fast resolution, not the prolonged siege, and that is exactly why the speed of this signing matters more than the drama around it.

What A Rate Break Would Do To The National Market

The national housing market is not frozen because demand vanished. It is frozen because affordability broke, and that is a very different problem with a very different fix. Existing-home sales are crawling at roughly a 4.17 million annual pace, with the median price near $429,300 and inventory around four and a half months, per the National Association of Realtors. That same group had projected a fourteen percent jump in sales for 2026 on the expectation of cheaper money, then cut the forecast to roughly four percent once the war drove rates back up. Read that the right way. The buyers did not leave. They got priced to the sideline, and they are standing there waiting on one number to move. A market like that does not drift lower when rates fall. It thaws, and it thaws fast, because the demand was never gone. It was just holding its breath.

Why North Texas Is The Most Leveraged Housing Market In The Country To This Exact Event

Now let’s take the national headline somewhere the cable segments won’t, because this is where the real intelligence lives. North Texas is not an average housing market right now. It is a market that has been held together by builder rate buydowns. Roughly seventy percent of new-home sales across DFW already carry a buydown or structured incentive that puts buyers near 5.5 percent, per HousingWire, a full point under the open-market rate that resale buyers are still paying. That sub-six-percent number lives in the new-construction segment specifically, not the metro resale median, and the distinction matters the moment you run your own deal. Builders are doing that because they are sitting on real inventory.

North Texas closed 2025 with more than 12,300 finished vacant homes and a developed-lot supply measured in years, not months. Housing supply is often measured in months of inventory, but builders are now staring down years of inventory. Resale supply has expanded to roughly three to four months, days on market have stretched toward sixty, and the demand engine underneath all of it is still running, with the metro adding more than 24,000 net new jobs in a single quarter and corporate relocations still landing.

The Ellis County corridor is where a lot of that new supply is going vertical. Builders across Waxahachie, Midlothian, Red Oak, and Ennis have been competing for the same relocation buyer with some of the most aggressive incentive packages in the metro. Which means the leverage I am describing is not only impacting central DFW, it’s also sitting on lots forty minutes south of downtown.

Put those pieces together and the picture sharpens fast. We have motivated builders, expanded inventory, major incentives already on the table, with all of it sitting on top of mortgage rates that have been propped up by a war premium. Strip the war premium out of oil, let oil pull the premium out of inflation, and the rate relief lands on a market that is already primed to hand buyers the advantage. That’s leverage stacked on leverage, offering advantages many thin-inventory coastal markets with no builder incentives don’t have access to.

The Move: Five Steps Ahead

Here is what the prepared buyer does this week, while the rest of the market waits for a headline to hand them permission.

If you are buying new construction, lock the builder’s buydown now. That incentive is real today, Iran signing or not, and a subsidized rate near 5.5 percent beats every published 2026 forecast for the open market. If broader rates fall later, you refinance into the lower number and keep the home you already negotiated on your terms.

If you’re a buyer sitting on the sidelines waiting for the perfect rate, understand the trap you are walking into. When rates fall, the sidelined demand comes back with you. The National Association of Realtors estimates a return toward a six percent rate would put the median-priced home back in reach for roughly 5.5 million more households, about 1.6 million of them renters. Those households are your competition, and they will reappear the moment financing gets cheaper. The window where you hold both the incentive and the negotiating leverage is open right now, but it will not stay open after the news confirms what you were waiting for.

If you’re a seller, watch the rate path like it is your listing’s heartbeat, because that is exactly what it is. The resale environment improves the instant financing gets cheaper, since lower rates expand what buyers can pay and pull the hesitant ones off the fence. Honesty cuts both ways, so play the other side too. If the signing slips and oil spikes again, rates may hold high or even climb. At that point you’re selling into a slower market where builders are still buying down rates you can’t match. Either way the preparation is identical. Be ready before the demand returns, not flat-footed when the picture turns. Price to today’s market, present the home like it is new construction, and be positioned to catch the wave the moment it forms.

The Benchmarks That Tell You Which Way This Breaks

You don’t have to guess, and you don’t have to wait for a reporter to tell you what happened. Savvy buyers will watch these markers, because they move before the headlines catch up to them.

The bullish case, the one that says the relief is real, looks like this. The Friday signing actually happens. Oil holds at or below eighty dollars. The next inflation report shows the decline coming out of the energy line. The thirty-year fixed breaks below 6.25 percent and keeps trending down. When you see those line up, the window is open, and the buyers who locked their deals early will be the ones holding the winning hand.

The bearish case, the one that says stay patient and keep your leverage, looks like the opposite. The signing slips or collapses. Oil spikes back above one hundred dollars. Inflation re-accelerates instead of cooling. The Fed starts hinting at a hike rather than a cut. When you see those and rates stay high or start climbing, builder incentives will stick around and perhaps get even more enticing. The negotiating power will unfortunately stay right where it is, in the buyer’s hands. That is not a disaster though, it is simply the alternative game plan, and you will know which one you need to be running because you watched the right four numbers instead of the noise.

If You Are Moving to North Texas From Out Of State, The Math Is Different For You

A specific word for the relocation buyers, because a large share of the people I work with are moving in from Utah, California, Washington, and Colorado, and a rate move touches your situation quite differently than a local move-up buyer’s.

When you relocate, you are usually running two transactions at once, selling there while buying here, and the rate environment hits both ends. Here is the leverage most out-of-state buyers miss. The equity you built in a California or Colorado home equates to serious buying power in North Texas, where the same dollars stretch dramatically further. That advantage exists today, at current rates, before any relief arrives. You do not have to wait on the Fed to win on price-per-square-foot when you are trading a coastal or mountain market for DFW or Ellis County.

What the Iran deal adds is a second potential tailwind on the financing side. If rates ease the way the chain suggests they could, your payment on your North Texas purchase improves while your home back home sells into buyers who are feeling that same relief. The risk runs the other way too, and I will say it plainly. If the deal fails and rates climb, your sale back home gets harder at the very moment your purchase here gets more expensive. That is the double squeeze, and moving while builder incentives are rich and inventory is wide is how you sidestep it.

The play for relocation buyers is the same as for everyone else, just with more riding on the timing. Get your financing modeled now, lock a builder incentive while the overhang lasts, and treat any future rate drop as a refinance bonus rather than a reason to delay a move you are already committed to making. For the full out-of-state breakdown, I keep a running North Texas relocation guide for buyers making exactly this move.

FAQ: Iran Deal and Mortgage Rates

Will the Iran deal lower my mortgage rate?

Not directly and definitely not instantly. The deal will lower oil prices, which will ease inflation, which will give the bond market and the Federal Reserve room to bring rates down over time. As of mid-June 2026 the thirty-year fixed sits around 6.5 percent. If the deal holds and oil stays down, that number has room to fall later in 2026.

How does reopening the Strait of Hormuz affect oil prices?

Roughly twenty percent of the world’s oil passes through that one waterway. The war effectively closed it and pushed crude up more than forty percent on the year. Once the new broke about a possible deal, oil fell to its lowest level since early March, near eighty dollars a barrel.

Why do oil prices move mortgage rates at all?

Oil is an inflation input. The Federal Reserve’s own research shows a ten percent move in oil can shift headline inflation by almost four-tenths of a percentage point. Mortgage rates follow inflation expectations through the bond market, so cheaper oil tends to mean lower rates over time.

Is now a good time to buy a home in North Texas?

For buyers who can act, the current setup is unusually favorable. Builders are sitting on a large inventory of finished vacant homes and offering aggressive buydowns near 5.5 percent, while resale supply has loosened to three to four months. That leverage favors buyers right now and tends to shrink once rates fall and competition returns.

Should I wait for mortgage rates to drop before buying?

Waiting carries a hidden cost. When rates fall, sidelined demand comes back. The National Association of Realtors estimates a six percent rate will bring roughly 5.5 million more households back into the market, which means more competition and less negotiating room. The common strategy is to buy now and refinance later if rates drop.

What is a builder rate buydown?

It is an incentive where the builder pays to lower your interest rate, often by a point or more, sometimes permanently. In DFW, roughly seventy percent of new-home sales currently include a buydown or similar incentive, putting many buyers near 5.5 percent while the open market sits higher.

Will home prices in DFW go up if rates fall?

Lower rates expand buyer purchasing power, which historically supports prices and speeds up sales rather than dropping them. North Texas is projected for modest appreciation in 2026, and a rate-driven return of demand would more likely firm prices than soften them.

What happens to rates if the Iran deal falls apart?

The oil relief reverses. If crude spikes back above one hundred dollars and inflation re-accelerates, rates stay high or climb, and the Fed could even weigh a rate hike. In that scenario builder incentives will stick around, possibly get stronger and buyer leverage holds, which is why positioning to win either way beats betting on a single outcome.

When is the Federal Reserve’s next meeting?

The Fed meets June 16 and 17, 2026 and is widely expected to hold rates steady. The path to future cuts is predicated on cooler inflation, which is exactly what a sustained oil decline from the deal would produce.

Does the Iran deal affect Ellis County and Waxahachie specifically?

Arguably more than the DFW average. Ellis County is absorbing heavy new construction across Waxahachie, Midlothian, Red Oak, and Ennis, where builder incentives have been among the most aggressive in the metro. That positions local buyers especially well to benefit if rate relief arrives.

How fast could mortgage rates actually come down?

History says energy-driven shocks can unwind quickly once supply normalizes, unlike the prolonged crises of the 1970s. The bond market tends to move ahead of the Fed, so the thirty-year fixed could ease before any official Fed level rate cut, provided inflation reports confirm the oil decline is real.

The whole game fits in one sentence. The opportunity is never in reacting to the news. It is in being positioned before the market finishes pricing it in. A signing in Geneva is not a home affordability story to most people. But, to the prepared buyer and the ready seller, it is the only story that matters this month.

Want the full read on where North Texas is heading this year? I laid out the complete picture in the Insider’s 2026 Housing Market Forecast, and I update my take the moment a development like this one breaks. When you are ready to run your own numbers and model both the buydown and the refinance scenario, talk to a lender who knows this market cold:

Andrew Bryan — Miramar Mortgage | andrewthelender.com | Jennifer Nelson — Eustis Mortgage | eustismortgage.com | Taylor Fruge — Lower Mortgage | lower.com

I recommend these lenders based on their expertise and service. I do not receive compensation for referrals.

Bobby Franklin, REALTOR® | Legacy Realty Group – Leslie Majors Team

📲 214-228-0003 | northtexasmarketinsider.com

Market figures referenced here are current as of June 15, 2026 and reflect a developing news event, so they will move as the situation evolves. This article is market commentary, not financial, legal, or investment advice. Bobby Franklin and North Texas Market Insider are committed to equal opportunity in housing in full accordance with the Fair Housing Act.