By Bobby Franklin, REALTOR® | North Texas Market Insider™ | Legacy Realty Group – Leslie Majors Team

Serving Ellis County, DFW & Greater North Texas | 214-228-0003 | northtexasmarketinsider.com

The headline writers certainly had their fun in May with the multitude of global and national events. Mortgage rates climbed for most of the month, and every doom account on your feed treated it like the sky was falling on housing. Here is what they missed, because they always miss it. The rate move had almost nothing to do with housing. While the country watched rates keep climbing on a chart, North Texas buyers quietly picked up the most negotiating leverage this market has handed them in years.

That is the real story of May 2026, and it’s the opposite of the one you were sold. Rates went up because of a war in the Middle East, not because of anything happening in Waxahachie or Midlothian or Red Oak. Right here in the I-35E corridor, sales volume actually rose, inventory stayed healthy, sellers started trimming their prices, and the biggest names in the global economy kept pouring billions into the ground south of Dallas. This is what a buyer’s window looks like before everyone else notices it has opened.

Here is the one idea to hold onto through everything that follows. In this market, buyer’s leverage is temporary while the corridor’s growth is permanent, and the gap between those two is your window of opportunity.

Let me walk you through exactly what happened, why it happened, and the moves that put you five steps ahead of everyone still reacting to the headline.

What Actually Moved Rates in May, and Why It Had Nothing to Do With Your Neighborhood

Let’s start with the number everyone was watching. The Freddie Mac 30-year fixed rate opened the month at 6.37% on May 7, eased a hair to 6.36% on May 14, then jumped to 6.51% on May 21 and finished at 6.53% on May 28. That is the highest the 30-year has sat since last August. Daily lender pricing ran even hotter, with some quotes brushing 6.68% around May 20, the steepest in roughly ten months.

So far that sounds like bad news, and the panic merchants ran with it. Here is the part they refuse to explain. A year ago that same Freddie Mac rate was sitting near 6.89%. You are buying at a lower rate today than buyers were a year ago, in a market with far more inventory and far more seller flexibility. The headline says rates are up. The context says you are still better positioned than the person who bought your neighbor’s house twelve months ago.

Now the question that actually matters. Why did rates climb at all when the housing market itself is soft? Because mortgage rates don’t take their orders from home sales. They follow the 10-year Treasury yield, and in May the Treasury market was reacting to one thing above all others: the ongoing war between the United States, Israel, and Iran. The conflict that began at the end of February kept the Strait of Hormuz in play, kept oil prices elevated near triple digits, and pushed the national gas average to roughly $4.50 a gallon. That energy shock lit a fire under inflation expectations, and the 30-year Treasury spiked to 5.127% on May 15, its highest reading since 2007. When the long bond moves like that, your mortgage rate moves with it. Redfin’s chief economist Chen Zhao put the cause plainly, noting that the Iran war is still driving rates more than economic data.

This is the exact dynamic I have been telling North Texas sellers and buyers about for months, and it is why I keep separating the Federal Reserve from your actual mortgage rate. They are two different animals. I broke that down in detail when the Fed paused in March, and May proved the point all over again. The Fed’s benchmark rate did not move your mortgage in May. A war and a strained oil market did.

Speaking of the Fed, May brought a leadership change that matters for the rest of the year. Kevin Warsh was confirmed as the new Fed Chair on May 13 in a 54-to-45 vote, the closest in modern history. He took the chair when Jerome Powell’s term expired on May 15. The minutes from the prior Fed meeting, released during May, showed a committee leaning hawkish, with a majority open to tightening policy further if inflation stays stubborn, and several officials openly floating the idea of hikes rather than cuts. With April inflation running at 3.8% on both the consumer and the Fed’s preferred gauge, the hottest in nearly three years, the market quietly erased its bets on rate cuts this year. Warsh’s first meeting lands June 16 and 17. That is the next domino, and we will be watching it very closely.

The takeaway is simple. The rate story of May was a geopolitical story wearing a housing costume. Strip off the costume and you find a market that is still functioning, still transacting, and still tilting toward the prepared buyer.

The National Picture: Soft, Not Sinking

Zoom out to the whole country and the data tells a consistent story. The market is soft, but is not collapsing. There is a meaningful difference, and the people conflating the two are going to miss the opportunity sitting in plain sight.

Builder confidence rose in May. The NAHB/Wells Fargo Housing Market Index climbed three points to 37, bouncing off April’s seven-month low. That said, 37 is still well under the neutral mark of 50, and it has been below 50 for 25 straight months. Builders are coping the way smart operators always cope with a slow market: they are buying down rates and sweetening deals. In May, 61% of builders offered sales incentives, the fourteenth straight month at or above that level, and roughly a third cut prices outright, with the average cut running about 6%. NAHB Chairman Bill Owens tied the softness directly to higher mortgage rates, rising gas prices, and the economic uncertainty radiating out of the war.

Sales data released during the month showed the same split-screen. Existing-home sales nudged up 0.2% in the report that landed May 11, with the national median holding around $417,700. New-home sales, reported on May 28, slid 6.2% lower. Home prices nationally have nearly flatlined, with the latest Case-Shiller reading showing the slowest annual growth since 2023 and the first monthly dip in eight months. The encouraging signal buried under the noise: pending home sales rose for a third consecutive month. Freddie Mac’s chief economist Sam Khater called that out directly on May 28, observing that pending home sales have increased three months in a row, a sign of buyers coiled and ready to move the moment rates give them an opening.

The structural backdrop is the most important piece, and it is the reason I keep telling people to ignore the crash chatter. The country is still short of housing. Oxford Economics published an affordability outlook on May 27 estimating the nation is missing more than two million units and warning that affordability will not normalize for the better part of a decade. A market with a genuine supply shortage does not crash. It grinds, it rebalances, and it rewards the buyers who show up while everyone else is frozen. I laid out the full case for why this housing market is not going to crash, and nothing in May changed that thesis. If anything, May reinforced it.

The divergence inside the national market is the detail that matters most for us, and almost nobody is explaining it correctly. The country is not one housing market. It is dozens of them moving in different directions at the same time. In the inventory-starved Midwest and Northeast, where almost nothing is listed for sale, prices kept climbing right through the spring because buyers had no choice but to compete for scraps. Chicago, Cleveland, and much of the Northeast corridor are still posting solid annual price gains. The Sun Belt is the mirror image. Texas, Florida, Arizona, and the Mountain West all built aggressively coming out of the pandemic, inventory has caught up to demand and in places surpassed it, and prices have softened as a direct result. That softening is not weakness. It is supply doing exactly what supply is supposed to do, which is hand pricing power back to the buyer.

DFW sits right in the heart of that Sun Belt rebalancing, and that is precisely why our market looks so different from the national headline. So when someone tells you that “the housing market” is doing one thing, the only correct response is to ask which market they mean. The answer in North Texas is its own story, and it’s a far better one for buyers than the national narrative would have you believe.

One more national data point sets up everything I am about to tell you about North Texas. Redfin’s tracking showed roughly 480,000 more sellers than buyers across the country, the textbook definition of a buyer’s market, with more than half of all sellers cutting their price in a handful of metros. Three of those metros sit in Texas. One of them is Dallas.

The DFW Reality: A Market Tilting Toward the Buyer

Here is where the national story becomes a local opportunity. Dallas-Fort Worth is not behaving like the inventory-starved Midwest, where prices are still climbing because there is nothing to buy. DFW has supply, and supply changes everything.

The MetroTex Association of REALTORS report released May 20 showed North Texas closed sales rose 8% year over year, with 8,240 single-family homes sold. The metro median price came in at $395,000, essentially flat at down about 1% from a year ago. Active listings sat at 29,578, supply registered at 4.1 months, and the typical home took 61 days to sell, up 5% from last year. Sellers received roughly 95.3% of their original list price, meaning the gap between asking and closing is real and growing.

The Texas Real Estate Research Center backed this up in its analysis released May 29. Across the DFW-Arlington market, prices were down a modest 0.8% year over year, the most contained decline of any major Texas metro, while sales climbed 4.7% and active inventory rose 3.4%. The detail that should grab every seller by the collar: the typical North Texas seller cut about $15,000, or 3.6%, off the initial asking price before the home went under contract.

Read those two reports together and the picture sharpens. Sales volume is up. Prices are flat to slightly soft. Inventory is comfortable. Homes are taking two months to move. That is not a crash. A crash means nobody is buying. In DFW, more people bought this spring than last spring. What we have is a rebalancing, a market exhaling after years of holding its breath, handing the advantage back to the buyer for the first time in a long time. You can watch these shifts unfold in real time on my live DFW market data page, which pulls current MLS numbers for Dallas, Ellis, Johnson, Hill, and McLennan counties.

Let me put numbers to what “buyer’s market” actually means on the ground, because the phrase gets thrown around without anyone defining it. Four months of inventory means that if no new homes came on the market, it would take four months to sell everything currently listed. A year of frenzy ran that number near one month, where buyers waived inspections and wrote offers over asking sight unseen. At four months, the buyer has room to breathe, time to think, and standing to negotiate. Sixty-one days on market means the average seller is waiting two full months for a contract, and every week a home sits is another week of leverage shifting toward whoever finally writes the offer. The 95.3% of original list price tells you the rest. Buyers are not paying asking anymore. They are paying less, and sellers are accepting it.

The smart read on DFW in May is not “prices are falling, be afraid.” The smart read is “the leverage just changed hands, and most people have not figured it out yet.”

But Make No Mistake, the Market Has Slowed

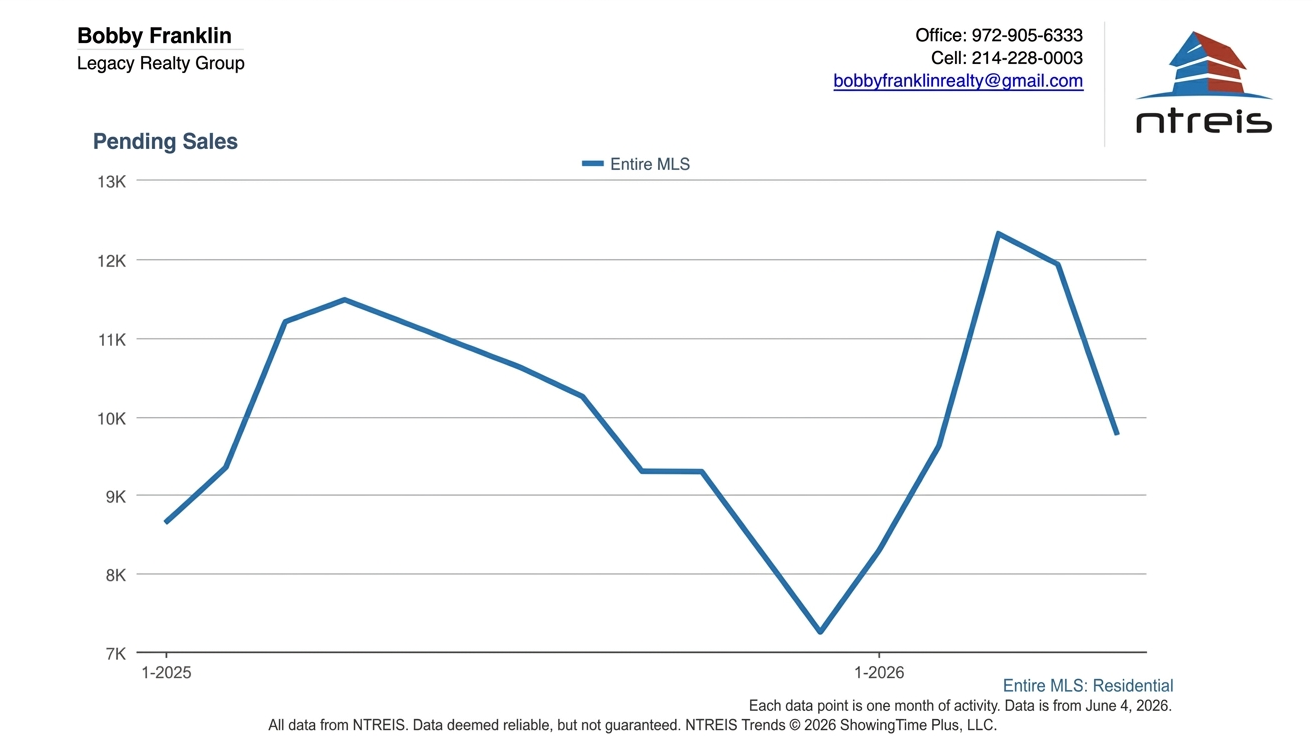

The clearest sign of that pressure is showing up in pending sales, the truest real-time read on buyer demand because it captures contracts being signed right now rather than deals that closed weeks ago. Across the metroplex, pending sales have fallen to 9,792 homes, the lowest level since February 2026 and a steep 20.56% drop from where they stood in March. That is not a number that wobbles on its own. It moves when buyers hesitate, and right now they are hesitating, weighed down by gas that ran past $4.50 a gallon at four-year highs and an inflation reading that climbed to 3.8% in April, the hottest in nearly three years. The independent MetroTex data tells the same story from a different angle, with pending sales down 6% year over year and homes now taking 61 days to sell. The people who build for a living see it too. NAHB Chairman Bill Owens put it plainly, noting that rising gas prices and economic uncertainty related to the war continue to dampen buyer demand.

I want to be careful with how I frame this, because the headline-chasers will take a number like that and scream collapse. This is not a collapse. It is a slowdown, and there is a real difference. Demand softening because buyers are catching their breath in the face of a war-driven affordability squeeze is a very different thing from a market with no buyers and no floor. The floor here is solid. The country is still short more than two million homes, our metro is still adding more than 300 new residents a day, and closings themselves held up just fine. What slowed is the pace of new contracts, not the long-term demand for a place to live in North Texas. The market took a breath when the war hit the gas pump, and the buyers who keep moving while everyone else waits for the exhale are the ones who will look smart a year from now.

What This Hands the Buyer Right Now

Let me be blunt, because softening this would do you a disservice. If you are a serious buyer in North Texas, this is the strongest position you have been able to negotiate from in years, and the window is open today.

Start with price. When more than half the sellers in your market are cutting their asking price and the typical home is sitting for two months, you are not the one under pressure. The seller is. That dynamic lets you negotiate on the sales price itself, on closing-cost credits, on repairs, and on the single most powerful tool in a high-rate environment: the rate buydown. This is not wishful thinking, it is what the data shows builders are already doing. Per the NAHB, 61% of builders offered sales incentives in May, and the average price cut ran about 6%. A builder-paid or seller-paid buydown can pull your effective rate meaningfully below the 6.53% headline for the early years of the loan, and that is what transforms your monthly payment while everyone else is still complaining about the sticker rate.

The mistake buyers make is showing up to this kind of market without their financing locked and loaded. Leverage means nothing if you cannot close. Before you negotiate a dollar, get fully pre-approved so you can move the moment the right home appears, and your offer carries the weight of a buyer who is ready. I work with three lenders who understand this market and structure these buydowns the right way:

Andrew Bryan – andrewthelender.com

Jennifer Nelson – eustismortgage.com

Taylor Fruge – lower.com

If land or new construction is on your radar, the leverage extends there too, and the long game in this corridor is land. I put together a complete walkthrough on purchasing land in North Texas that covers ag exemptions, utilities, and the corridor’s growth path, because the people buying dirt in the right spots right now are the ones who will look back in five years and realize they made an amazing investment.

No matter which corridor community you’re targeting, the same principle holds across the metro. The seller needs you more than you need any single house. Use that.

If You Are Moving to North Texas From Out of State, Read This Twice

A large share of the people I help are not moving across town. They are moving across the country, from California, Colorado, Washington, Arizona, and Utah, and a number of them are coming home from postings in Germany. If that describes you, the national context in this report is not abstract. It is the entire reason your move makes sense right now.

Here is the math that out-of-state buyers feel in their bones the moment they run it. The affordability gap between a coastal metro and North Texas is not a rounding error. It is life-changing. The national affordability picture sat deep in unaffordable territory in May, and the markets dragging that number down the hardest are the very coastal metros people are leaving in the first place. Texas is where the dollar still stretches. A household priced out of Seattle or the Bay Area looks at a $395,000 DFW median, a corridor full of brand-new construction, and a state with no income tax, and the decision starts making itself. You can frequently buy more home, on more land, with a lower monthly payment than you were carrying for a smaller place back west.

Then layer the timing on top of the math. You are arriving in a buyer’s market, with sellers actively cutting prices and builders handing out incentives, in a corridor absorbing billions of dollars in permanent investment. You are not chasing a hot market and praying you did not overpay. You are stepping into a market that just tilted in your favor, in the exact moment the long-term growth story is accelerating underneath you. That combination, genuine buyer leverage stacked on top of genuine structural growth, does not come around often, and it will not last once rates ease and the sideline buyers come flooding back.

The one piece of advice I give every relocating buyer is this. Do not let the rate headline you read in your current city make the decision for you. The number that matters is not the national average rate, it is the effective rate after a builder or seller buydown, against a Texas cost of living, on a home in a corridor that is being rebuilt around you. Run that full picture before you conclude anything. Most people who do are stunned at how far ahead the move puts them. If you want to understand a specific community before you ever board a plane, my city guides for Waxahachie, Midlothian, and Red Oak are built to give you the lay of the land from wherever you are sitting today.

The Seller Playbook: Price to Today, or Watch It Sit

Sellers, this section is the unfiltered truth, and I would rather you hear it from me than learn it the hard way after 90 days on market.

The market is still moving. Remember, 8% more homes closed this spring than last spring. People are buying. The homes that are selling, though, are the ones priced to what a buyer will actually pay in May 2026, not what your neighbor got in the frenzy of 2022. With the typical seller already conceding about $15,000 off the original ask and homes averaging 61 days to sell, the cost of overpricing is no longer a slow burn. It is a stalled listing, a stale calendar, and a string of price drops that signal weakness to every buyer’s agent in the metro.

The winning approach has not changed, it has just gotten more demanding. Price to the current comparable sales, not the aspirational ones. Present the home in move-in-ready condition, because buyers with leverage will punish anything that needs work. Be ready to offer the same concessions the builders are offering, including a rate buydown or covering closing costs, because that is what the competition across the street is doing. Most seller concessions in North Texas are going towards paying the buyers closing costs, which is typically 3% of the home value. I lay out the full framework in my guide to pricing strategies for North Texas sellers, and if you want the tactical prep list before you ever hit the market, my home sellers’ checklist walks you through it room by room.

Here is the reframe that separates the sellers who win from the ones who chase the market down. A correctly priced home in North Texas sells on time and near asking. An overpriced one does the opposite. It sits, it goes stale, and it funds its own price-drop spiral while the 61-day calendar punishes every week of denial. The 95.3% of original list price that realistic sellers are netting is not a tragedy, it is the reward for pricing to the market instead of fighting it. Price it right on day one and you skip the slow bleed entirely. The buyers are out there, give them a reason to choose your home over the three others they are weighing.

The Part Nobody on Your Feed Is Tracking: Ellis County’s Structural Boom

Now for the piece that makes everything above almost a footnote, because this is the intelligence that nobody else in this market is delivering, and it is the reason I am not the least bit worried about a soft spring market.

While the headlines obsessed over a quarter-point on the 30-year, the largest companies on earth kept writing nine and ten-figure checks for land and buildings in southern Dallas County and Ellis County. Construction is underway right now on Google’s fifth building at its Midlothian campus, an $880 million data center of roughly 288,000 square feet, with completion targeted for early 2027. That building is one piece of the $40 billion statewide investment Google announced in November, anchored right here in Midlothian, the company’s single largest commitment to any state in the country.

Data centers are only part of it. Healthcare is now following the rooftops. In mid-May, Baylor Scott & White’s Waxahachie medical center cleared a major structural milestone on a roughly $240 million campus expansion that adds 59 beds, a larger emergency department, more operating rooms, and intensive-care capacity, with the new six-story tower on track to open this fall. Hospitals do not expand by a quarter of a billion dollars in places they expect to shrink. They expand where the population is exploding, and Ellis County is exploding. Midlothian alone grew about 34% in five years.

The residential pipeline matches the commercial momentum. A 3,170-acre master-planned community approved in Waxahachie earlier this year will eventually bring more than 13,000 homes to the area, with buildout beginning later this year. The 5,200-acre South Creek Ranch development in Ferris is reshaping the southern end of the corridor, tied to I-45 and the future Loop 9 connector that will stitch the region together. Every one of these projects is a magnet for jobs, and every job is a future buyer.

Step back and see the whole board. Dallas-Fort Worth has led the entire nation in corporate headquarters relocations, drawing more than 100 since 2018. I am not going to pretend that momentum is still accelerating, because it is not. Site Selection magazine recently dropped DFW from first to fourth on its ranking of the best metros for headquarters, behind Nashville, Atlanta, and Charlotte, and the pace of relocations has cooled off its record highs. That is the honest picture, and I would rather you hear it from me than from an agent who only tells you the bullish half of the story. Here is why it does not change the thesis. Even off its peak, DFW remains a top-tier destination for capital, companies, and people, and the corridor I serve is precisely where that overflow is landing. A market does not need to be the undisputed number one to be the smartest place to own a home. It needs durable demand that outlasts any single year’s headlines, and this one has it in writing, in concrete, and in cranes on the skyline.

This is the five-steps-ahead read. Mortgage rates are reacting to a war that will eventually resolve, oil prices will eventually normalize and the Treasury market will settle at some point. Those are temporary forces. But the Data centers, hospitals, master-planned communities, and corporate relocations are permanent forces, and they are all pointing in the same direction to Ellis County. The floor under this corridor is rising while the short-term noise tells everyone to wait. The people who understand that distinction are the ones who buy now.

The Move That Puts You Five Steps Ahead

Pull it all together and the strategy almost writes itself.

Rates climbed in May because of a war, not because of housing, and they remain below where they sat a year ago. The national market is soft but structurally short of homes, which means a grind, not a crash. DFW has tipped into buyer-friendly territory, with rising sales, ample inventory, and sellers actively cutting prices. Underneath all of it, Ellis County is absorbing billions in permanent investment that will define property values here for the next decade.

So here is what the prepared buyer does. You move during the leverage window, because leverage windows close fast. The same Sam Khater data showing three straight months of rising pending sales is telling you that demand is coiled and waiting. The moment the Strait of Hormuz reopens or a durable ceasefire holds, oil should fall, the Treasury market will relax, rates will drift back down toward the high fives, and every buyer who was sitting on the sidelines will flood back in at once. When that happens, the price negotiations, the seller concessions, the builder buydowns, all of it evaporates. The advantage you have today is borrowed against tomorrow’s competition.

Here is what the smart seller does. You price to the market that exists in front of you now, not the one in your memory, and not the oen you hope for down the road. You let the genuine demand in this corridor do its work. The buyers are real and so are the relocations. Meet the market where it’s at and you win. Fight it and you fund your own price-drop spiral.

The market gave us a gift in May disguised as bad news. The headline scared the timid. The data rewarded the prepared. That is how it always works, and it is exactly the kind of moment that builds real estate fortunes for the people paying attention.

If you want to see precisely where your home stands in today’s numbers, or you want to know which corridor opportunities fit your situation before the crowd catches on, the live DFW market data is up for you, and I am one call away. Let’s get you five steps ahead. Schedule a consultation

Bobby Franklin, REALTOR®

Legacy Realty Group – Leslie Majors Team

📲 214-228-0003 | northtexasmarketinsider.com

Lender recommendations reflect expertise and service only, and I receive no compensation for referrals. Market data is current as of publication and subject to change, nothing here is financial, legal, or investment advice, and all real estate services are provided in full compliance with the Fair Housing Act and TREC.