By Bobby Franklin, REALTOR® | North Texas Market Insider™ | Legacy Realty Group – Leslie Majors Team | Waxahachie, TX | 214-228-0003 | northtexasmarketinsider.com

Last Updated: April 13, 2026 | Reading Time: ~25 minutes

⚡ Companion Resource: This article is a deep dive on the Iran conflict as a geopolitical force on North Texas real estate covering the history, the fallout, 2026 forecasting, and the strategic playbook on how to succeed in this market. For the full March snapshot of DFW inventory, prices, days on market, and county-by-county data, read the March 2026 North Texas Market Report. For the full 2026 guide read The Complete 2026 North Texas Real Estate Intelligence Report .

Section 1: The Strike That Moved Your Mortgage

At 06:35 UTC on Saturday, February 28, 2026, U.S. Central Command announced that American and Israeli forces had launched Operation Epic Fury, a joint air campaign against Iran that ran nearly 900 strikes in the first twelve hours. B-2 stealth bombers. B-1 Lancers. B-52 Stratofortresses. Tomahawk cruise missiles. Army HIMARS launchers. All deployed at once. The stated objectives were direct: destroy Iran’s nuclear and ballistic missile programs, eliminate the naval threat, and remove Supreme Leader Ali Khamenei. Within hours, Khamenei was confirmed killed alongside dozens of senior Iranian officials.

Global energy markets did not wait for daylight to react. By Sunday evening, before a single U.S. mortgage lender had opened for business, West Texas Intermediate crude had ripped 8% to roughly $72 a barrel, up from $67 on Friday. Brent crude jumped to around $79 from $72.87. About 20% of the world’s oil supply moves through the Strait of Hormuz, and Iran’s retaliatory strikes on two vessels in the strait turned a theoretical supply disruption into a live one. By late March, spot price on Brent crude touched a wartime high of $124.68 per barrel.

The mortgage market absorbed the shock just inside 72 hours. On February 26, two days before the strikes, Freddie Mac’s Primary Mortgage Market Survey printed the 30-year fixed at 5.98%, the lowest reading in three years and the first time rates touched the fives since September 2022. North Texas was lined up for its strongest spring in years. Then Operation Epic Fury began. Within days the 30-year crossed back above 6%. By April 2 it was at 6.46%, a 48-basis-point spike in five weeks, the fastest sustained rate increase since the Fed’s 2022 tightening cycle.

Run the math on a North Texas buyer financing $450,000. Locked at 5.98% in late February? Roughly $1,346 less per year than the identical buyer locked at 6.46% in early April. Over 30 years that compounds to more than $40,000 in additional interest. One military operation, half a world away, transferred tens of thousands of dollars from North Texas homebuyers to the bond market, before most people had even heard the name Operation Epic Fury.

Below is a full-spectrum analysis: how a war becomes a mortgage payment, what history says happens next, and the strategic playbook for every buyer, seller, and relocator in North Texas right now.

Section 2: The Transmission Mechanism – How a War Becomes a Mortgage Payment

Most people experience mortgage rate moves as numbers on a lender’s website. The chain that connects bombs in Tehran to your monthly payment is real, mechanical, and traceable. Understanding it is what separates reactive buyers from strategic ones.

Step 1: Oil Prices and Energy Inflation

Iran is a major crude producer, and the Strait of Hormuz, the oil transportation chokepoint this conflict is based around, is the single most critical oil passage on the planet. About 15–20 million barrels per day move through the Strait, roughly 20% of global supply. When that transit is threatened, as it was on February 28, oil traders reprice global supply risk immediately. Gasoline, diesel, aviation fuel, and every petroleum-dependent supply chain follow.

Step 2: Oil Prices Stoke Inflation Expectations

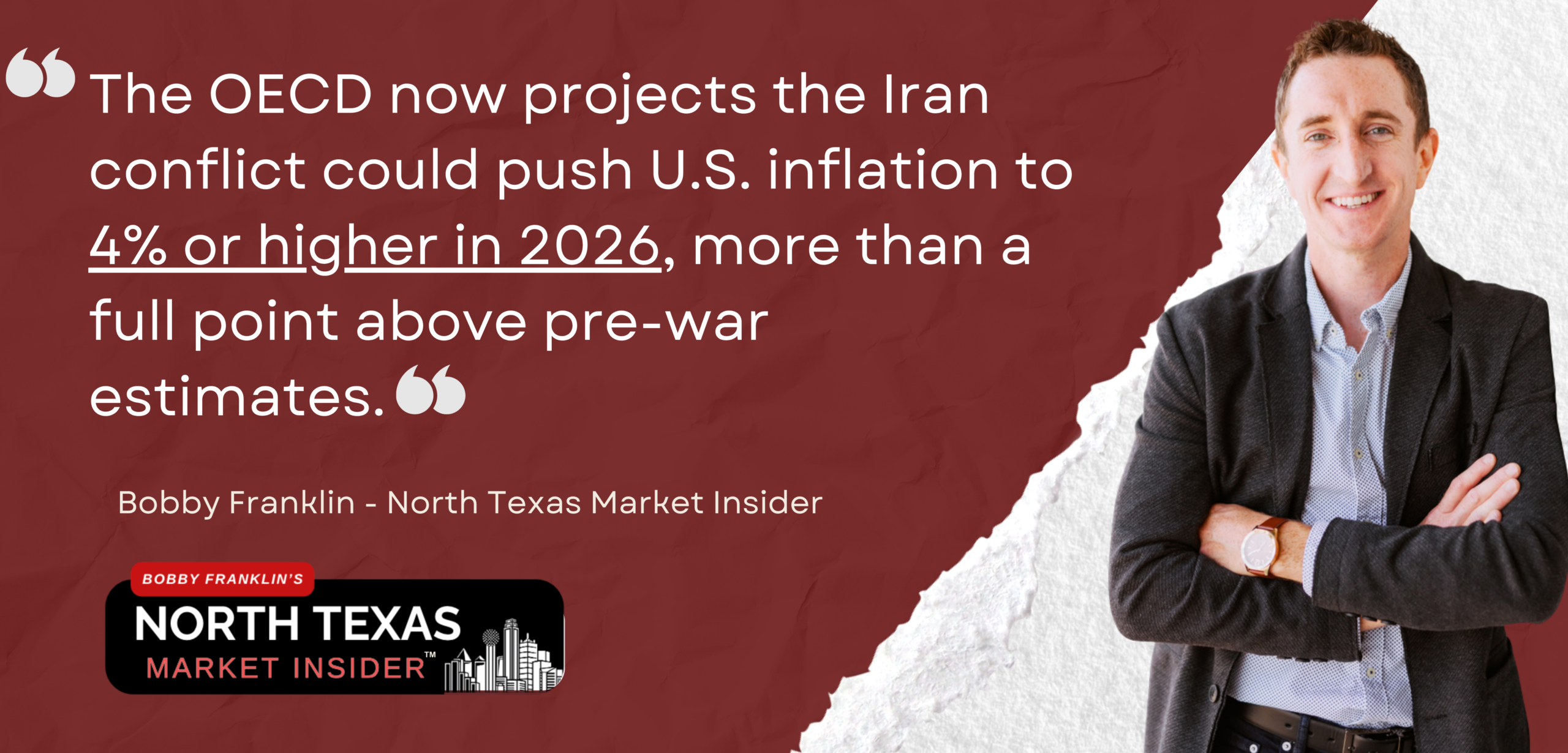

Energy spikes do not stay at the gas pump. Diesel rises, which raises trucking costs across the entire American goods economy. Petrochemical feedstocks get more expensive, dragging up plastics, chemicals, and manufactured goods. Airlines raise fares. Food distribution costs jump. The Producer Price Index and Consumer Price Index both climb. The Fed’s preferred gauge, PCE, gets pulled higher. The OECD now projects the Iran conflict could push U.S. inflation to 4% or higher in 2026, more than a full point above pre-war estimates.

Step 3: Inflation Expectations Drive Treasury Yields Higher

Bond investors require a yield premium above expected inflation. When inflation expectations rise, they sell bonds. Bond prices fall. Yields rise. The benchmark 10-year U.S. Treasury yield, trading near 3.92% at an 11-month low just before the strikes, reversed violently. By March 3 it was over 4.11%. By late March, 4.43%. Here is the part that makes this conflict different: in most geopolitical crises, investors run to the safety of U.S. Treasuries, which pushes yields down and pulls mortgage rates with them. Iran produced the opposite. The inflation signal overwhelmed the safety signal. That distinction is the entire reason this conflict hit mortgage rates so hard.

Step 4: Treasury Yields Move Mortgage Rates

The 30-year fixed mortgage is priced as a spread above the 10-year Treasury yield. Historically that spread sits at 170–200 basis points. So when the 10-year climbed roughly 50 basis points from late February to late March, mortgage rates moved with it, plus more, as MBS volatility compounded the move.

Step 5: MBS Spread Dynamics Amplify the Move

Most mortgages get securitized into Mortgage-Backed Securities (MBS) – bond instruments sold primarily through Fannie Mae and Freddie Mac to institutional investors. The yield those investors demand on MBS sets the rate lenders can offer. During market stress, MBS spreads widen, investors demand more premium above Treasuries to hold mortgage paper. From late January to late March 2026, current-coupon MBS spreads widened from 0.94% to roughly 1.25%, a 31-basis-point widening on top of the Treasury move. That is why mortgage rates rose faster than Treasury yields alone would predict. To counter it, the Trump administration directed Fannie Mae and Freddie Mac to step up MBS purchases signaling direct intervention to compress spreads and pull rates lower.

The Complete Transmission Chain

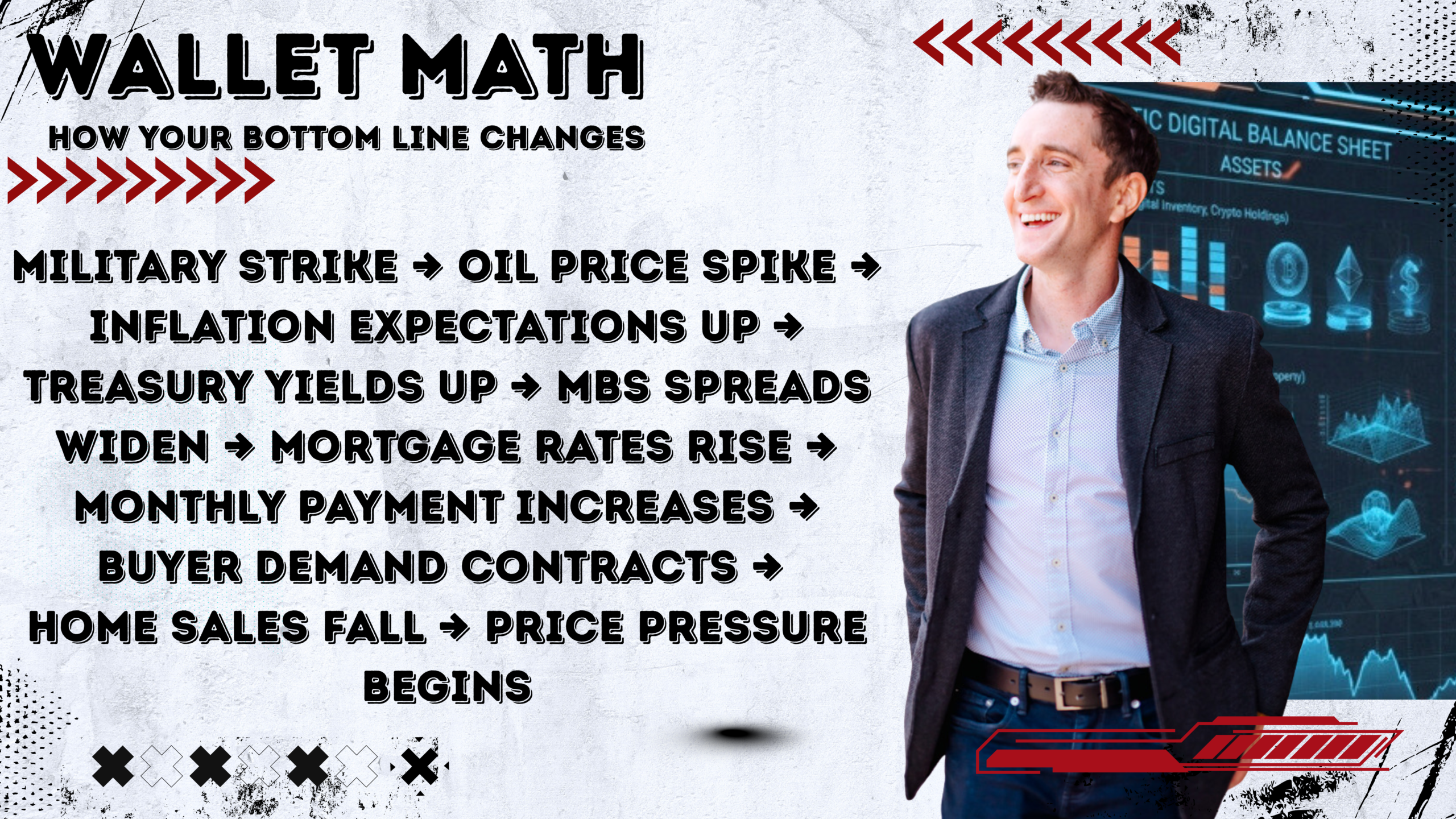

Military Strike → Oil Price Spike → Inflation Expectations Up → Treasury Yields Up → MBS Spreads Widen → Mortgage Rates Rise → Monthly Payment Increases → Buyer Demand Contracts → Home Sales Fall → Price Pressure Begins

This chain plays out in days, not months. Knowing every link is the difference between getting blindsided by a rate quote and understanding exactly why it changed and what conditions reverse it.

Section 3: Historical Precedent – What Past Middle East Conflicts Did to U.S. Housing

Geopolitical shocks are not new to mortgage markets. Four major conflicts since 1990 give us a data-rich playbook for what happens,m and what doesn’t happen, when Middle East tension explodes into American housing.

The 1990–91 Gulf War

When Iraq invaded Kuwait on August 2, 1990, crude oil nearly doubled from $20 to $40 per barrel within weeks. The 30-year fixed mortgage, 9.84% when Kuwait was invaded – climbed to 10.04% by September 1990. Housing was already weakened by the savings and loan crisis and a real estate bubble that had started deflating. The war accelerated the contraction.

Then the pattern flipped hard. By the time U.S. warplanes hit Baghdad on January 17, 1991, the 30-year had pulled back to 9.55%. When the ceasefire came in February 1991, the market detonated with buyer activity. Mortgage lenders described phones “ringing off the hook.” Houston and Denver saw sales jump 20%+ from year-ago levels. The end of the war, not the beginning, was the most powerful stimulant for housing demand.

The pattern: Short conflict → brief rate spike → sharp recovery on ceasefire. The market endured not because the conflict was mild but because its resolution was decisive.

The 2003 Iraq Invasion

The March 19, 2003 invasion hit a totally different housing backdrop. Rates were at 40-year lows around 6% and demand was surging nationally. There was no comparable oil crisis. The Fed’s post-9/11 easing had flooded the system with cheap credit. Mortgage rates barely flinched. Housing barely noticed.

The lesson is not that war is irrelevant to housing. The lesson is that monetary policy context determines the war’s impact. In 2003 the Fed was in full easing mode. Inflation pressure from oil got absorbed without a rate spiral. That environment is the exact opposite of 2026, where the Fed is fighting elevated inflation with no room to cut aggressively without reigniting prices.

The 2011 Libya Conflict and Arab Spring Oil Shock

When the Arab Spring escalated into civil war in Libya, oil ripped hard, crude hit $96 per barrel in February 2011, a two-and-a-half-year high. Brent-Dubai differentials widened sharply as light sweet Libyan crude vanished from global markets. But U.S. mortgage rates and housing were struggling for an entirely different reason: the wreckage of 2008 was still being absorbed. Home prices were falling. The S&P/Case-Shiller index showed declines in 11 major cities.

The 2011 oil shock had minimal direct impact on mortgage rates because the Fed had every weapon deployed, near-zero rates and quantitative easing, to keep yields suppressed. The lesson: when central banks are buying Treasuries and MBS aggressively, oil spikes can’t push yields meaningfully higher. No such QE program exists in 2026, which is why this transmission is so much more direct and so much more painful.

The 2022 Russia-Ukraine Invasion

The February 24, 2022 Russian invasion produced a counterintuitive initial result for U.S. mortgage rates: they briefly fell, from 4.19% to 3.89% as the classic flight-to-safety into Treasuries played out. The relief was short. Within two weeks, rates rebounded to 4.28% and were rising fast as inflation took over. The Fed launched its historic tightening in March 2022. By October 2023, 30-year rates hit 7.79%.

Ukraine is the most relevant modern precedent for 2026, with one critical difference: in 2022 the flight-to-safety dynamic suppressed rates briefly. In 2026 that dynamic largely failed to materialize because investors are now questioning whether war spending and energy-driven inflation might erode the U.S. fiscal position. When global investors question U.S. creditworthiness even at the margins, Treasuries lose their safe-haven premium and mortgage rates rise faster and higher than simple oil-inflation math would predict.

Historical Geopolitical Conflicts and U.S. Housing Market Impact

| Conflict | Oil Spike | Mortgage Rate Move | Home Sales Impact | Recovery Timeline |

|---|---|---|---|---|

| Gulf War 1990–91 | $20 → $40/bbl (+100%) | 9.84% → 10.04%, then fell to 9.55% | Frozen during conflict, sharp rebound at ceasefire (+20–46% in some markets) | 2–3 months post-ceasefire |

| Iraq Invasion 2003 | Moderate; no crisis-level spike | Minimal movement; rates stayed near 6% | Housing boom continued uninterrupted | No disruption |

| Libya/Arab Spring 2011 | ~$96/bbl (2.5-yr high) | Minimal; QE suppressed yields | Already declining from prior crisis; Arab Spring added uncertainty | Gradual; recovery by 2012 |

| Russia-Ukraine 2022 | $90s–$120s/bbl | Brief dip 4.19% → 3.89%, then surged to 7.79% by Oct 2023 (Fed-driven) | Slowed sharply as rates rose; price growth peaked 2022 | 18–24 months |

| US-Israel/Iran 2026 | ~$67 → $124 spot Brent; ~$95–97 post-ceasefire | 5.98% → 6.46% (5 weeks); 6.37% post-ceasefire | March existing home sales: 3.98M (9-month low); apps down 3–5% | Scenario-dependent |

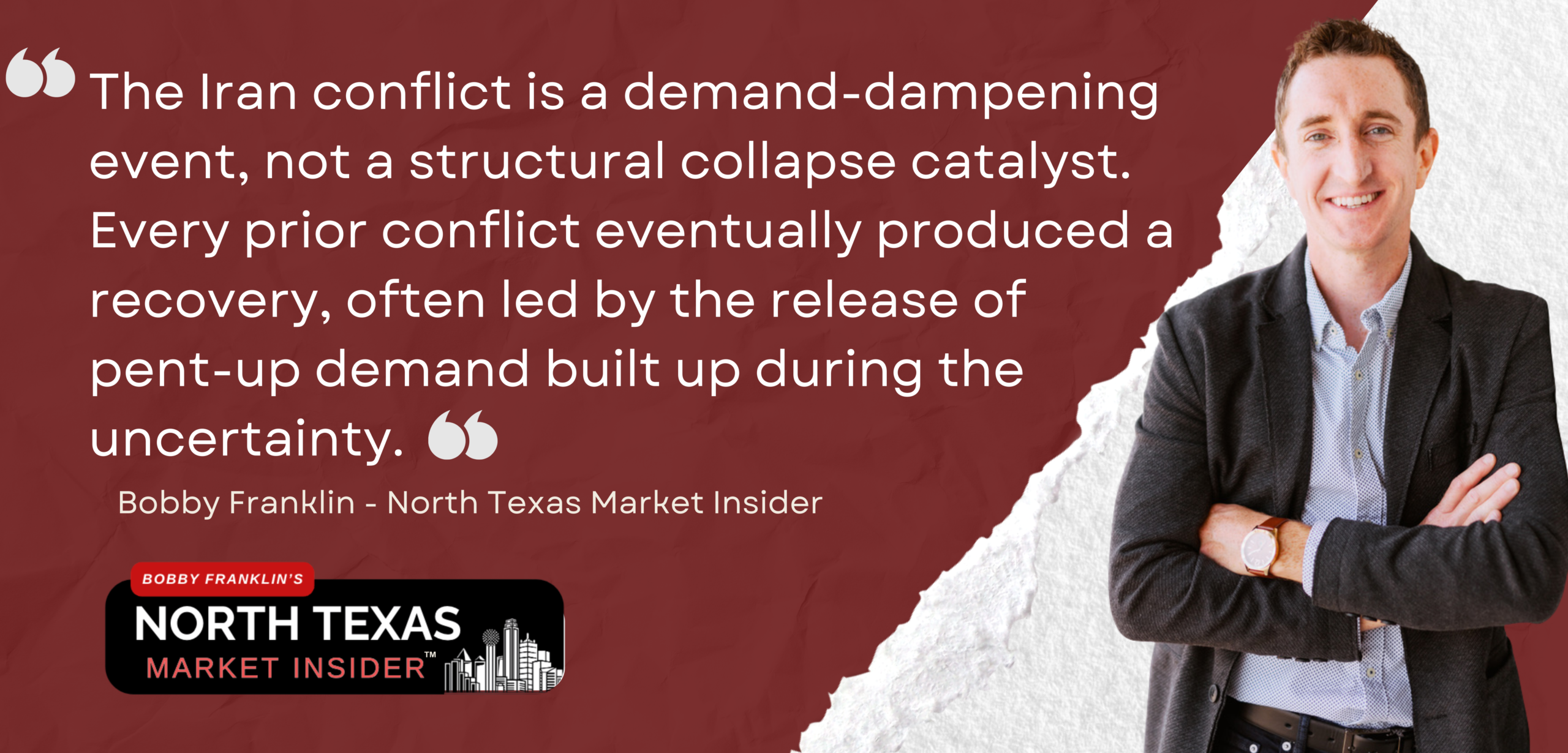

The pattern across four decades is consistent: Geopolitical oil shocks temporarily disrupt housing markets. They do not cause housing crashes. Crashes require overlapping structural failures like predatory lending, speculative bubbles and forced selling at scale. The Iran conflict is a demand-dampening event, not a structural collapse catalyst. Every prior conflict eventually produced a recovery, often led by the release of pent-up demand built up during the uncertainty.

Section 4: The Fed’s Impossible Position

No institution is more constrained by the Iran conflict than the Federal Reserve. Understanding their bind is essential to understanding where rates go next.

The March 17–18, 2026 FOMC Meeting

The FOMC met March 17–18 against the worst possible backdrop for monetary policymakers: a surging energy-driven inflation shock colliding with a softening labor market. The result: an 11-1 vote to hold the federal funds rate at 3.5%–3.75%. The lone dissent came from Trump appointee Stephen Miran, who pushed for a quarter-point cut citing labor market deterioration. Critically, Governor Christopher Waller, who had voted to cut in January, flipped to hold ratres, citing energy-driven inflation risk.

The revised dot plot was sobering: seven of 19 FOMC members now project zero rate cuts in 2026, up from a smaller number before the conflict. The median forecast still showed one cut this year, but the distribution shifted hard toward “higher for longer.” Markets had been pricing two cuts before the war. After March, one was the maximum base case and now even that is getting shaky.

The April 8 Minutes: Rate Hikes on the Table

The release of the March meeting minutes on April 8 made the Fed’s dilemma official. “Some” officials supported language that explicitly acknowledged the possibility of future rate increases. In Fed-speak, that is a major escalation. Officials acknowledged that after years of inflation running above their 2% target, “long-term inflation expectations could become more reactive to fluctuations in energy prices.” Translation: if the public starts expecting 4%+ inflation rather than 2%, the Fed loses its anchor which could be the most dangerous outcome in monetary policy.

Why This Fed Is More Constrained Than Any in Recent Memory

Jerome Powell faces a combination with no modern precedent: energy-driven stagflation risk + fiscal deficits + war spending + a divided FOMC + a presidential term expiring in May 2026. Cutting rates to support housing risks inflaming oil-shock inflation that could spiral into the kind of price-wage cycle we haven’t seen since the 1970s. Hiking rates to kill inflation risks a recession in a labor market already showing cracks. Holding steady, the path they chose, is the monetary policy version of driving in a storm with both hands on the wheel hoping the road straightens before the next curve.

The practical implication for DFW buyers and sellers: the Fed is not coming to the rescue. Do not build your purchase strategy around rate cuts arriving in time for the 2026 spring or summer market. This is a make-your-move-on-the-fundamentals market, not a wait-for-the-Fed market. For more on how the March pause creates a strategic window for North Texas sellers, read the companion piece: Why the Fed’s March 2026 Rate Pause Is the Green Light to Sell in North Texas.

Section 5: Rate Whiplash by the Week The Real Money Impact

Basis points only become real money when you apply them to a real loan. Here is the week-by-week and what it means for every buyer segment in North Texas, first-time buyers in Ennis to move-up executives in Southlake.

The Freddie Mac PMMS Timeline: February 26 to April 9, 2026

| Week Ending | 30-Yr Fixed (Freddie Mac) | Weekly Change | Key Event |

|---|---|---|---|

| Feb 19, 2026 | 6.01% | –0.08 | Pre-war trend down |

| Feb 26, 2026 | 5.98% | –0.03 | Pre-strike low; 3-yr low |

| Mar 5, 2026 | 6.00% | +0.02 | Operation Epic Fury; first reaction |

| Mar 12, 2026 | 6.11% | +0.11 | Oil above $80; inflation fears build |

| Mar 19, 2026 | 6.22% | +0.11 | FOMC holds 11-1; Waller flips to hold |

| Mar 26, 2026 | 6.38% | +0.16 | 4th straight increase; highest since Sep |

| Apr 2, 2026 | 6.46% | +0.08 | 5th consecutive increase; 7-month high |

| Apr 9, 2026 | 6.37% | –0.09 | First drop in 6 weeks; ceasefire effect |

Source: Freddie Mac Primary Mortgage Market Survey

Payment Math: Waxahachie to Southlake

Numbers below are principal and interest only (no taxes, insurance, or HOA) on 30-year fixed mortgages at four key benchmarks.

| Loan Amount | @ 5.98% (Pre-War Low) | @ 6.22% (FOMC Week) | @ 6.46% (Apr 2 Peak) | Monthly Increase (Low→Peak) |

|---|---|---|---|---|

| $300,000 | $1,796 | $1,846 | $1,887 | **+$91/mo |

| $400,000 | $2,394 | $2,461 | $2,517 | **+$123/mo |

| $500,000 | $2,993 | $3,077 | $3,147 | **+$154/mo |

| $650,000 | $3,890 | $4,000 | $4,091 | **+$201/mo |

For the typical North Texas buyer, purchasing in the $350,000–$475,000 range in Waxahachie, Midlothian, Red Oak, or Mansfield, this rate swing meant a tangible setback of $100–150 per month. Not catastrophic. But enough to push some first-time buyers out of approval range and to make move-up buyers rethink their upgrade timeline.

For where these rate moves fit in the broader 2026 affordability picture, see: Will Housing Actually Become Affordable in 2026?

Section 6: The Construction Cost Chain Reaction

The Iran war’s housing impact runs beyond mortgage rates and directly into the physical cost of building homes, a channel that threatens DFW’s inventory pipeline at the worst possible time.

Materials Costs: The Energy-to-Construction Link

Every major construction material has an embedded energy cost. Steel takes massive energy to produce. Cement requires kiln temperatures only fossil fuels can reach. PVC, polyurethane, and epoxy are petroleum derivatives. Diesel powers every truck, crane, and piece of heavy equipment on a jobsite. When oil pushes $120, construction input prices spike across the board.

Associated Builders and Contractors reported construction input prices jumped 1.3% in February 2026 alone, before the strikes even started. Annualized, that is 12.6%, a trajectory that threatens project economics at every level. A Linesight construction consultancy report shows materials costs for homebuilders up 15–39% year-over-year across critical categories: steel up 15–25%, cement up 10–18%, PVC and plastics up 20–33%, construction chemicals up 15–24%.

New Home Sales: The Cascade

The numbers from major homebuilders confirm the pressure. Lennar’s Q1 2026 revenue came in at $6.62 billion against $6.93 billion in analyst expectations, a 13.3% YoY decline, with operating margins collapsing from 9.1% to 5.1%. D.R. Horton showed more resilience, beating Q1 estimates with $6.9 billion in revenue and reaffirming full-year guidance of $33.5–$35 billion. But homebuilder stocks have been punished sector-wide: D.R. Horton is down 27% from its 52-week high; Lennar is down 47%. New home sales from builders fell roughly 17% month-over-month in early 2026 per Reventure data.

What This Means for DFW Inventory

Here is the paradox builders face: rising material costs compress margins on new homes at the exact moment they need to increase incentives and trim prices to keep velocity. The result is fewer spec starts, a thinner pipeline of future inventory, and a heavier reliance on buyer-funded rate buydowns rather than outright price cuts. For DFW specifically, where new construction is a far bigger share of inventory than most U.S. markets, this pipeline compression matters enormously.

The long-term consequence: the housing supply shortage in North Texas, already estimated at 400,000 units over the next decade, gets deeper, not shallower. Every new home that doesn’t get started today is a home unavailable in 2027 or 2028. That supply gap creates a structural floor under prices even in this short-term demand disruption. For new construction in South DFW: The 5 New Construction Gold Mines Under $350K in South DFW.

Section 7: The Ceasefire Scenario Matrix

On April 7–8, 2026, a two-week ceasefire was announced between the U.S. and Iran. The terms: American military strikes suspended; Iran agrees to reopen the Strait of Hormuz for safe vessel transit. Oil dropped 13–16% immediately. The Dow ripped 1,300 points. The 10-year fell sharply. Mortgage rates responded, down to 6.37% in the April 9 Freddie Mac survey, the first decline in six weeks. But the ceasefire is fragile. Iran accused the U.S. of breaching terms within 24 hours. Talks between VP Vance and Iranian officials in Pakistan collapsed April 12 over nuclear weapons demands.

Three scenarios now determine the North Texas trajectory. The probability-weighted read:

Scenario A: Ceasefire Holds and Conflict De-escalates (35% Probability)

Conditions: The two-week ceasefire extends into a durable agreement. The Strait fully reopens. Oil stabilizes in $75–85.

- Mortgage rates: Pull back toward 6.0–6.2% by May; sub-6% possible by Q3 2026 if the Fed gets one cut in.

- DFW home sales: Spring partially recovers. Pent-up demand from the buyers who paused in March and April floods back. The 3.98% YoY decline in national existing home sales reverses.

- Prices: Modest appreciation resumes. DFW’s TRERC-projected 1.3–1.8% annual appreciation is achievable.

- Builder activity: Spec starts reaccelerate. Incentives stay strong but moderate. DR Horton’s full-year guidance of 86,000–88,000 closings looks achievable.

- For North Texas buyers: The “buy now” scenario. Lock 6.0–6.2% before competition returns. Builder rate buydowns drop effective rates into the mid-5s. New construction incentives in DFW are the best vehicle.

Scenario B: Ceasefire Collapses and Conflict Escalates (30% Probability)

Conditions: Talks fail. Strikes resume. The Strait stays restricted 60+ days. Oil returns to $115–130. Iran’s nuclear program intact.

- Mortgage rates: Spike back to 6.6–6.8%. If the Fed gets forced to raise to fight a second inflation wave, 7%+ is on the table by Q4 2026.

- DFW home sales: The worst-case Zillow scenario (existing sales -0.73% YoY) materializes nationally. DFW outperforms on structural demand but still absorbs a 15–25% volume decline.

- Prices: Flat to -1% in DFW; potentially -2% to -5% in overbuilt northern suburbs. Ellis County, with its lower absolute prices and value-driven demand, holds better than Frisco or Allen.

- Builder activity: Material cost spikes force project delays. Spec starts drop hard. Incentive packages explode; 3-2-1 buydowns, $50,000+ flex cash. Buyers with cash or pre-approval capture historically strong deals.

- For North Texas buyers: The “negotiate hard” scenario. Seller concessions of 3–5% achievable. Builder packages become extraordinary. Rate-lock strategy and lock periods become critical.

Scenario C: Prolonged Stalemate with No Formal Resolution (35% Probability)

Conditions: Neither side achieves victory or peace. Low-level conflict continues. Oil stabilizes $90–105 with ongoing supply uncertainty.

- Mortgage rates: Stay 6.25–6.50% through most of 2026. One Fed cut possible late, but the 10-year stays elevated at 4.2–4.4%.

- DFW home sales: Volume runs 10–15% below pre-war trajectory. Days on market stay elevated (50–60 metro, 80–90 Ellis County). Seller price reductions continue at elevated pace.

- Prices: Essentially flat in DFW metro. Ellis County holds at +0.5% to +1.5% on affordability-driven demand and corporate relocation momentum.

- Investor opportunity: Rental yields remain strong as rate-locked-out would-be buyers stay renting. Single-family rental demand in Waxahachie, Red Oak, and Midlothian stays robust.

- For North Texas buyers: The “systematic drip” play – buy on timeline, not market timing. Leverage builder incentives. Refi when the stalemate eventually resolves. Time in the market beats timing the market.

Section 8: Why North Texas Absorbs Macro Shocks Better Than Anywhere Else

Every macro shock hits local real estate markets differently based on the underlying demand fundamentals. The DFW metroplex has the deepest, most diversified, most durable demand foundation of any major metro in America and the Iran conflict, as serious as its near-term impact is, does not change that structural reality.

The Corporate Relocation Engine

Since 2018, over 100 corporate headquarters have relocated to DFW, more than any competing metro. Charles Schwab. CBRE. Oracle (partial). McKesson. Caterpillar Financial. These are not branch offices. These are full headquarters that import thousands of high-income employees who need housing in commuting distance. The Dallas Regional Chamber confirmed continued momentum through Q1 2026, with new relocations, expansions, and investments announced despite the conflict. Geopolitical noise may slow this pace at the margins. It does not reverse the fundamental cost, tax, and talent advantages that make Texas the default for corporate America.

Job Creation at Scale

DFW added approximately 46,800 non-farm jobs year-over-year as of February 2026, holding its status as a top-two U.S. metro for total job creation. Average hourly wages in Dallas reached $37.71, 6.0% YoY growth, outpacing national wage growth of 3.8%. Job growth is the primary driver of housing demand. As long as DFW creates jobs at this rate across tech, healthcare, finance, logistics, manufacturing, and energy, housing demand has a structural floor independent of any single geopolitical event.

Population Growth: 339 New Residents Per Day

Latest Census Bureau estimates show DFW added approximately 123,557 new residents in 2024–2025, about 339 people per day. Even with international migration slowing on federal policy changes, domestic migration into Texas stays strong. Dozens of new Texas laws from the 2025 legislative session have strengthened property rights, streamlined business formation, and made Texas even more attractive relative to high-tax coastal states. Each of those 339 daily new residents eventually needs housing, as a renter who keeps multifamily occupancy strong, or as a buyer creating demand for the next available listing.

Economic Diversification: The Shock Absorber Nobody Talks About

DFW’s economy is deliberately diversified across financial services (American Airlines, AT&T, Celanese HQ), technology (Texas Instruments, Match Group, Keurig Dr Pepper), healthcare (UT Southwestern, Baylor Scott & White), logistics (major e-commerce and distribution corridors), and energy (traditional and renewable). Unlike Houston, which wobbles with oil prices, or Austin, heavily dependent on tech capital, DFW absorbs sector-specific shocks without systemic demand collapse. When energy weakens, healthcare hires. When tech pulls back, financial services and logistics expand. The diversification that makes DFW less exciting to write about in boom cycles is exactly what makes it the most resilient market in shock cycles.

The No-State-Income-Tax Multiplier

Texas levies no personal state income tax. For a household earning $150,000, typical for a dual-income family driving a $475,000–$600,000 home purchase in the DFW suburbs, that is $10,000–$20,000 in annual tax savings compared to California, Washington, Oregon, or Colorado. That’s a 30-year mortgage payment differential that operates every single year, regardless of oil prices, Fed policy, or Middle East geopolitics. As long as that advantage holds, Texas absorbs a disproportionate share of high-income domestic migration, and the housing demand that comes with it.

The PwC Verdict: #1 Market in America

PwC’s “Emerging Trends in Real Estate” report ranked Dallas-Fort Worth #1 overall for investment and development prospects in 2026, the second consecutive year at the top. When the world’s largest professional services firm puts its reputation on a market ranking, and that ranking says DFW for two straight years, geopolitical noise doesn’t change the structural conclusion.

North Texas is not immune to the Iran shock, but is the most resistant major metro in America to this specific type of shock. The demand floor here; corporate relocations, job growth, population inflows, economic diversification, is real, data-verified, and durable.

Section 9: The Strategic Playbook – What to Do Right Now

Uncertainty is not a reason to do nothing. It is a reason to act with more intelligence. The specific tactical playbook for each of the four major reader segments in North Texas:

🏠 First-Time Buyers

Your situation: You were weeks from pulling the trigger when rates jumped from 5.98% to 6.46%. You’re asking whether to wait for rates to come back or move now.

The strategic move: Use builder incentives as your rate-reduction vehicle. DFW’s new construction market, particularly Ellis County (Waxahachie, Midlothian, Red Oak), southern Tarrant County (Mansfield, other South DFW communities), and select Johnson County communities, is currently offering some of the most aggressive rate buydown packages since 2008. DR Horton, Lennar, and smaller regional builders are funding 3-2-1 buydown structures that drop your effective rate 2–3 percentage points in Year 1.

- On a $325,000 home at 6.46%, a builder-funded 2-1 buydown looks like this: Year 1 effective rate 4.46% (~$1,640 payment). Year 2 effective rate 5.46% (~$1,830). Year 3+ at 6.46% (~$2,050). Year 1 monthly savings vs. market rate: ~$410. That is real affordability relief funded entirely by the builder, not by waiting on the Fed.

- Stack down payment assistance. Texas has multiple programs that grant 3–5% down for first-time buyers. On a $325,000 purchase, that’s $9,750–$16,250 in assistance. Ask your lender specifically about TSAHC and TDHCA programs. As your agent, I’ll connect you to my three preferred lender partners, Denise Donoghue at The Mortgage Nerd, Andrew Bryan at Miramar Mortgage, and Ethan Hester at Midtex Mortgage, to compare programs and rates side-by-side.

- Target Ellis County. Waxahachie at $370K median, Midlothian at $538K for new construction, Red Oak under $340K. This is where first-time buyers get the most house for the money in the DFW metro.

- Do not wait for 5% rates. If 5% rates arrive, they arrive with 50 competitive buyers per listing. Buy at 6.46% with low competition, then refinance. The house you buy today starts appreciating today, regardless of your rate.

📈 Move-Up Buyers

Your situation: You bought 2015–2020. You have significant equity. You want to upgrade from a $350,000 home to a $500,000–$650,000 home but feel locked by the rate gap between your current 3–4% mortgage and today’s 6.46%.

The strategic move: Use the buyer’s market on your purchase. Price competitively on your sale.

- Your equity is real and portable. A 2018 Waxahachie purchase at $285,000 is worth ~$365,000 today. That’s $80,000+ in appreciation already banked. That equity doesn’t disappear when you sell, it funds your down payment on the next home, reducing the loan balance and the payment impact of the higher rate.

- It is a buyer’s market for your purchase. DFW listings are up ~20% YoY. Sellers cut over 8,000 asking prices in March 2026 alone. You have negotiating leverage you haven’t seen since 2019. Use it to negotiate seller concessions, typically 2–3% of purchase price, toward a permanent rate buydown.

- New construction extended close timelines work in your favor. Build with an 8–10 month close window. Sell your current home as construction completes. Coordinate closings to minimize bridge financing.

- The payment differential is real but manageable. Trading a 3.5% $285,000 mortgage ($1,280/month) for a 6.46% $460,000 mortgage ($2,895/month) is a $1,615/month increase. But your household income is materially higher than 2018. At 6% wage growth, a $100,000 household income in 2018 is $134,000 today, a $34,000/year income increase. The payment increase is painful, but it’s proportional, not catastrophic.

🏡 Sellers

Your situation: You need to sell. Rising rates, war uncertainty, and 8,000+ competing price reductions in March have you nervous about pricing.

The strategic move: Price aggressively to land in the top 20% of value in your submarket, not the median.

- The buyers active right now are serious buyers. Rate shock has already chased the casuals to the sidelines. Buyers touring at 6.46% have real need and real urgency whether it’s job relocations, growing families, or downsizing. Price correctly and you’re negotiating with motivated buyers, don’t and you get mostly tire-kickers.

- Offer seller concessions toward rate buydowns. A 2–3% seller concession offered specifically toward buying down the buyer’s rate, is the highest-ROI closing tool in this market. A $400,000 seller offering $10,000 toward a rate buydown effectively drops the buyer’s payment by ~$100/month for years. Buyers on the fence about affordability will cross the line for a $10,000 buydown credit. Sellers who refuse and drop their price $10,000 accomplish the same thing for less impact on the buyer’s monthly cost.

- Professional photography, pre-listing inspection, and strategic pricing are non-negotiable. The margin between a 30-day sale and a 90-day sale in this market is almost entirely execution, not luck. Overpriced homes that sit accumulate negotiating leverage for buyers and stigma in the MLS. Price to move. Then execute.

- Don’t time the market. The ceasefire scenario that eventually resolves this conflict will bring buyers rushing back. By then, your competition rushes back too. The sellers who close in the next 60–90 days are competing into reduced inventory. The sellers who wait for “better conditions” are selling into a market with twice as many listings.

✈️ Out-of-State Relocators – California, Colorado, Washington, and International

If you’re reading this from California, Colorado, or Washington, or from outside the U.S., the Iran conflict is paradoxically improving your entry opportunity in North Texas, not hurting it.

- Your home state market is also under pressure. California, Colorado, and Washington are all experiencing rate-driven demand declines. If you’re planning to sell before moving, you’re selling into a softening market, which means acting sooner may produce a better price on your current home.

- DFW sellers are offering concessions they haven’t offered in years. Sellers are currently contributing to closing costs, rate buydowns, and home warranties at levels not seen since 2019. A relocation budget calibrated for the competitive 2024 market goes substantially further in 2026.

- The no-state-income-tax advantage is permanent. Whether oil is at $70 or $120, whether the Fed is cutting or holding, Texas’s zero state income tax is structural. For a California household earning $200,000, moving to Texas saves $18,000–$25,000+ in annual state income taxes. That savings funds your mortgage rate premium many times over.

- Specific relocation guides: Relocating from California | Relocating from Colorado | Relocating from Washington

Section 10: The 18-Month Outlook – North Texas Through Late 2027

Forecasting under geopolitical uncertainty requires intellectual honesty about what can and cannot be predicted with precision. What can be stated confidently is the range of outcomes and which structural forces persist across all of them.

What Stays Constant Across All Scenarios

- DFW population growth: 339 new residents per day. Demand doesn’t pause for geopolitical uncertainty.

- Corporate relocation momentum: Q1 2026 showed continued corporate expansion into North Texas. The factors driving it; no income tax, lower cost, pro-business environment, and infrastructure are independent of Middle East policy.

- The housing supply deficit: DFW needs roughly 400,000 new homes over the next decade. Construction cost pressure from the Iran war widens that deficit. Supply constraints support prices even in a demand-dampened environment.

- Ellis County’s value proposition: The $100,000–$150,000 price gap between Ellis County new construction and comparable product in Collin or Denton Counties does not narrow in a soft market. If anything, affordability-driven demand flows more strongly to value markets during rate-shock environments.

The 18-Month Timeline by Scenario

Scenario A (Ceasefire Holds): By Q3 2026, oil stabilizes below $85, the Fed executes one cut in late 2026, the 10-year pulls toward 4.0–4.1%. Freddie Mac 30-year reaches 5.85–6.0% by year-end. Spring 2027 becomes the strongest homebuying season since 2021, but with a critical difference: inventory is higher, prices are fairer, builder incentives stay strong. DFW leads national recovery metrics. By late 2027, DFW median prices sit 3–5% above April 2026 levels. The buyers who transacted in Q2–Q3 2026 right now capture both the softened prices and the equity appreciation of the recovery.

Scenario C (Prolonged Stalemate): By Q1 2027, the market has adapted to a “new normal” of 6.25–6.50% rates. Buyer psychology recalibrates the same way it did in 2018–2019 when 5% rates became accepted. Transaction volume runs 10–15% below 2025 levels nationally, but DFW closes the gap faster. New construction incentives stay robust through all of 2027. The Texas Real Estate Research Center forecast of median prices reaching $334,000 statewide by December 2026 looks achievable. By late 2027, DFW values sit 1.5–3% above current levels becoming modest but positive.

Scenario B (Escalation): This is the hardest scenario. If conflict resumes and oil surges to $115–125/barrel, mortgage rates push toward 6.8–7.2% and the Fed may be forced to hike. DFW transaction volume drops sharply in Q3 2026. Prices flatten to -1% in the metro. But, and this needs to be said clearly, even in this scenario, DFW does not collapse. The structural demand described in Section 8 does not evaporate in a conflict scenario. It pauses. The buyers who purchased at the 2020–2021 lows held their equity through 7.79% rates in 2023. The buyers who purchase today will hold their equity through whatever scenario materializes next. The fundamentals of the DFW market are not hostage to Middle East geopolitics.

The Call to Action

The chaos you’re reading about, oil at $95+, rates at 6.37–6.46%, a Fed that has quietly opened the door to hikes, a ceasefire that may or may not hold, is exactly the environment that creates the best opportunities for prepared buyers and strategic sellers. Confusion creates leverage. When the market is uncertain, sellers are more motivated, builders are more generous with incentives, and competition among buyers is reduced. The buyers and sellers who win in 2026 are not the ones who waited for clarity. They are the ones who acted with clarity while everyone else waited.

Frequently Asked Questions: Iran War, Mortgage Rates and the Housing Market

1. Will the Iran war cause a housing market crash in 2026?

No. Geopolitical conflicts do not cause housing crashes by themselves. Crashes require structural failures, predatory lending at scale, speculative bubbles, forced mass selling. None of those exist in the current U.S. housing market. The Iran conflict is a demand-dampening event that raises borrowing costs, slows transaction volume, and squeezes builder margins. Major housing research firms including Zillow, NAR, and Capital Economics do not forecast a housing crash from this conflict. They forecast slower sales, modest price adjustments in overbuilt markets, and recovery on de-escalation. In North Texas, where structural demand from corporate relocations, job growth, and population inflows creates an independent demand floor, the case for a crash is even weaker. The closest historical parallel, the 1990 Gulf War, produced a market freeze, not a crash, followed by a sharp rebound at ceasefire.

2. How do oil prices affect mortgage rates?

The chain of transmission: Oil prices rise → inflation expectations increase → bond investors demand higher yields → 10-year Treasury yield rises → mortgage rates (priced as a spread above the 10-year) rise. During market uncertainty, the spread between Treasuries and mortgage-backed securities (MBS) widens, meaning mortgage rates rise even faster than Treasury yields alone would predict. In the Iran conflict, the 10-year rose roughly 42–50 basis points from late February to late March 2026, MBS spreads widened another 31 basis points, and the combined mortgage rate increase was about 48 basis points over five weeks. See Section 2 above for the full mechanism.

3. Should I buy a house during a war?

Historical data consistently shows that buyers who purchased during, or immediately after, major geopolitical conflicts outperformed those who waited for resolution. After the 1990 Gulf War ceasefire, home sales surged 20–46% within months in markets like Houston, Denver, and Connecticut. After the 2022 Ukraine invasion’s initial disruption, buyers who held their positions built significant equity over the following 18–24 months. The principle: buy based on personal financial readiness and local market fundamentals, not geopolitical headlines. If your income is stable, your credit is strong, and you’re buying in a fundamentally sound market like North Texas, the conflict adds risk primarily as rate volatility, which builder incentive programs and rate buydowns can partially offset. The alternative, waiting indefinitely for geopolitical resolution, has historically cost buyers far more in rent and missed appreciation than any rate premium.

4. What happens to housing prices during geopolitical crises?

Home prices are more resilient to geopolitical crises than most people expect. Transaction volume is highly sensitive to uncertainty, buyers pause when the future is unclear. But prices require a supply-demand imbalance to fall meaningfully, and most geopolitical shocks do not create oversupply. In the current Iran conflict, the national median existing home price rose 1.4% YoY in March 2026, the 33rd consecutive month of price increases, even as sales volume fell to a 9-month low. In North Texas specifically, where population grows by 339 people per day and supply is structurally constrained, downward price pressure is limited primarily to overbuilt luxury and spec-heavy submarkets.

5. When will mortgage rates go back down after the Iran war?

The April 9 Freddie Mac survey already showed the first decline in six weeks (6.37%, down from 6.46%) following the ceasefire announcement. In a durable ceasefire scenario, rates could pull back toward 6.0–6.2% by Q2 2026 as oil normalizes and inflation expectations moderate. If the Fed executes its projected single rate cut in late 2026, rates could approach the high 5s by year-end. However, several structural forces, a widened federal deficit from war spending, persistent oil supply uncertainty, and MBS spread dynamics, suggest the sub-6% environment of late February 2026 may not return quickly even in a best-case diplomatic scenario. The prudent planning assumption is a 6.0–6.5% environment through most of 2026.

6. Is North Texas a good place to buy during the Iran conflict?

Yes, and arguably better now than before the conflict for buyers with solid financial footing. The Iran conflict has expanded seller concessions, increased days on market, and driven builder incentive packages to levels not seen in years. All buyer-favorable conditions. At the same time, North Texas’s structural advantages like the 120+ corporate relocations, 46,800+ annual jobs added, 339 daily new residents, PwC’s #1 ranking, and Texas’s zero state income tax provide a demand floor that makes North Texas uniquely resilient to the macro disruption. Buyers entering with proper financial preparation and a 5+ year horizon are buying into one of the most fundamentally sound real estate markets in the country at temporarily softened demand conditions. That is the definition of an opportunistic entry point.

7. How does the Iran war affect new home construction in DFW?

The Iran conflict affects DFW new construction through two channels: (1) higher material costs – construction input prices rose 12.6% annualized through February 2026, with steel up 15–25%, cement up 10–18%, PVC and plastics up 20–33% and (2) compressed builder margins driving some to reduce new spec starts. The near-term consequence is fewer new homes entering the pipeline in 2026–2027, deepening DFW’s existing supply deficit. Ironically, this supports long-term home values in North Texas even as the short-term rate shock dampens demand. Builders are currently compensating with aggressive incentive packages, rate buydowns, design credits, closing cost assistance that partially offset the rate increase for buyers who act now.

8. What is the Federal Reserve doing about mortgage rates during the Iran war?

The Fed held rates steady at 3.5%–3.75% at its March 17–18 FOMC meeting (11-1 vote), with only Trump appointee Stephen Miran dissenting in favor of a cut. The April 8 release of the March minutes revealed that “some” officials now want to keep rate increases on the table, an escalation from “several” who held that view in January. Simultaneously, the Trump administration directed Fannie Mae and Freddie Mac to increase MBS purchases to stabilize mortgage spreads. The Fed’s fundamental constraint: it cannot cut rates without potentially fueling oil-driven inflation, but it cannot raise rates without risking recession in a softening labor market. The result is a “higher for longer” rate environment more constrained than any Fed in recent memory.

9. How does the Strait of Hormuz affect gas and home prices in Texas?

The Strait of Hormuz carries approximately 20% of global crude oil daily. When that chokepoint is threatened, as happened when Iranian missiles struck two vessels in the strait on February 28, 2026, global oil markets reprice supply risk immediately. Oil spiked 8% overnight and continued rising for weeks, reaching a spot Brent high of $124.68/barrel. Higher crude prices flow directly into gasoline prices (impacting every Texas driver and business), diesel prices (raising trucking costs for all goods, including construction materials), and petrochemical feedstocks (raising costs for plastics, chemicals, and synthetic building materials). These energy costs feed PCE inflation, which the Fed monitors. When the Fed sees persistent energy-driven inflation, it delays rate cuts and mortgage rates stay elevated. For Texas homeowners specifically, the energy transmission is direct: diesel-heavy DFW construction activity becomes more expensive, new home costs rise, and the 15-39% material cost increases documented since the conflict began make the housing supply problem structurally worse.

10. Should I sell my North Texas home now or wait?

The March 2026 Federal Reserve rate pause, combined with an active buyer pool despite the Iran conflict, creates a strategic window serious sellers should not ignore. Active buyers in a 6.5% rate environment are serious buyers, rate shock has already filtered out casual shoppers. The sellers who price strategically now, offer targeted concessions (particularly rate buydown credits), and execute with professional marketing are closing transactions. The sellers who wait for “better conditions” are competing into a market where the ceasefire resolution brings both buyers and sellers back simultaneously. First-mover advantage belongs to sellers who act now. Read the companion analysis: Why the Fed’s March 2026 Rate Pause Is the Green Light to Sell in North Texas.

Ready to Make Your Strategic Move in North Texas? Schedule a consultation

Bobby Franklin | REALTOR® | North Texas Market Insider™ | Legacy Realty Group – Leslie Majors Team serves buyers, sellers, and relocators across Ellis County, DFW, and greater North Texas with data-driven intelligence that converts market uncertainty into competitive advantage.

Fair Housing Notice: Bobby Franklin and Legacy Realty Group – Leslie Majors Team are committed to the Fair Housing Act and offer services without regard to race, color, religion, national origin, sex, handicap, or familial status. Nothing in this article constitutes steering, discrimination, or commission-fixing of any kind. All information is for educational purposes only and is not legal, financial, or investment advice. Market data sourced from publicly available primary sources including Freddie Mac, NAR, Federal Reserve, Census Bureau, and Zillow Research.

Mortgage referrals provided to multiple lenders: Denise Donoghue at The Mortgage Nerd, Andrew Bryan at Miramar Mortgage, and Ethan Hester at Midtex Mortgage, in compliance with RESPA. Outbound links are provided for reference; North Texas Market Insider does not endorse or control third-party content. REALTOR® is a registered trademark of the National Association of REALTORS®. Equal Housing Opportunity.