By Bobby Franklin, REALTOR® | North Texas Market Insider™ | Legacy Realty Group – Leslie Majors Team

Serving Waxahachie, Midlothian, Ennis, Red Oak, and the greater Ellis County and DFW Metroplex

Updated: May 2026 | Reading Time: ~20 minutes

Here’s what I want you to understand before you read a single word of this article: the people waiting on the sidelines for rates to “come back down” aren’t being patient. They’re either misinformed, or practicing magical thinking. I’d rather give you the uncomfortable truth than the comfortable story most agents are still telling.

On May 7, 2026, Freddie Mac’s Primary Mortgage Market Survey® (PMMS®) confirmed the 30-year fixed-rate mortgage is averaging 6.37%, up from 6.30% the week prior. Freddie Mac Chief Economist Sam Khater was blunt about it: there is “no clear near-term catalyst for a meaningful, sustained decline.”

Sit with that sentence for a second, because it’s doing a lot of work.

This isn’t a bad-news article. I don’t write those. This is an intelligence briefing, the kind I wish every buyer and seller in Waxahachie, Midlothian, Ellis County, and greater DFW had in their inbox before they made their next move. By the time you finish reading, you’ll understand exactly: why rates are where they are, why 3% would require something catastrophic, what the 10-year Treasury actually has to do with your mortgage payment, and most importantly, what your next move looks like right now in this market.

Let’s get into it.

The Real Reason Rates Are at 6.37% (And Why Nobody’s Telling You the Full Story)

Most rate coverage reads like a weather report. Here’s the number, here are some quotes, good luck. I’m going to give you the actual mechanisms, because understanding the why is what separates strategic buyers from people who keep waiting and losing.

Geopolitics Is Driving Everything Right Now

The dominant force behind the May 2026 rate increase isn’t the Fed, and it isn’t the housing market. It’s the escalating U.S.-Iran conflict and what it’s doing to oil prices. Elevated oil prices feed inflation expectations. When inflation expectations rise, bond investors demand higher yields to protect the purchasing power of future payments and that demand pressure drives up the 10-year Treasury yield. The 10-year Treasury drives mortgage rates. That’s the chain.

Nicole Rueth, senior vice president at The Rueth Team of Cross Country Mortgage, put it directly: “Geopolitics is driving everything right now in a way we haven’t seen in a while. Oil prices feed into inflation expectations, inflation expectations feed into the 10-year Treasury yield, and the 10-year drives mortgage rates.”

There’s no quick resolution to that chain. Anyone telling you otherwise is speculating.

The Fed Paused- But That’s Not the Disadvantage You Think It Is

As of early May 2026, the Federal Reserve has paused rates for the third consecutive meeting, holding the federal funds rate at 3.50%–3.75%. There’s no Fed meeting in May, which removes one potential short-term catalyst in either direction.

But here’s the thing most buyers fundamentally misunderstand: the Fed doesn’t set your mortgage rate. The federal funds rate is an overnight lending rate between banks. Your 30-year fixed mortgage operates on a completely different mechanism, and confusing the two is exactly how buyers end up waiting on the wrong signal.

The Puppet Master: Understanding the 10-Year Treasury

This is the most important concept in this entire article. If you understand this one thing, you’ll understand more about mortgage rate movement than most people in this business.

Your mortgage rate follows the 10-year U.S. Treasury yield – not the federal funds rate.

Lenders price the 30-year fixed mortgage at roughly 1.6% to 2.2% above whatever the 10-year Treasury yield is doing. The 10-year has been hovering around 4.2%–4.3% recently. Add the current spread of 2.05%–2.20%, and you land at 6.37%. It’s math, not mystery. The Richmond Federal Reserve has detailed research on exactly how this spread works, worth a read if you want to go deeper.

For the 30-year fixed to reach 5.5%, you’d need the 10-year to drop to around 3.3%–3.5% and the spread to normalize. That requires either a severe economic slowdown driving a massive flight to Treasury safety, a dramatic collapse in inflation expectations, or both happening simultaneously. None of that is on the near-term calendar.

“Higher for Longer” Is the Operating Reality

The Mortgage Bankers Association, Fannie Mae, and NAR are all projecting that 30-year rates will end 2026 in the 6.0%–6.5% range. Some optimistic scenarios put the low 6’s in play if inflation cools and the Fed resumes cutting. Morgan Stanley has penciled in a scenario where the 10-year could approach 3.75% by mid-2026, potentially pushing rates toward 5.50%–5.75%, but they also flag that rates could rise again in the second half.

The baseline? Mid-6’s for 2026, possibly into 2027. Plan accordingly.

Why 3% Rates Requires Something Catastrophic: Or Time Travel

I’m going to be straight with you here because I think this is the most misunderstood concept in the entire market right now. Buyers are waiting on 3% rates like they’re waiting on a bus that runs on a regular schedule. It doesn’t. It ran once, under conditions so extreme they may never repeat, and even if they did, you wouldn’t want to live through what caused them.

The Perfect Storm That Produced 2.97%

In December 2020, the 30-year fixed rate bottomed at 2.97%, the lowest number ever recorded in U.S. history. That number didn’t happen because the economy was thriving. It happened because four once-in-a-generation emergency interventions hit simultaneously, and the combination was unprecedented.

Emergency Action One: The Fed Cut to Zero

In March 2020, the Federal Reserve slashed the federal funds rate to 0%–0.25% in an emergency move triggered by COVID-19. The only other time in modern history this happened was during the 2008 financial crisis. This was a break-glass-in-case-of-emergency action, not a standard policy tool.

Emergency Action Two: $1.33 Trillion in Mortgage-Backed Securities Purchases

Between 2020 and 2022, the Federal Reserve purchased approximately $1.33 trillion in mortgage-backed securities, roughly 90% of the total MBS market growth during that period. By buying MBS at that scale, the Fed directly suppressed the yields investors required to hold those securities, which artificially collapsed mortgage rates to levels the market never would have produced on its own. This wasn’t a market phenomenon. It was a government intervention of extraordinary magnitude.

Emergency Action Three: Global Deflation Panic

In early COVID, global investors were genuinely terrified of deflation, the kind of sustained price decline that accompanies a deep depression. When deflation fears dominate global capital markets, money floods into U.S. Treasury bonds as the ultimate safe haven. That tidal wave of demand crushes Treasury yields, and mortgage rates follow. It takes a specific, severe kind of fear to produce that kind of movement.

Emergency Action Four: A Pandemic That Shut Down the Global Economy

COVID-19 triggered the sharpest GDP contraction since the Great Depression, vaporized tens of millions of jobs in weeks, and produced a scale of fiscal and monetary response without modern peacetime precedent. The 2.97% rate wasn’t a feature of a healthy market. It was a symptom of a global emergency.

As a widely shared comment from the r/RealEstate community put it: “You’re gonna need a DeLorean” to get back there. The most upvoted economic reply was equally direct: “Another complete global economic collapse requiring insane Fed stimulus.”

That’s not a market condition. That’s a catastrophe.

Waiting for 3% Rates Is Like Praying for a Hurricane

I want to sit here for a minute, because this is the framing I think every buyer in North Texas needs to internalize before they make another decision.

When a hurricane devastates a coastal town, something uncomfortable happens in the aftermath. Distressed sellers, people dealing with insurance chaos, structural damage, emotional exhaustion, sometimes let properties go at dramatically reduced prices. You could, technically, find a “deal” on beachfront real estate in the wreckage of a Category 4. The numbers might even look compelling on paper.

But nobody, and I mean nobody, is sitting in Houston in August thinking: “I really hope a major hurricane makes landfall so I can pick up some cheap waterfront property.”

That’s insane. Because the destruction required to produce the price drop would simultaneously destroy the power grid, the local economy, the insurance market, the lending environment, and the very coastal lifestyle the property was supposed to provide. The “deal” arrives packaged with everything that makes the deal worthless.

Waiting and hoping for 3% mortgage rates is the exact same logic.

Here’s what 3% rates actually require:

A deflationary global recession severe enough to send investors flooding into U.S. Treasuries as a safe haven, which collapses the 10-year yield, narrows the spread and brings mortgage rates down to emergency-era levels. That scenario means tens of millions of job losses, cratered consumer spending, and a lending environment so tight that the buyers who “finally” get their 3% rate are simultaneously facing stricter debt-to-income requirements, larger required down payments, and a banking system terrified of defaults.

The cheap rate arrives at the exact moment the door to qualifying for it gets significantly harder to walk through.

Then add the Federal Reserve’s required response. Getting rates that low means deploying emergency quantitative easing targeting mortgage-backed securities at a scale the Fed has only authorized once in modern history, when the alternative at the time looked like complete financial system collapse. That’s not a policy tool. That’s a “break-glass-in-emergency” intervention.

And even with all of that in motion: the recession, the deflation panic, the emergency QE, you’d still need the inflation regime of the 2020s to completely reverse course. The structural factors driving today’s inflation don’t evaporate in a quarter. They unwind over years, if they unwind at all.

So what does the buyer who “waits for 3%” actually get?

They get a rate that arrives packaged with job insecurity, tightened lending standards, potential income disruption, and a housing market that may have appreciated another 8%–15% in the window they spent waiting. The cheap rate comes with an expensive everything else and a personal financial position that may no longer qualify for it anyway.

The most dangerous thing in real estate isn’t a 6.37% rate. It’s a decision made on incomplete information, a mental model built on a number that existed for 18 months under conditions that required a global catastrophe to produce.

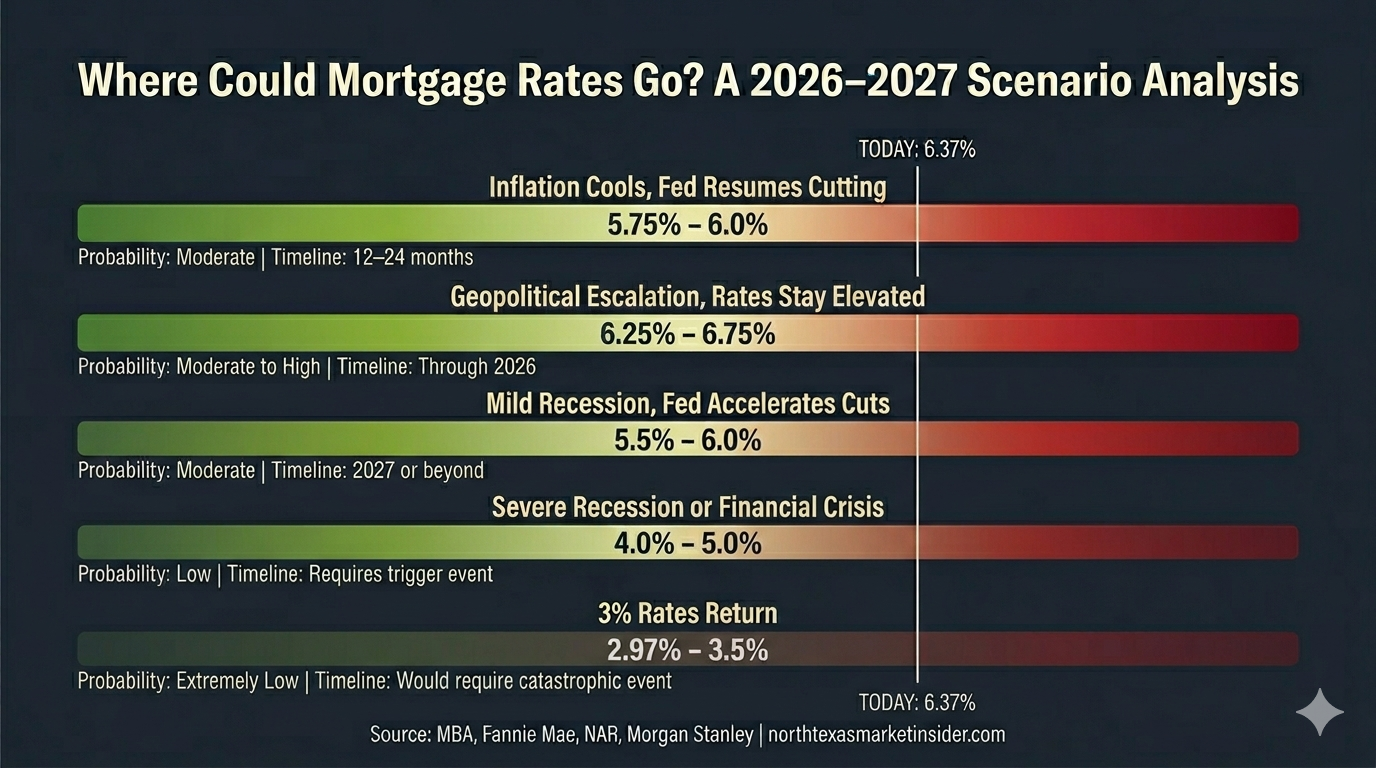

The Scenarios: What Would Actually Move Rates Lower

Let me walk through the realistic and less-realistic scenarios for rate movement, because this matters for your planning horizon. Understanding what would have to happen, and how likely each scenario is, is the intelligence edge that separates strategic buyers from reactive ones.

Scenario One: Inflation Cools, Fed Resumes Cutting (Optimistic Base Case)

This is the scenario most mainstream forecasters consider most likely over the next 12–18 months. If inflation continues its gradual decline toward the Fed’s 2% target, the Fed will resume rate cuts. Possibly one or two by late 2026. The 10-year Treasury drifts toward 3.75%–4.0%. Mortgage rates ease into the high 5’s, perhaps touching 5.75% in an optimistic version of this scenario by late 2026 or early 2027.

This scenario is plausible. It requires no catastrophe. It requires sustained inflation moderation, geopolitical de-escalation reducing oil price pressure, and a Fed that reads the data as permissive for easing. In this scenario, the buyer who purchased in May 2026 at 6.37% refinances in late 2026 or 2027 and wins on both sides. They’re locked in at a lower purchase price and then they captured the rate drop.

Probability: Moderate to low. Timeline: 12–24 months.

Scenario Two: Geopolitical Escalation Keeps Rates Elevated (Pessimistic Base Case)

If the U.S.-Iran conflict escalates further, oil prices remain elevated or climb higher, and inflation expectations stay stubborn, the Fed stays on pause through most of 2026. The 10-year Treasury holds near 4.3%–4.5%. Mortgage rates remain in the 6.25%–6.75% range through year-end. This isn’t a crisis scenario, rather it’s a continuation of the current environment, which buyers have already largely adapted to.

In this scenario, buyers who purchase now face no refinancing opportunity in the near term, but they also face continued price appreciation pressure in supply-constrained markets like Ellis County. The cost of waiting is measured in price appreciation, not rate savings.

Probability: Moderate to high near-term. Timeline: Through 2026.

Scenario Three: Mild Recession, Rates Drop to High 5s or Low 6s

A moderate economic slowdown, not a collapse, but a genuine contraction, could accelerate Fed easing and push the 10-year Treasury toward 3.5%–3.75%. In this scenario, mortgage rates could reach 5.5%–6.0%. The trade-off: job market softening, tighter lending standards, and potential income disruption for some buyers. In a recession scenario, the buyers best positioned to act are those with stable employment, strong credit, and sufficient reserves. Not the buyers who were already stretched at 6.37%.

This scenario is worth planning for, not panicking about. If your employment is stable and your financial position is solid, a mild recession actually creates a buying window in markets where prices soften temporarily.

Probability: Moderate over 18–36 months. Timeline: 2027 or beyond.

Scenario Four: Severe Recession or Financial Crisis, Rates Drop to 4%–5%

A severe economic contraction(think 2008-level disruption) could push the 10-year Treasury toward 2.5%–3.0% and bring mortgage rates to the 4%–5% range, depending on Fed response. This scenario requires significant economic pain: widespread job losses, financial market disruption, and a housing market that’s simultaneously more affordable by rate and less accessible by lending standard. Most buyers who are waiting for this scenario haven’t thought through what their own financial position looks like in it.

Probability: Low near-term. Requires a trigger event that isn’t currently visible.

Scenario Five: 3% Rates Return (Catastrophic Scenario)

As detailed above, this requires a confluence of emergency conditions: $0 Fed funds rate, $1 trillion+ in MBS purchases, global deflation panic, and an economic contraction severe enough to produce all three simultaneously. Every mainstream forecaster considers this a tail risk, not a planning scenario. The CBS News analysis of what would drive mortgage rates lower is consistent with this read: the conditions required are extraordinary, not cyclical.

Probability: Extremely low. Would require a catastrophic and unprecedented economic event.

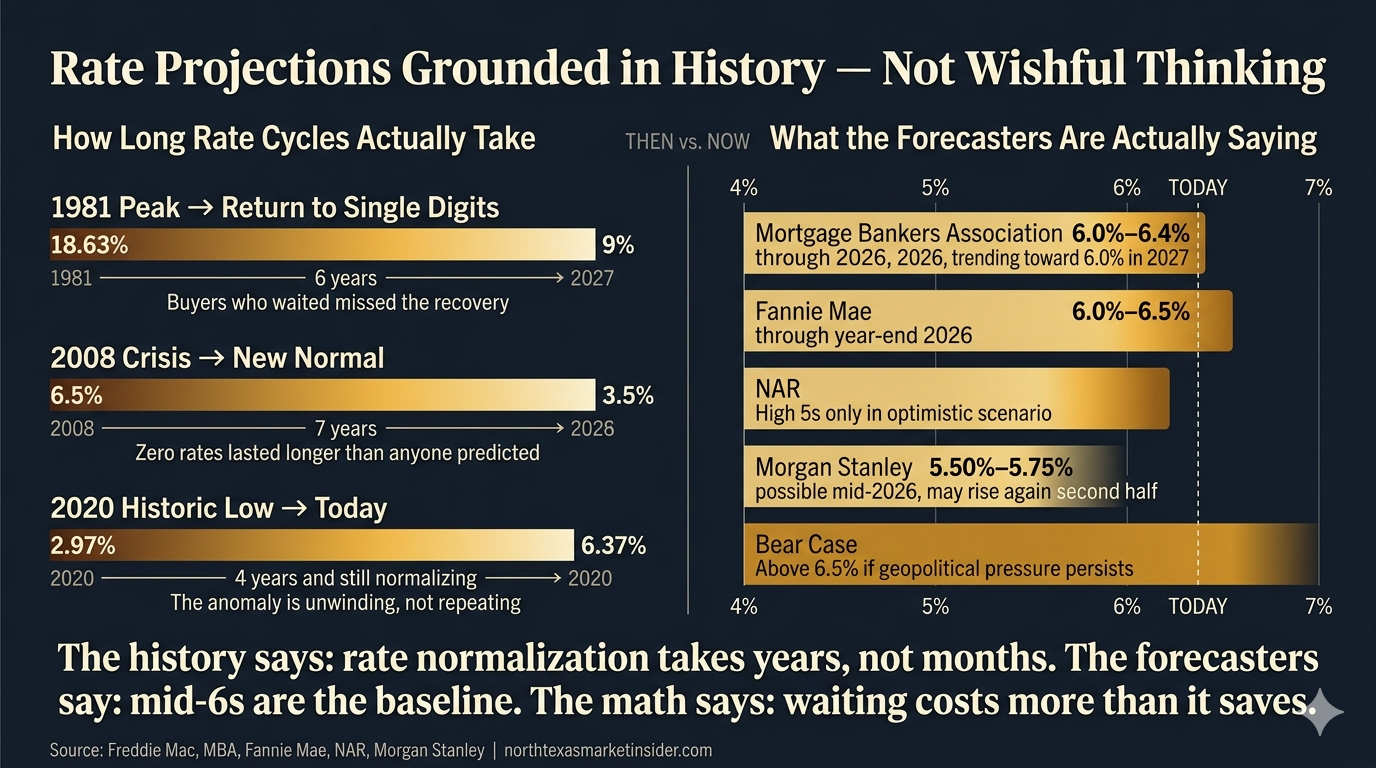

The 50-Year History of Mortgage Rates That Nobody Shows You

Here’s the reframe that changes everything.

Most buyers who are waiting for rates to “come back down” are operating on a sample size of one. They bought, or watched their friends buy, during the 2020–2021 window when 30-year fixed rates were sitting at 2.97%–3.5%, and that number became their mental baseline for what a mortgage rate is supposed to be. Everything above it feels wrong. Everything above it feels like paying too much.

That’s not a market analysis, that’s a reference point built on the single most anomalous rate environment in American history.

Let me show you the full picture.

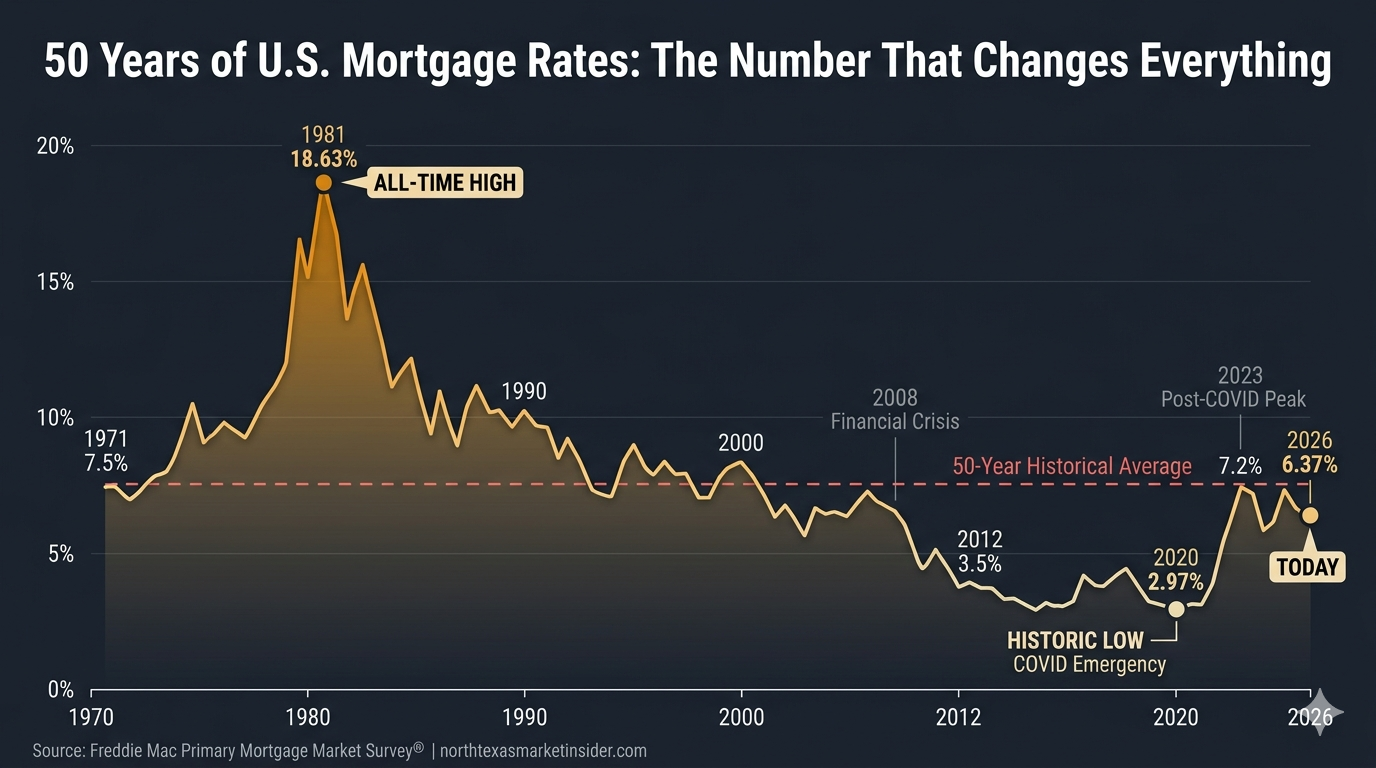

In 1981, the 30-year fixed-rate mortgage averaged 18.63%, the highest ever recorded in U.S. history. That wasn’t a blip. Rates stayed above 10% for most of the decade as the Federal Reserve, under Chairman Paul Volcker, deliberately engineered a recession to break the back of 1970s stagflation. Buyers in that era weren’t debating whether to wait for 6%. They were calculating whether they could survive 17%.

Through the 1990s, mortgage rates averaged between 8% and 10%. The economy was growing, consumer confidence was rising, and the housing market was healthy and active, all with rates that would make today’s buyers faint. The families who bought in 1994 at 9.2% didn’t wait for a better number. They bought the house, built the equity, and refinanced when conditions improved.

Through the 2000s, before the financial crisis, rates averaged 6% to 7%. Sound familiar? The pre-crisis housing boom, the one that produced some of the strongest appreciation numbers in modern history, happened almost entirely in a rate environment that looks nearly identical to where we are right now.

Then came 2008. The financial crisis triggered an emergency Fed response, rates cut to zero, quantitative easing deployed at scale and the country entered what many economists called the “new normal” of 3.5%–5% rates that lasted from roughly 2012 through 2019. That seven-year window conditioned an entire generation of buyers to expect rates that were, by any historical measure, extraordinarily cheap.

And then 2020 happened. The confluence of zero Fed funds rate, $1.33 trillion in MBS purchases, global deflation panic, and pandemic-level economic disruption pushed rates to 2.97%, a number that had never existed before in the recorded history of the American mortgage market.

Here’s what all of that history adds up to:

The 50-year average for the 30-year fixed-rate mortgage is approximately 7.7%.

Read that again. The long-run average; across booms, recessions, crises, and recoveries is 7.7%. Today’s rate of 6.37% is not historically high. It is historically below average. The anomaly wasn’t 2026. The anomaly was 2020. Buyers who are waiting for the anomaly to return are waiting for something that required a global catastrophe to produce the first time and has never happened under any other conditions.

That’s not pessimism. That’s the data. And the data says that 6.37%, in the context of 50 years of mortgage rate history, is a completely normal place to buy a home.

The Federal Reserve’s Rate Cycle and What It Actually Tells Us

Understanding where rates are going requires understanding how we got here, because the Fed’s decision-making pattern over the last four years is one of the clearest maps we have for what comes next.

In March 2020, the Federal Reserve cut the federal funds rate to 0%–0.25% in an emergency response to COVID-19. This was the second time in modern history the Fed had deployed a zero rate, the first was during the 2008 financial crisis. Alongside that rate cut, the Fed launched its quantitative easing program, purchasing Treasury bonds and mortgage-backed securities at a pace that had no modern precedent. The goal was simple: flood the system with liquidity, suppress borrowing costs, and prevent economic collapse.

It worked, arguably too well. By 2021, with stimulus checks flowing, supply chains disrupted, and demand surging, inflation began climbing. The Fed initially characterized it as “transitory.” It wasn’t.

By March 2022, with inflation running at 40-year highs, the Fed began one of the most aggressive rate-hiking cycles in its history. Over the next 18 months, the federal funds rate rose from 0.25% to 5.25%–5.50%, an increase of 525 basis points in approximately 16 months. Mortgage rates, which had already begun rising in anticipation of Fed action, climbed from their historic lows to above 7% by late 2022 and into 2023.

Here’s the part most buyers miss: mortgage rates peaked before the Fed stopped hiking. The bond market had already priced in the end of the tightening cycle and began easing yields before the Fed made a single cut. This is the lag dynamic that makes watching Fed announcements a lagging indicator for mortgage rate direction. The bond market is always looking forward, never at what the Fed did last month.

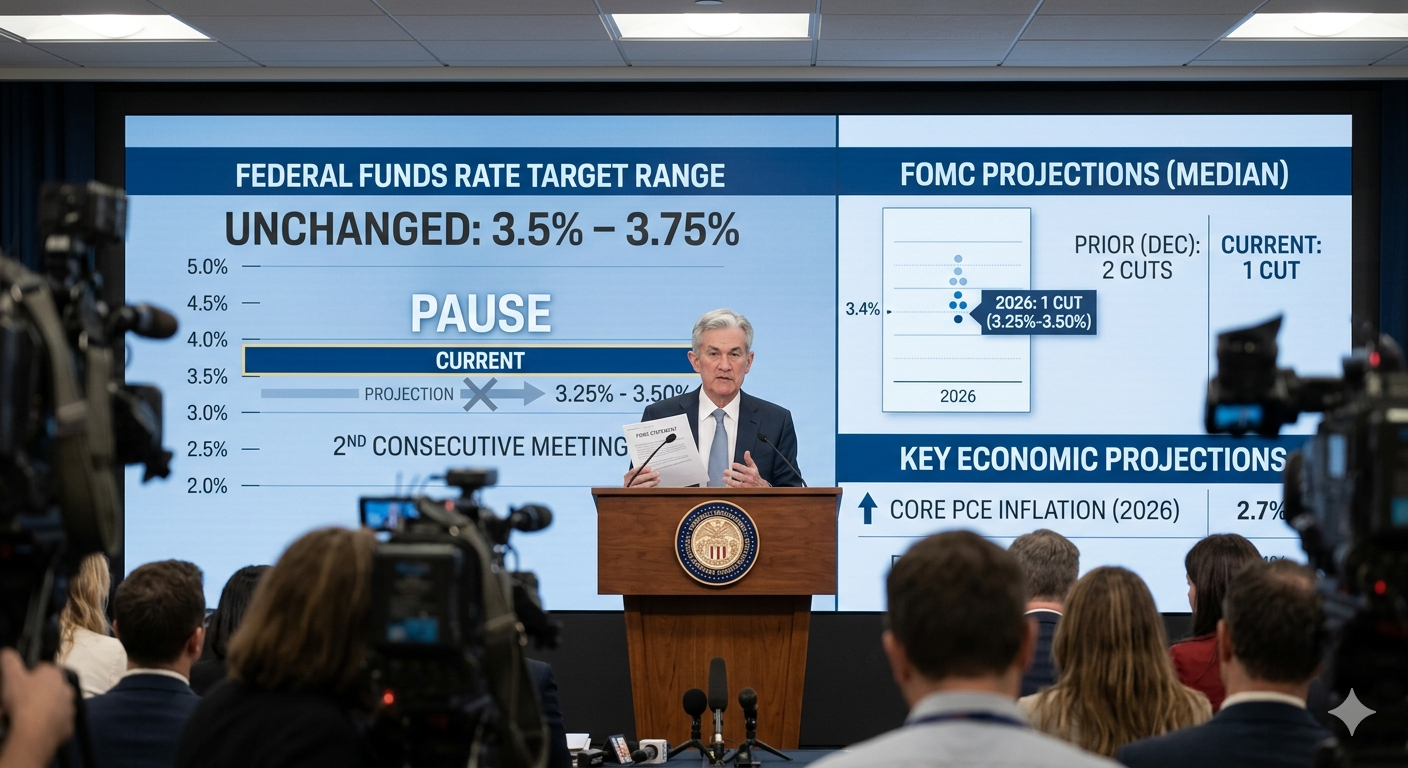

The Fed began cutting rates in late 2024, and by early 2026 had brought the federal funds rate down to its current 3.50%–3.75% level. A significant reduction from the peak, but still well above the emergency-era zero. The Federal Open Market Committee has now paused for three consecutive meetings, signaling that they believe the current rate level is appropriate for the current inflation environment, neither stimulative nor restrictive enough to force further cuts.

What does this tell us about where rates go from here?

The Fed’s own projections, the “dot plot” released after each quarterly meeting, have consistently shown a gradual, measured path toward rate normalization, not a rapid return to emergency-era levels. The Fed is not signaling zero. It’s not signaling 1%. It’s signaling a long, slow walk toward a neutral rate that most economists peg somewhere in the 2.5%–3.5% range for the federal funds rate. Which, given the current spread dynamics, translates to mortgage rates in the 5.5%–6.5% range in a normalized environment.

That’s the honest read from the Fed’s own guidance. Not 3%. Not 4%. A gradual drift toward the mid-to-high 5s over a multi-year horizon, but only if the inflation data cooperates.

And if it doesn’t cooperate: if geopolitical pressures keep oil elevated, if services inflation stays sticky, if the labor market remains tighter than the Fed’s models expect, then the pause extends, the cuts get pushed out, and the mid-6’s become the operating environment for longer than most buyers are currently planning for.

The strategic implication is direct: waiting for the Fed to rescue your mortgage rate is waiting for a process that moves slowly, unpredictably, and in response to data that hasn’t been generated yet. The buyers who win in this environment are the ones who stop waiting for the Fed and start building a strategy around the rate environment that actually exists.

Rate Projections Grounded in Historical Patterns – Not Wishful Thinking

Forecasting mortgage rates is an exercise in humility. The institutions with the most sophisticated models in the world; the Fed, Fannie Mae, the Mortgage Bankers Association, have all consistently missed rate movements by meaningful margins in both directions. Anyone who tells you with certainty where rates will be in 18 months is selling you something.

What historical patterns can tell us is how long rate normalization cycles typically take and that timeline should inform every buyer’s planning horizon.

After the 1981 peak at 18.63%, it took six years for rates to fall back to 9%. Six years of buyers waiting, debating, and ultimately purchasing anyway because life doesn’t pause for rate cycles. The families who bought in 1983 at 13% refinanced in 1987 at 9% and called it a win.

After the 2008 financial crisis, the Fed held rates near zero for seven years from 2008 through 2015. Mortgage rates during that window gradually declined from around 6% to the 3.5%–4% range, but the decline was slow, uneven, and punctuated by multiple periods where rates rose before falling again. Buyers who waited for the “perfect” rate in 2009 were still waiting in 2012 while prices in recovering markets climbed steadily.

The post-COVID normalization has now been underway for four years and isn’t finished. Rates climbed from 3% to above 8%, then moderated to the current 6.37%. That moderation has taken the better part of two years and has been anything but linear. Rates have moved up and down multiple times within the broader downtrend, punishing buyers who tried to time the market at specific moments.

The pattern across all three cycles is consistent: rate normalization takes longer than buyers expect, moves less smoothly than models project, and rewards the buyer who purchases within an acceptable range rather than the one who holds out for a specific number.

So where are rates likely heading? Here’s the range of credible projections from major forecasters as of May 2026:

The Mortgage Bankers Association projects the 30-year fixed ending 2026 near 6.4% and gradually declining toward 6.0% through 2027 as inflation moderates and the Fed resumes measured cuts. The Fannie Mae Economic and Strategic Research Group holds a similar view, projecting rates in the 6.0%–6.5% range through year-end with modest improvement in 2027. NAR’s forecast aligns with the consensus, projecting the high 5s as a realistic target only in an optimistic scenario where inflation surprises to the downside.

The most bullish credible scenario came from Morgan Stanley strategists and it projects the 10-year Treasury reaching approximately 3.75% by mid-2026, which would push mortgage rates toward 5.50%–5.75% in that window before potentially rising again in the second half of the year.

The most bearish credible scenario keeps rates above 6.5% through 2026 if geopolitical pressures persist and the Fed is forced to hold or reverse course.

Notice what’s missing from every credible forecast: 3%. Notice what’s present in all of them: a range that looks a lot like where we are right now, with modest improvement over a multi-year horizon.

Here’s what that means for your decision. If you’re a buyer planning to hold your home for five or more years, which is the minimum horizon for a sound real estate purchase in any rate environment, the difference between buying today at 6.37% and buying in 18 months at a hypothetical 5.75% is approximately $120–$150 per month on a $350,000 loan. That gap closes further when you account for potential price appreciation in the interim. And it closes completely if rates don’t cooperate with the optimistic forecast and you end up buying at 6.25% anyway after 18 months of waiting.

The history says: normalize your expectations, build your strategy around the rate environment that exists, and use every available tool including buydowns, concessions and builder incentives to optimize within that environment. That’s what sophisticated buyers do and that’s what my clients do.

What This Means for North Texas: The Ellis County and DFW Reality

Here’s where I shift from national context to the market I actually operate in every day, because the national rate story and the North Texas opportunity story are two different conversations, and most agents only tell you one of them.

The Relocating Buyer Has a Window Right Now

The volume of buyers relocating to North Texas from California, Colorado, Washington, and Arizona is not stopping because mortgage rates are at 6.37%. When you’re selling a $900,000 house in California or Colorado and buying a $450,000 home in Waxahachie or Midlothian, a 6.37% mortgage on a smaller principal is still a dramatic improvement in monthly cash flow, total debt load, and net worth position. The spread between what they’re leaving and what they’re landing in is the opportunity and that spread is substantial.

The buyers who understand this are moving. The ones who don’t are still searching “when will mortgage rates drop” at 11pm.

Ellis County Inventory Is Still Lean Enough That Waiting Has a Real Cost

Here’s the North Texas-specific dynamic that national rate headlines completely ignore: inventory in Ellis County, i.e. Waxahachie, Midlothian, Red Oak, Ennis, Ferris, Palmer, is not sitting around waiting for buyers to get off the fence. The region’s growth trajectory, driven by I-35E corridor development, corporate relocations to the south DFW suburbs, and continued migration from higher-cost metros, keeps demand structurally elevated even as rates moderate buyer enthusiasm.

Waiting for lower rates doesn’t just mean waiting for lower payments. It means waiting in a market where prices have a structural upward bias, where the best new construction communities sell out phases before they’re framed, and where the family who locked in twelve months ago at a slightly higher rate is now sitting on equity while the family that waited is competing for the same inventory at a higher price point.

Rate sensitivity is real. But it has to be weighed against price trajectory and in this corridor, the trajectory argument is compelling.

The Infrastructure Argument Nobody Else Is Making

Most agents talk about current inventory and current rates. I track what’s coming before it becomes current, because that’s where the real advantage lives.

The I-35E corridor through Ellis County is not finished developing. The commercial and industrial announcements in and around Waxahachie, Midlothian, and the broader Ellis County corridor over the last 24 months represent a wave of employment base expansion that feeds housing demand for years, not quarters. When major employers announce and then open their doors, the surrounding residential market tightens further. The buyers who are already positioned in those communities when that happens are the ones who bought before the demand wave priced them out.

This is five-steps-ahead thinking. Not waiting for the wave to arrive.

New Construction Buyers Have Tools the Resale Market Doesn’t

One thing I track closely in Ellis County and the broader South DFW to Waco corridor is what builders are doing with their incentive structures when rates climb. Right now, national builders operating in this market are buying down rates, offering closing cost contributions, and in some cases locking qualified buyers into temporary rate buydowns that materially change the monthly payment math. I’ve seen effective rates in the mid-5s on builder-to-buyer transactions when all available incentives are stacked correctly.

That’s not magic, it’s market mechanics. Builders need to move inventory to fund the next phase. When the resale market slows, they compete and with much deeper pockets than your typical resale home seller. Buyers who understand how to access and stack those incentives have options that pure resale buyers don’t. This is exactly the kind of intelligence I make sure my clients have before they walk into a sales office.

Ten Strategies That Actually Work in a 6%+ Rate Environment

This isn’t a list of platitudes. Every one of these is actionable right now, in this market, for buyers and sellers in Ellis County and DFW.

1. Stop watching the Fed announcement and start watching the 10-year Treasury.

Set up a basic alert for the 10-year Treasury yield. When it moves, your mortgage rate is about to move. You’ll have information ahead of the headlines.

2. Get pre-approved now, before conditions change.

A current pre-approval gives you an accurate baseline and positions you to move when the right property appears. It also forces the rate conversation to happen with a real lender running real numbers, not your flawed Zillow estimate. My preferred lending partners know this market inside and out: Denise Donoghue at The Mortgage Nerd (yourmortgagenerd.com), Andrew Bryan at Miramar Mortgage (miramarmortgage.com), or Ethan Hester at Midtex Mortgage (mid-texmortgage.com). These are the lenders I trust with my clients because they have the product depth and the North Texas market context to actually help.

3. Understand the buydown math before you dismiss it.

A 2-1 temporary buydown, where your effective rate is 2% below the note rate in year one and 1% below in year two before resetting, can dramatically change the affordability calculus in the hardest financial years of a new purchase. If you’re planning to refinance when rates drop anyway, the buydown gives you payment relief in the window before that refinance happens.

4. Think about the refinance as part of the purchase strategy, not a separate future event.

If rates reach the mid-to-low 5s over the next 18–24 months, which a handful oc forecasters consider plausible, the buyer who purchased today at 6.37% refinances and wins on both ends. They locked in a price before potential appreciation, then captured the rate drop. The buyer who waited paid the sale higher price and likely has a higher monthly payment.

5. Run the total cost of ownership math, not just the monthly payment.

At 6.37% on a $350,000 home with 10% down, your principal and interest payment is roughly $1,970/month. If waiting 18 months produces a 5.75% rate but the home has appreciated to $375,000, your new payment is approximately $1,972/month, essentially identical. Most buyers aren’t running this number, but they should be.

6. For sellers: price precision is the strategy, not price reduction.

In a 6%+ rate environment, buyers are payment-sensitive in ways they weren’t at 3%. Overpricing a listing and chasing it down with reductions is a slower, more expensive version of just pricing it right from day one. Right-priced properties in Waxahachie and Midlothian are still moving. Overpriced ones are sitting, accumulating days on market, and eventually selling for less than a precise day-one price would have captured.

7. Explore the seller concession conversation on every offer.

In a normalized market, sellers have more flexibility on concessions than they did during peak competition. Sellers can contribute toward closing costs, rate buydowns, and prepaid items; all of which reduce your out-of-pocket and effective rate without requiring the seller to dramatically cut their net price. This is a negotiation conversation worth having on every offer right now.

8. Stack new construction incentives.

If you’re open to new construction, and in Ellis County, you really should consider it, learn to stack builder incentives. Rate buydowns plus closing cost contributions, plus design center credits can meaningfully reduce the true cost of entry on a new build versus a comparable resale. I help clients navigate this conversation every week, and the difference in effective payment can be significant.

9. Don’t let the national narrative override the local opportunity.

National rate headlines drive national sentiment. But your opportunity is hyperlocal. The specific dynamics of Waxahachie, of Midlothian, of Red Oak, and the communities coming soon along Highway 287, these are not reflected in a national media rate story. Local intelligence is what produces local advantage.

10. Talk to someone who actually knows this market.

This sounds obvious, but it’s remarkable how many people are making six-figure financial decisions based on national media coverage and algorithm-generated estimates. A conversation with an agent who tracks Ellis County permit filings, new community launches, price movement by subdivision, and local absorption rates changes your decision-making calculus.

FAQ: The Most Asked Most About Interest Rates

Q: Should I wait for lower rates before buying in North Texas?

That depends on your specific situation — timeline, financial position, price point, and how long you intend to hold the property. But as a general framework: if you’re buying a home you plan to own for five or more years in a market with a structural growth tailwind, waiting on rate relief that may not arrive on your timeline while prices continue moving means trading a rate problem for a price problem. One you can refinance. The other you can’t.

Q: Will rates come back to 3%?

Almost certainly not without a catastrophic economic event. It would be one you definitely don’t want to live through. Every major housing economist projects mid-6s through 2026 and likely into 2027, with some optimism around high 5s in the right macro scenario. See the hurricane section above.

Q: How does the 10-year Treasury affect my mortgage rate?

Lenders price 30-year mortgages at roughly 1.6%–2.2% above the 10-year Treasury yield. When the 10-year moves, mortgage rates follow, usually within days. Watch the 10-year if you want real-time leading indicators on where your rate is heading.

Q: What’s the Fed actually doing and why does it matter?

The Fed paused for a third consecutive meeting, holding the funds rate at 3.50%–3.75%. But the federal funds rate doesn’t directly set your mortgage rate, the 10-year Treasury is the more direct signal to watch. Waiting on a Fed announcement to tell you where mortgage rates are heading is watching the wrong scoreboard.

Q: Is it a good time to buy in Waxahachie specifically?

I track this market more closely than anyone in it. Waxahachie has infrastructure investment, population growth, quality school districts, and a price point that still makes sense for in-state and out-of-state buyers. The question isn’t whether the market is positioned well — it is. The question is whether your personal timeline and financial position align with this moment. That’s a conversation worth having directly.

Q: Are builders offering rate incentives right now?

Yes. Multiple national builders operating in Ellis County and south DFW have active rate buydown programs, closing cost contributions, and design center incentives. The specific terms change regularly and vary by community and phase. I track these actively because the right incentive stack can change the effective payment math significantly.

Q: What’s the difference between a rate buydown and a rate lock?

A rate lock protects you from upward movement during your transaction window, typically 30 to 60 days. A rate buydown actually lowers your effective rate, either temporarily (2-1 buydown) or permanently (paying points at closing). These are different tools for different situations. Denise Donoghue, Andrew Bryan, and Ethan Hester are excellent resources for modeling both scenarios.

Q: What happens to North Texas home prices if rates stay elevated?

In markets with structural demand tailwinds like population growth, employment base expansion, infrastructure investment and net in-migration, elevated interest rates moderate the pace of appreciation but don’t necessarily produce price declines. Ellis County falls into that category. Flat to modest appreciation is more likely than correction in my read of this market.

Q: Should sellers be worried about 6%+ rates?

Sellers should be strategic, not worried. Right-priced homes are still selling. The market has adjusted to this rate environment and buyers have recalibrated their expectations, payment tolerance, and strategy. What sellers need is an agent who understands where the buyer pool is, what concessions make sense, and how to price precisely for current conditions. Data-based pricing is working right now. Emotion-based pricing is not.

Q: How do I get started?

Call me at 214-228-0003 or schedule a consultation. Whether you’re buying, selling, relocating from out of state, or just trying to understand what this market is actually doing, that’s what the North Texas Market Insider™ is built for.

The Strategic Take: What Prepared Buyers and Sellers Do Right Now

Here’s where I land on all of this and this is my read, not a consensus opinion.

The 6.37% rate environment is not a crisis. It’s a sorting mechanism. It separates buyers who understand the market from buyers who are waiting on a number they saw in 2020. It separates sellers who price with precision from sellers who price with hope. It separates agents who deliver intelligence from agents who deliver generic advice wrapped in enthusiasm.

The North Texas corridor from South DFW down through Ellis County to the Waco region has structural growth drivers that most rate environments can’t erase. Corporate relocations, population migration, infrastructure investment and housing supply that still haven’t caught up with long-term demographic demand. That’s the ground-level reality I see from inside this market every day.

The prepared client in this environment doesn’t wait. They get informed, they get pre-approved andthey understand the tools available to them such as rate buydowns, builder incentives and seller concessions. They make decisions based on their specific position and timeline, not on a national media headline.

That’s the intelligence play. And that’s exactly what I’m here to help you execute.

Prefer to talk through your specific situation? Reach out directly.

Bobby Franklin, REALTOR® | North Texas Market Insider™

Legacy Realty Group – Leslie Majors Team

📲 214-228-0003 | northtexasmarketinsider.com

Preferred Lenders (RESPA Disclosure: I recommend these lenders based on their expertise and service. I do not receive compensation for referrals.)

- Andrew Bryan — Miramar Mortgage

- Jennifer Nelson — Eustis Mortgage

- Taylor Fruge — Lower Mortgage

This content is for informational purposes only and does not constitute financial, legal, or investment advice. All real estate transactions involve risk. Consult with a licensed professional before making any financial decisions. Bobby Franklin is a licensed Texas REALTOR® with Legacy Realty Group – Leslie Majors Team. Equal Housing Opportunity.