By Bobby Franklin, REALTOR® | North Texas Market Insider™ | Legacy Realty Group – Leslie Majors Team | Serving Ellis County, DFW & Greater North Texas | 214-228-0003 | northtexasmarketinsider.com

Most agents are about to spend the next thirty days posting daffodil emojis and “spring market is heating up!” graphics. I’m going to do something different. I’m going to tell you exactly what just happened in March, what it means for your house in DFW, your relocation from California, your first purchase in Red Oak, or your investment play in Whitney, TX and we’ll cover what the move is right now while everyone else is still trying to figure out if the war is over.

Because here’s the truth nobody in this business wants to say out loud: March 2026 was the most consequential month for North Texas housing in two years, and 90% of buyers and sellers will completely miss what it actually meant. That’s not a tragedy. That’s an opportunity. For you, and for the clients I work with every single day.

Let’s get into it.

The 30-Second Insider Read

Before we go deep, here is the headline:

The U.S.-Israeli strikes on Iran on February 28 detonated a chain reaction that ran straight through the bond market and into your mortgage payment. Rates went from a three-year low of 5.99% to a six-month high of 6.61% in about five weeks. The Fed held rates steady 11-1 and quietly opened the door to raising rates if inflation re-accelerates. National inventory hit a 29-month growth streak. DFW listings are up around 20% year-over-year. Days on market in the metro pushed to 48. Sellers are cutting prices in droves — over 8,000 DFW listings dropped their ask in March alone. Then on April 7, a two-week ceasefire was announced, oil tanked 15%, the Dow ripped 1,300 points, and the rate environment started reversing in real time.

Translation: chaos. Real, structural, market-moving chaos. And exactly the kind of chaos that rewards the prepared and punishes the passive.

Here’s a video version of what I am going to walk you through. (Keep scrolling to read more below)

Table of Contents

- The Iran War and Your Mortgage Payment: The Chain Reaction Nobody Explained to You

- The Fed’s March Meeting: What Holding 3.50–3.75% Actually Signals

- Mortgage Rate Whiplash: 5.99% to 6.61% in Five Weeks

- National Inventory: 29 Straight Months of Growth and What It Means Locally

- Home Prices in March: Why “National Headlines” Are Lying to You About DFW

- Days on Market: The Single Most Honest Metric in This Market

- North Texas County by County: The Real Map

- New Construction in DFW: The Builder Incentive Window Is Wide Open

- First-Time Buyers in 2026: You Are Not Locked Out — You Are Being Underserved

- Sellers: The 2021 Playbook Is Dead. Here Is the 2026 One

- The Road Ahead: Three Scenarios, One Strategy

- The Insider FAQ: 10 Questions Buyers and Sellers Are Actually Asking

1. The Iran War and Your Mortgage Payment: The Chain Reaction Nobody Explained to You

On February 28, 2026, the United States and Israel launched coordinated military strikes against Iran. Within 72 hours, oil prices were ripping higher, Treasury yields were climbing, and the mortgage market, which had been quietly drifting toward sub-6%, got slapped sideways.

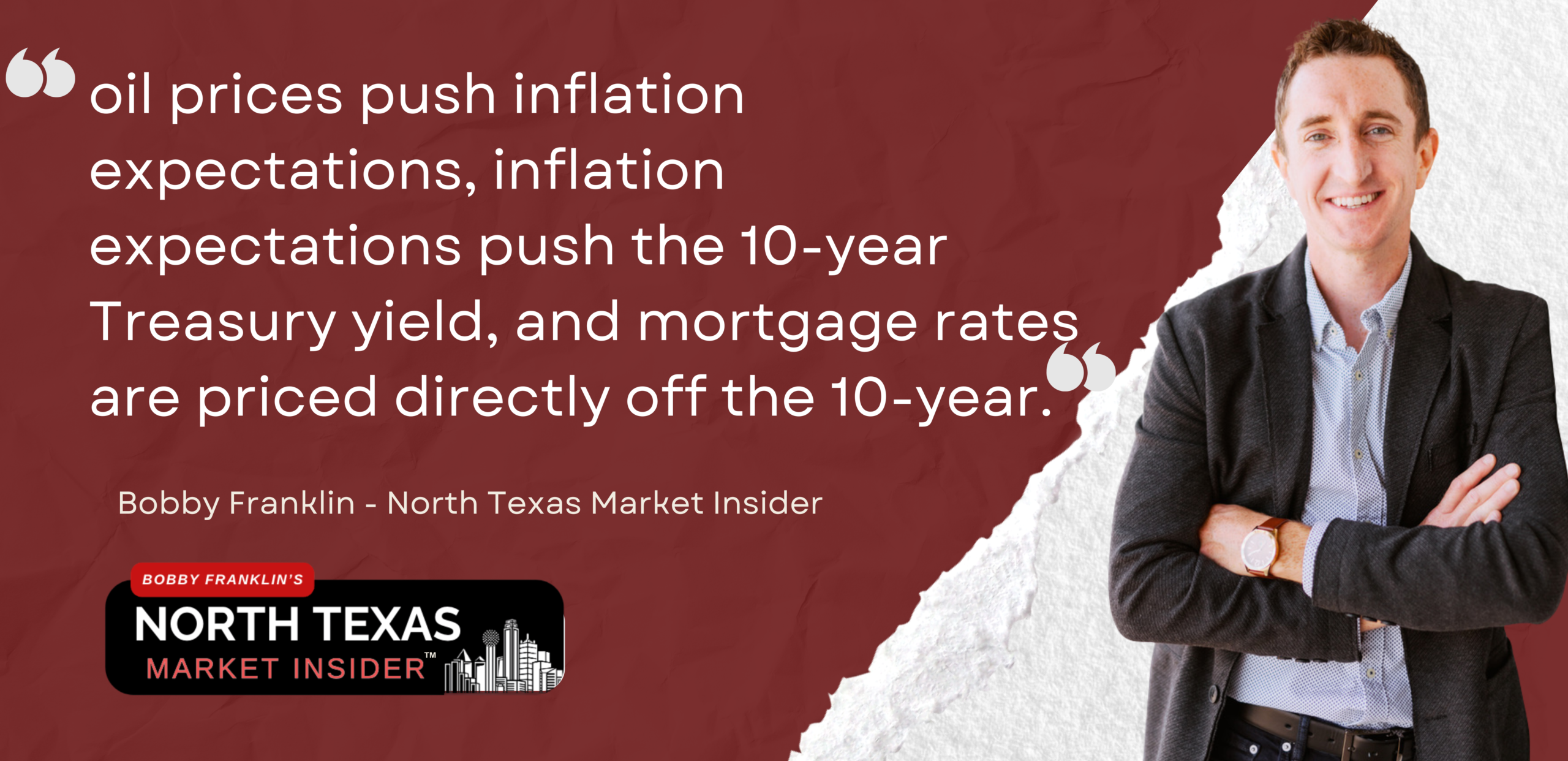

Here is the chain reaction. Memorize this, because every other “market update” you read this spring is going to skip it: oil prices push inflation expectations, inflation expectations push the 10-year Treasury yield, and mortgage rates are priced directly off the 10-year. When a region that supplies a meaningful share of global crude becomes a war zone, the bond market doesn’t wait for the data. It prices in the inflation risk immediately. Your mortgage rate moves before the first oil tanker even reroutes.

Look at the numbers:

- February 27: the average 30-year fixed mortgage was sitting at 5.99%, the lowest level since September 2022, according to Redfin’s mortgage rate tracker.

- March 20: that same average had vaulted to 6.53% – a six-month high.

- March 27: the Freddie Mac weekly survey clocked in at 6.38%, the fourth consecutive weekly increase since the strikes.

- March 31: Bankrate had the 30-year fixed at 6.61%.

Construction got hit too. Materials costs climbed 15% to 39% year-over-year, according to ManageCasa’s analysis of the Iran conflict’s impact on U.S. property. The Census Bureau then dropped a brutal print: new home sales fell 17.6% in February from January’s adjusted annual rate of 712,000. Builders felt it before buyers did, and they started moving fast. Which, as I’ll show you in section 8, is exactly the window strategic buyers should be exploiting.

Mortgage applications cratered. The Mortgage Bankers Association reported a 10.4% drop in seasonally adjusted application volume in the last week of March, with refinances tumbling 14.6%. MBA’s Joel Kan put it plainly: rising rates + affordability stress + economic uncertainty pushed buyers back to the sidelines.

Then came April 7. President Trump announced a two-week ceasefire with Iran. Oil dropped more than 15%. The Dow ripped 1,300 points. The 10-year Treasury yield slid. Realtor.com’s senior economist Joel Berner said the ceasefire instantly began reversing the wartime trend in mortgage pricing.

Is the ceasefire going to hold? Unfortunately, it didn’t. But here is the Insider read: the buyers and sellers who position themselves while the rest of the market is paralyzed by the headlines are the ones who win this quarter. I broke part of this down in my earlier piece on why the Fed’s March pause was actually the green light to sell in North Texas. Go read that next, because it will fill in the gaps with this report.

2. The Fed’s March Meeting: What Holding 3.50–3.75% Actually Signals

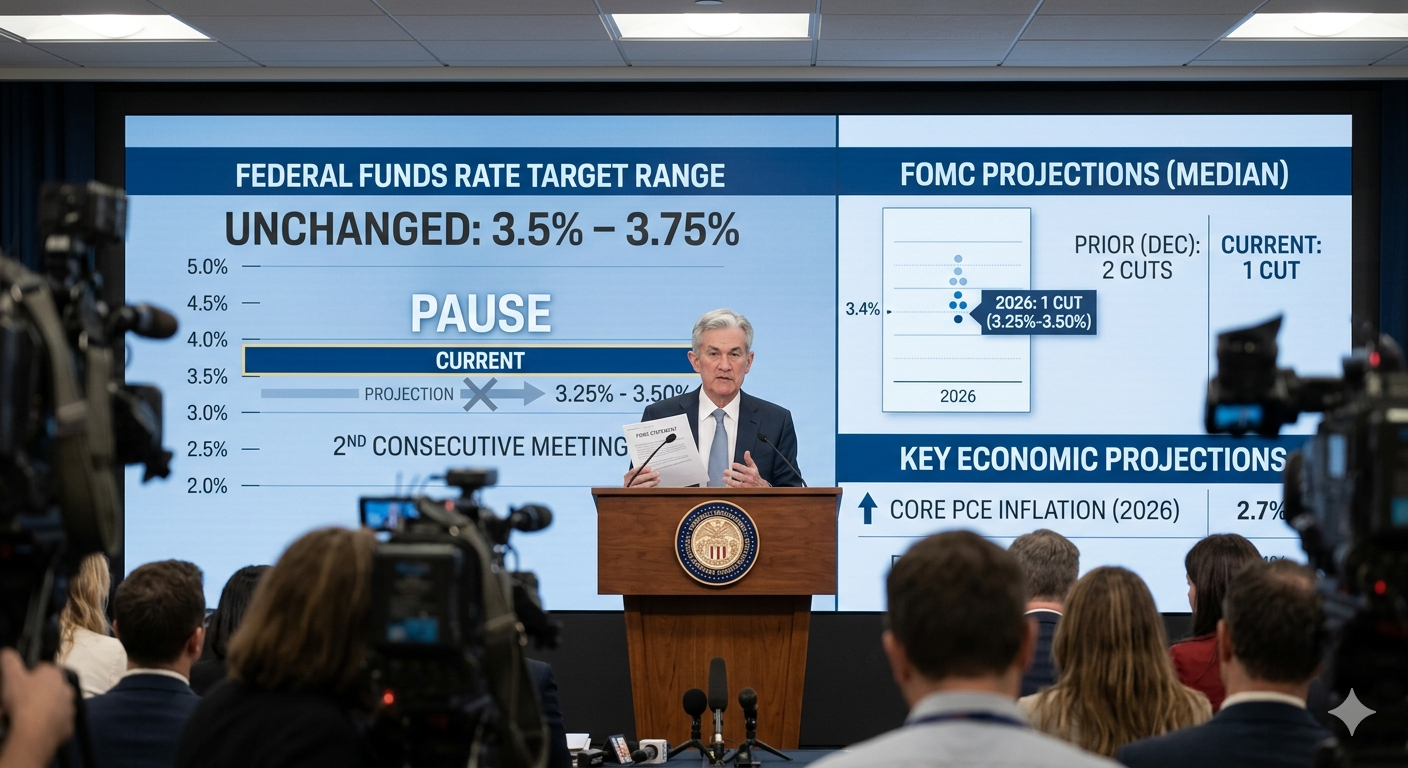

The Federal Open Market Committee met March 17–18 and voted 11 to 1 to hold the federal funds rate steady at 3.50%–3.75%. Fed Governor Stephen Miran was the lone dissent, he wanted a 25 basis point cut, citing labor market concerns. Governor Christopher Waller, who had voted to cut in January, flipped and voted to hold this time. That flip sums up the entire story of how much the Iran shock changed the Fed’s calculus in six weeks.

Chair Jerome Powell told the press the economy was “doing pretty well,” but the real signal was in the updated dot plot, the chart that shows where each committee member sees rates going. The committee now projects one cut in 2026 and one in 2027. Before the war, the consensus was two cuts this year. According to Reuters’ coverage of the FOMC minutes released April 8, some members are now openly discussing whether rate hikes might be necessary if Iran-driven inflation sticks above target.

Read that sentence again. We went from “two cuts in 2026” to “we might have to hike” in six weeks. That is the chaos I keep talking about, and that is why “wait and see” is the worst strategy in real estate this spring.

Here is the plain English version for North Texas buyers and sellers:

The Fed does not set your mortgage rate. Stop waiting for Powell to do something that fixes your closing costs. The federal funds rate controls overnight lending between banks. Your 30-year fixed is priced off the 10-year Treasury, which moves on inflation expectations and Fed policy outlook, not the actual rate.

Sub-5% rates in 2026 are a fantasy. Even the most optimistic forecast calls for one quarter-point cut this year. If you’re sitting on the sidelines waiting for a 4.99% rate to text you, you’re still going to be sitting there in 2027, watching home prices across the metroplex grind higher around you.

Stability is a gift to sellers. The worst thing for a seller is a sudden rate spike that vaporizes buyer demand overnight. The Fed holding steady prevents that. It is the closest thing to a green light this market is going to give you.

Buyers still have real tools. Builder buydowns, seller concessions, and assistance programs are stacking up and I’ll show you exactly how to use them in sections 8 and 9. The math still works. You just have to know which math.

For the deeper affordability breakdown, read my full analysis of whether housing actually becomes affordable in 2026.

3. Mortgage Rate Whiplash: 5.99% to 6.61% in Five Weeks

This is the part of the story that should have been on every news channel in America and barely made the local segment. March 2026 delivered one of the sharpest short-term rate moves since the post-pandemic shock of 2022.

The timeline:

- Feb 27: 30-year fixed average at 5.99%. Three-year low.

- Feb 28: Strikes on Iran. Oil starts climbing.

- Mar 6: Freddie Mac average around 6.04%. Markets pricing in inflation risk.

- Mar 13: Rates climb to 6.22%. Applications start dropping.

- Mar 20: Redfin daily average hits 6.53% — six-month high.

- Mar 26: Fortune tracks conventional at 6.40%, VA at 6.06%, FHA at 6.15%.

- Mar 30–31: Bankrate’s benchmark 30-year fixed sitting at 6.61%.

- Apr 7: Ceasefire announced. 10-year yield begins easing. Mortgage rates start to follow.

The math on a real loan: on a $400,000 mortgage, the difference between 5.99% and 6.61% is roughly $160 more per month, and around $57,000 in additional interest over 30 years. That is a real, tangible, “I can feel it in my checking account” number.

But here is the Insider take, and this is the part you won’t get from a headline: even at 6.61%, rates are still lower than they were for most of 2023 and 2024, when buyers were routinely closing deals at 7% and above. The buyers who closed in 2023 are the buyers who already have equity right now. The buyers who waited are still waiting and with no equity.

The other thing to understand is the spread. According to Axios’s March 25 analysis, both the 10-year Treasury yield and the spread between that yield and mortgage rates rose in March. That’s a double hit. But here’s the upside: spreads historically compress when conditions stabilize. If peace can be established, you’ll get rate relief from two directions at once, falling Treasury yields and tightening spreads. That’s the scenario that pulls a sub-6% rate back into reach by late spring.

The smart play in this rate environment is not waiting. It is stacking tools. Builder rate buydowns. Seller-paid temporary buydowns (2-1 or 3-2-1 structures). Down payment assistance programs. Stack two or three of these on the right property and your net effective rate lands in the 5% range TODAY. No waiting on the Fed. No trying to time the markey. I lay this out in detail in my new construction guide for South DFW under $350,000.

4. National Inventory: 29 Straight Months of Growth and What It Means Locally

The slow grind of inventory recovery is one of the only consistent stories in housing right now. March extended the streak.

Zillow’s March 2026 Market Report shows 1.23 million homes for sale nationally, up 4.2% year-over-year and 9.5% from February. Realtor.com’s March data puts active listings at 964,477, up 8.1% year-over-year, the 29th consecutive month of annual inventory growth.

But, and this is critical, even with 29 straight months of expansion, national inventory is still 13.8% below the 2017–2019 baseline. The structural housing shortage in the U.S. remains over 4 million homes, according to Churchill Mortgage’s March update. That deficit is not closing this year and probably not next year either.

Regional inventory growth is uneven. The Midwest is up 13.6%, the West 10.6%, the Northeast 7.9%, and the South 5.8%. Texas is doing the heavy lifting in the South: the Texas Real Estate Research Center reported statewide active listings at 131,420 in January 2026, up 11.2% year-over-year, with 2026 expected to set new highs.

And here’s the part that surprises most agents I talk to: pending listings are up. Zillow reported 281,546 newly pending listings in March, the second-highest figure since August 2022, up 4.6% year-over-year and 29.8% month-over-month. That’s the strongest March for pending listings since 2021.

Read that signal carefully. Buyers are not hibernating. They are being more selective and more price-sensitive. The deals are happening. They are just happening to the buyers who showed up prepared and to the sellers who priced their homes correctly.

5. Home Prices in March: Why “National Headlines” Are Lying to You About DFW

If you’ve been reading national real estate coverage you’ve seen contradictory headlines all month. Some say prices are still rising. Others say they’re falling. Both are technically true and both are useless if you’re making a decision.

The most recent NAR data (February 2026) shows the national median existing-home price at $398,000, up 0.3% year-over-year. That’s the 32nd consecutive month of annual price gains. Zillow’s Home Value Index shows national values up about 0.8% year-over-year in March, slightly faster than February. Meanwhile Realtor.com shows the median list price down 1.2% year-over-year, the 23rd straight week of flat or negative list price growth, with price per square foot down 2.2%.

Both can be true at the same time because list prices and sale prices are not the same thing. Sellers are softening their asks faster than the actual closed-sale data is moving. That gap can’t last forever. One side is going to give.

In Texas, the Texas Real Estate Research Center projects a statewide median around $334,000 for 2026. Austin and San Antonio are softening more. Houston and DFW are more stable.

The DFW picture, broken down:

- DFW metro: median sale price around $399,000, down just 0.2% year-over-year is essentially flat, per Homes.com’s DFW report.

- Fort Worth / Tarrant County: $335,000 median, +3.6% year-over-year. The most resilient submarket in the metro.

- Dallas (city): average value $305,523, down 3.8% year-over-year, per Zillow’s Dallas page.

- Frisco: $645,000 median, modestly up year-over-year.

- McKinney: $440,000 median, +4.6% year-over-year – the best appreciation story in Collin County right now.

- DFW condos and townhomes: down roughly 19.8% year-over-year, reflecting brutal affordability pressure on attached product.

UTA economist Dr. Sriram Villupuram told UTA’s news office that DFW is transitioning from a frenzied seller’s market to a more balanced, but slower, environment, with flat-to-slightly-negative pricing through mid-2026.

For Ellis County and the southern corridor where I live and work every day:

- Waxahachie median is sitting in the high $300s to mid $400s. Stable.

- Midlothian is being held up by strong new-construction demand and elite school ratings.

- Red Oak has a structural floor under it from the Google and Compass Datacenters investments, that’s not a temporary tailwind, that’s a 10-year story.

The seller data point that matters most: over 8,000 DFW listings cut their asking price in March, and a local study showed 78% of buyers are now closing below ask. If you’re priced like it’s 2021, your house is going to sit. If you’re priced for the actual market, you’re going to sell.

6. Days on Market: The Single Most Honest Metric in This Market

Days on market doesn’t lie. Sellers can wish. Agents can spin. DOM tells you what’s actually happening.

FRED’s DFW series puts the DFW median at 48 days for March 2026. Fort Worth single-family is around 51 days. Dallas around 53. In practice, plenty of DFW homes are sitting 60 to 89 days before going under contract. That is a whole different ball game from the 10-to-14-day frenzy of 2021.

Statewide, the Texas Real Estate Research Center reports 104 days for unsold inventory, up from 97 in 2025 and 93 in 2024.

For sellers: the first two weeks on market are everything. Overprice in week one and you’re playing catch-up for the next ninety days. Photos matter. Staging matters. Foundation, roof, and HVAC matter more than they have at any time in the last 5 years because buyers have time to inspect, and they’re using it.

For buyers: you have negotiating room you haven’t had since 2019. A 60+ DOM listing usually has a motivated seller behind it. Foundation inspections, repair credits, rate buydowns paid by the seller, all of it is back on the table. But don’t get cute with well-priced sub-$350K homes in desirable areas. Those still move in two weeks. The leverage is in the middle and upper tiers, not the entry-level steal.

You can track real-time DOM by city using my Live DFW Market Updates hub.

7. North Texas County by County: The Real Map

DFW contains over 200 zip codes and dozens of distinct submarkets. Anyone telling you “the DFW market is doing X” without breaking it down is selling you a headline.

Tarrant County (Fort Worth, Mansfield, Arlington)

The most resilient submarket in the metro. $335,000 median, +3.6% year-over-year, around 3.5 months of inventory, sale-to-list ratio near 96%. Fort Worth’s diversified employment base and the fact that it never absorbed the same new-construction tsunami that Collin County is paying off right now. Arlington is a high-demand central corridor. Mansfield keeps pulling families for its schools. Grand Prairie is the move-up play for buyers priced out further north.

Collin County (Frisco, McKinney, Prosper, Allen)

The most pronounced cooling in the metro. Frisco absorbed massive new-construction waves from 2021 to 2024 with median prices around $645,000, DOM around 32 days. Prosper’s median sits near $895,000, supported by ~$198K median household income, but it’s the most rate-sensitive zip code in North Texas at the luxury end. McKinney, sitting at $440,000 with 4.6% year-over-year appreciation, is the best relative value in the county.

Denton County (Denton, Lewisville, Flower Mound, Carrollton)

Inventory climbing, DOM rising, sales slowing in pockets. The “Westoplex”, west of Fort Worth, is pulling demand toward more affordable corridors and applying pressure here.

Dallas County (Dallas, DeSoto, Cedar Hill, Duncanville, Lancaster)

The are is highly segmented. The city of Dallas itself saw sharp drops in new listings and sales in early 2026. Cedar Hill is the outdoor-access value play near Joe Pool Lake. DeSoto is a value corridor with strong schools. The City of Dallas’s First-Time Homebuyer Purchase Assistance Program offers up to $60,000 in deferred assistance, which is one of the most generous local programs in the entire state.

Ellis County (Waxahachie, Midlothian, Red Oak, Ennis, Ovilla, Glenn Heights)

The single most compelling value story in the entire metro. Waxahachie is sitting in the high $300s to mid $400s, getting steady demand from buyers priced out of the northern suburbs. Midlothian has 15+ active new-construction communities and is the hottest builder corridor south of I-20. Red Oak is leveraged directly by the Google and Compass Datacenters’ multi-billion-dollar buildout. Ennis gives you some of the lowest entry prices in DFW-adjacent Texas along the I-45 corridor.

For the broader strategic picture, read The Insider’s Complete 2026 Housing Market Forecast for North Texas.

8. New Construction in DFW: The Builder Incentive Window Is Wide Open

Pay attention to this section. This is where the math works right now.

New home sales nationally fell 17.6% in February. Builders responded the only way they can: aggressive incentives. Here is what’s actually on the table in DFW today:

1. Mortgage rate buydowns. Temporary structures (2-1 and 3-2-1) and permanent buydowns funded by the builder’s preferred lender. A 2-1 buydown on a 6.5% note gives you 4.5% in year one and 5.5% in year two. That is a real number giving measurable short-term payment relief.

2. Closing cost credits. $10,000 to $30,000 in flex cash toward lender fees, title, and prepaids is now standard. On some quick-move-in spec inventory, builders are stacking credits up to $50,000 combined.

3. Design center allowances. Credits for upgrades that hold long-term resale value like flooring, countertops, fixtures and even structural upgrades like extra bedrooms.

4. Lot premium discounts. Especially on quick-move-in homes and end-of-phase inventory that builders desperately need off the books.

The catch you have to know about: the preferred-lender requirement. Builder incentives are almost always tied to using the builder’s lender. That lender is sometimes great and sometimes not. Always compare the builder’s lender against an independent lender. A slightly lower rate plus lower fees from an independent can be worth more over the life of the loan than the headline incentive. This is exactly the kind of analysis I do with my buyers and it’s why I always tell my clients to talk to all three of my preferred lender partners side by side: Denise Donoghue at The Mortgage Nerd, Andrew Bryan at Miramar Mortgage, and Ethan Hester at Midtex Mortgage. Three quotes side by side really helps put the builder’s incentives into perspective.

For specific deals, see The 5 New Construction Gold Mines Under $350K That DFW Agents Don’t Want You to Find. For policy backdrop, read 40+ New Texas Laws Attracting Thousands of New Residents.

9. First-Time Buyers in 2026: You Are Not Locked Out – You Are Being Underserved

The story that first-time buyers can’t afford to buy in 2026 is wrong. It is being told by people who haven’t bothered to look at the data.

First-time buyers accounted for 34% of existing-home sales in February 2026, the highest share since last spring. The NAR Housing Affordability Index hit 117.6 in February, the highest level since March 2022 and the eighth straight month of improvement. Wages are outpacing home-price growth by nearly four percentage points.

Here is the actual program stack available to a first-time buyer in Texas right now:

- TSAHC Home Sweet Texas: 3% to 5% of the loan amount as a grant. Never repaid.

- TSAHC Homes for Texas Heroes: same structure, for teachers, first responders, veterans, healthcare workers.

- TDHCA My First Texas Home: up to 5% assistance as a 0% second lien, repaid only at sale or refinance.

- Local city programs: Fort Worth, Dallas, Irving, and Frisco all have programs ranging from $25,000 to $60,000 in assistance.

- Texas $140,000 Homestead Exemption: shields the first $140,000 of primary residence value from school district taxes. Lower monthly payment. Better qualification.

On the financing side, you’ve got conventional 3% down (HomeReady, Home Possible, Conventional 97), FHA at 3.5%, VA at 0% down, and USDA in eligible rural pockets of Ellis and surrounding counties.

The 20%-down myth is dead. Most successful first-time buyers I work with close with 3% to 5% down plus assistance. That’s the modern playbook.

For the full breakdown, read Will Housing Actually Become Affordable in 2026?.

Relocating? Start at Relocating to North Texas and International Relocation.

Married? Read New Property Tax Exemptions for Married Homeowners in Texas.

10. Sellers: The 2021 Playbook Is Dead. Here Is the 2026 One

If you’re a North Texas homeowner thinking about listing this spring, the window is open. But the rules have changed and the agents who haven’t updated their playbook are about to leave money on the table for their sellers.

Price accuracy is non-negotiable. With metro DOM at 48+ days, overpricing means extended time on market and lower eventual net proceeds. Every week you sit, you lose leverage.

Concessions are expected, not optional. Seller-paid closing costs, rate buydowns, and repair credits are running 2% to 3% of contract price and are the new normal. Budget for them up front. Don’t get blindsided in negotiations.

The best weeks to list nationally are mid-April through May, per Realtor.com seasonality data but, that window is closing fast.

Condition is a profit lever. In an inspection-heavy market, the foundation, roof, and HVAC questions are the deal-killers. Get ahead of them.

If you’re in Waxahachie, Midlothian, Mansfield, or Fort Worth, correctly priced homes are still moving and still hitting strong numbers. If you’re in outer Collin County, expect heavy competition from both resale inventory and aggressive builders. Strategy there matters more than ever.

Fort Worth urban core owner? See: Will Fort Worth’s New Panther Island Riverwalk Really Rival San Antonio?.

Short-term rental owner? Don’t sleep on The World Cup: Your DFW AirBnB Could Make $4,400+ This Summer.

11. The Road Ahead: Three Scenarios, One Strategy

March ended with more uncertainty than it began with. Here are the three real scenarios and what each one means for your move.

Scenario A: Ceasefire holds (most favorable). Oil stabilizes or drops. Inflation expectations ease. The 10-year drifts lower. Mortgage rates work back toward 6.0% to 6.2% by May. ManageCasa’s modeling has existing-home sales rising 3.48% year-over-year in 2026 if the conflict ends early.

Scenario B: Ceasefire collapses (most challenging). Oil re-spikes. Inflation fears reignite. The Fed leans hawkish. Talk of hikes intensifies. Mortgage rates push toward or above 7%. Buyer demand cools further.

Scenario C: Prolonged conflict, partial resolution (most likely). Tension persists through summer. Oil stays elevated but stable. Mortgage rates hover in the 6.3% to 6.6% range. Housing “muddles through” with flat prices and lower-than-expected transaction volume.

Here is the Insider truth that cuts through all three: North Texas has a structural demand advantage that doesn’t depend on which scenario plays out. DFW tops national rankings as the best place to buy, build, and finance real estate in 2026. Over 120 corporate relocations in the last five years. 40,000 to 50,000 new jobs created last year alone. Texas isn’t waiting on the Fed. Texas isn’t waiting on Iran. Texas is building, hiring, and absorbing population every single week in spite of those things.

The strategy in all three scenarios is the same: don’t time the market. Time the deal. Find the right property, structure it with the right tools, work with someone who actually understands the local sub-submarket, and execute. The clients I’m working with right now are getting better deals than the clients who waited through 2024.

Watch NAR’s existing-home sales release for the first full read of war-impacted closings.

The Insider FAQ: 10 Questions Buyers and Sellers Are Actually Asking

1. Is now a good time to buy a house in North Texas in 2026? For most qualified buyers, yes, with some nuance. Inventory is higher, DOM is longer, sellers are offering concessions, and assistance programs are stacked. This is the most buyer-favorable environment since 2019 in many DFW submarkets. Fort Worth and Ellis County are the top value plays. If you’re waiting for sub-5% rates, you’re going to be waiting beyond 2026.

2. Will home prices drop in North Texas in 2026? The data supports normalization, not a crash. Texas Real Estate Research Center projects 1% to 2% statewide growth, with DFW flat to slightly negative through mid-year and stabilizing after. Outer Collin County faces the most pressure. Ellis County and Fort Worth are stable.

3. What are mortgage rates right now and will they go down in 2026? As of March 31, the 30-year fixed is in the 6.5% to 6.6% range. Markets expect one quarter-point Fed cut by year-end. If the ceasefire holds and inflation eases, modest downward drift is likely. A return to the 5s is possible but not guaranteed.

4. Is North Texas a buyer’s or seller’s market right now? Mixed. Fort Worth and Ellis County lean slightly seller-friendly. Metro-wide is near balanced with concessions common. Outer Collin County tilts toward buyers. Buyers have more leverage than at any time since 2019, but this isn’t a deep-discount environment.

5. How is the Iran war affecting the housing market? Two channels: higher oil pushes inflation expectations, which pushes Treasury yields, which pushes mortgage rates. And higher materials costs make new construction more expensive and slower. Rates rose from 5.99% to 6.61% in five weeks. Applications fell 10%+. The April ceasefire started reversing some of it. but only temprorarily.

6. Should I sell now or wait for rates to come down? Waiting assumes rates fall meaningfully and that may not happen this year. Meanwhile inventory keeps building, especially from builders. If you’re in Fort Worth, Waxahachie, or Midlothian, listing this spring with accurate pricing and a concession budget is a strong move.

7. How much is DFW inventory up in 2026? DFW active listings are up roughly 20% to 22% year-over-year, with around 30,000 active listings at any time. Statewide is up 11.2%. Texas Real Estate Research Center expects 2026 to set new highs.

8. What are the best cities to buy in North Texas in 2026? Waxahachie, Midlothian, Red Oak, Ennis, Fort Worth, Mansfield, and McKinney. The combination of price, job access, and appreciation potential is best in those seven cities.

9. Do I need 20% down to buy a house in Texas? No. You can purchase with FHA at 3.5%, conventional at 3% down, VA at 0% down and USDA at 0% down in eligible areas, not including local and state assistance programs. Most successful first-time buyers close with 3% to 5% down plus assistance.

10. How long does it take to sell a house in North Texas right now? Median DFW DOM is around 48 days. Fort Worth around 51. Statewide unsold inventory near 104. Properly priced homes in strong submarkets still sell in two to four weeks. Overpriced or condition-challenged listings are sitting between 90 to 120+ days.

Work With Someone Who Actually Reads the Data

Whether you’re buying your first home in Waxahachie, relocating from California to DFW, selling a property in Fort Worth, or looking at investment plays in Ellis County, the decisions you’re making this spring are too consequential to base on national headlines.

As a REALTOR® with Legacy Realty Group under Broker/Owner Leslie Majors (consistently ranked in the top 1% of Ellis County agents) I work every transaction with the same data-driven intelligence applied to your unique situation.

Ready to make a move? Schedule a Consultation

Bobby Franklin, REALTOR®

Legacy Realty Group – Leslie Majors Team

📲 214-228-0003 | northtexasmarketinsider.com

Bobby Franklin is a licensed Texas REALTOR® (License #0805459) with Legacy Realty Group – Leslie Majors Team, serving buyers and sellers across Ellis County, DFW, and greater North Texas. All content represents the author’s market analysis and professional opinion based on publicly available data. Nothing in this article constitutes legal, financial, or tax advice. Real estate services are provided without regard to race, color, national origin, religion, sex, familial status, disability, or any other characteristic protected under the Fair Housing Act or applicable Texas law.

Mortgage referrals are provided from multiple lenders: Denise Donoghue at The Mortgage Nerd, Andrew Bryan at Miramar Mortgage, and Ethan Hester at Midtex Mortgage in compliance with the Real Estate Settlement Procedures Act (RESPA). Commission amounts are not fixed or recommended by any real estate organization and are fully negotiable. NAR Code of Ethics compliance is maintained at all times. This content is 100% original, created exclusively for North Texas Market Insider, and is not reproduced from any other source.