By Bobby Franklin, REALTOR® | North Texas Market Insider™ | Legacy Realty Group – Leslie Majors Team | Serving Ellis County, DFW & Greater North Texas

The Headline That Should Have Stopped You Cold

I want you to sit with this for a second.

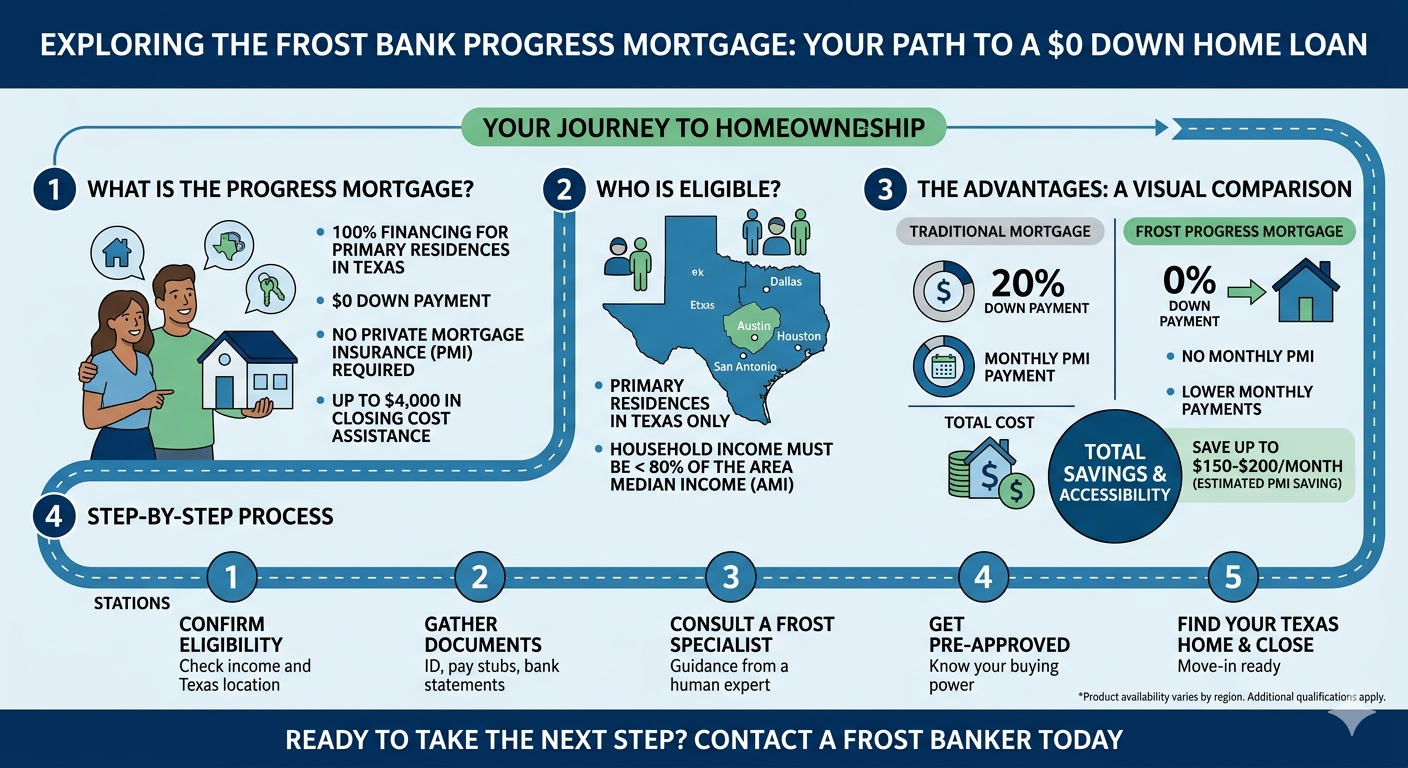

One of the most respected, financially stable banks in the state of Texas just re-entered the mortgage business after a 20-year absence and their opening move is a 100% financing product with no down payment, no PMI, and up to $4,000 toward your closing costs.

That’s not a teaser rate. That’s not a bait-and-switch. That is Frost Bank’s Progress Mortgage, and it is real, it is live, and it is available right now to qualifying buyers across the state of Texas, including every community I serve from South DFW down through Ellis County and beyond.

If you’ve been sitting on the sidelines of homeownership because you couldn’t accumulate a down payment fast enough or because rent kept going up faster than your savings account could grow, this is the article that was written specifically for you.

I’m going to break down exactly how this product works, who qualifies, what it costs you in real dollars, how it compares to every other zero-down option available in Texas, and why the convergence of this product with current North Texas market conditions is creating one of the most significant buyer opportunities I’ve seen in over a decade.

No hype. No fluff. Just intelligence you can actually act on.

Let’s go.

Who Is Frost Bank, and Why Should You Take This Seriously?

Because I know what you’re thinking. Zero down, no PMI, it sounds like the kind of product that disappeared in 2008 for good reason. So let me establish why this is categorically different.

Frost Bank is not a startup. It is not a fringe online lender chasing market share with reckless underwriting. Frost Bank is the largest bank headquartered in San Antonio, Texas, with approximately $53 billion in total assets and more than 206 financial centers spread across the state, up from 131 locations when its branch expansion began in 2018. That’s a 57% increase in physical footprint. Its parent company, Cullen/Frost Bankers, Inc. (NYSE: CFR), is publicly traded with full regulatory oversight and a transparent earnings history. American Banker named Frost a Top Performing Bank (over $50 billion in assets) for 17 consecutive years.

Frost exited the mortgage business around the year 2000. Ironically, right before one of the largest real estate run-ups in American history. Now they’re back, and they didn’t ease back in quietly. According to National Mortgage Professional, Frost hired 80 dedicated loan officers, built a digital lending platform in partnership with Infosys, and rolled out mortgage operations across Texas in phases. By the end of 2025, Frost’s mortgage division had surpassed its own internal target of $500 million in outstanding loans, reaching $595 million, with its best single quarter on record coming in Q4 2025.

This is a disciplined, capitalized, Texas-rooted institution making a serious long-term commitment to the home lending market. When Frost designs a mortgage product, they build it to perform, not to blow up on the books in three years.

The Progress Mortgage is their flagship community lending product, and understanding it is the first step toward using it.

What the Frost Bank Progress Mortgage Actually Is

Here are the core features, drawn directly from Frost Bank’s official mortgage page:

$0 Down Payment. Full stop. 100% financing. You do not bring a down payment to the closing table.

No Private Mortgage Insurance (PMI). This is the feature that separates the Progress Mortgage from almost every other zero-down or low-down product on the market. PMI typically adds $100 to $300 per month to your housing payment when your loan-to-value ratio exceeds 80%. Frost waives it entirely. That’s real money, anywhere from $1,200 to $3,600 per year back in your pocket.

Up to $4,000 in Lender Credits Toward Closing Costs. If your income is at or below 80% of the Area Median Income (AMI) for your county, Frost will credit up to $4,000 toward your total closing costs. Combined with the zero down payment, qualifying buyers can potentially reach the closing table with little to nothing out of pocket.

Administrative Fee Waiver for LMI Census Tract Borrowers. If your subject property is located in a low-to-moderate income census tract and your income falls between 80% and 110% of AMI, Frost waives its administrative fee even if you don’t qualify for the $4,000 credit.

30-Year Fixed Rate. This is a stable, predictable loan product. Not an adjustable rate. Not an interest-only structure. A traditional 30-year amortizing mortgage with a fixed payment from day one.

No Minimum Loan Amount. Useful for buyers targeting more modestly priced homes in Ennis, Ferris, or Palmer where entry-level inventory can be found well below the metro average.

Available Exclusively in Texas.

The primary qualifying threshold is income. To access the full benefit package, including the $4,000 closing cost credit, your household income must fall at or below 80% of the Area Median Income (AMI) as defined by the Federal Financial Institutions Examination Council. AMI figures are updated annually and vary by county and household size. Use the FFIEC Census Data tool to look up the exact figure for your area before assuming eligibility.

Why Is Frost Doing This Right Now? The Strategic Play Behind the Product

This is where I want to give you more than the press release version. Frost Bank is not launching the Progress Mortgage out of pure altruism. This is also smart, calculated market positioning and understanding the strategy tells you something important about the market conditions we’re operating in right now.

The North Texas housing market has shifted materially over the past 18 months. After years of explosive appreciation and a seller’s market that left buyers outgunned and exhausted, the DFW market is entering what researchers at the University of Texas at Arlington have called a “turning point.” Active listings across DFW are up more than 22% year-over-year. Days on market have extended to 60 to 89 days across many submarkets, compared to 10 to 14 days during the pandemic frenzy. Home values in markets like Waxahachie have seen year-over-year softening. The bidding war era is over. Sellers are negotiating again.

At the same time, mortgage rates are stabilizing. The 2026 Texas mortgage rate forecast from Fannie Mae, NAR, the Mortgage Bankers Association, and Wells Fargo all project rates holding near 6.0% to 6.4% for most of the year. That range is historically normal. The 30-year average from 1990 through 2020 was approximately 6.3%. And in a stable rate environment, a deposit-taking bank can confidently build a long-term mortgage book.

Frost sees exactly what I’ve been telling my clients: there is a massive, underserved population of working Texans who have solid employment, stable income, and the discipline to be responsible homeowners, but who simply haven’t been able to outrun rising rents long enough to stack a meaningful down payment. The Progress Mortgage is designed for that buyer. And in 2026, that buyer exists in enormous numbers across Ellis County and the broader South DFW corridor.

This isn’t charity. It’s a business decision that happens to create a generational wealth-building opportunity for the right buyers at exactly the right moment.

Who Qualifies — The Honest, Detailed Breakdown

The Income Threshold: 80% AMI

The primary qualification gate is income. Your household gross income must fall at or below 80% of the Area Median Income for your specific county, as determined annually by the FFIEC. This is a standard benchmark used across community lending programs nationwide, the same standard used by Frost’s companion product, the Frost Progress Home Equity Loan.

What does 80% AMI actually look like in North Texas? In general terms, for a family of four in the Dallas-Fort Worth metro, 80% AMI typically falls somewhere in the range of $70,000 to $90,000 annually, though these figures shift annually and vary by county. Single-person households and smaller families will have correspondingly lower thresholds. The only way to know your exact number is to look it up directly at the FFIEC Census App and then verify it with Frost.

Credit Score

Frost has not published a minimum credit score on their public website. As with most community lending products, standard underwriting criteria apply. As a general reference point, most programs of this type look for scores of 620 or above, but your specific situation may vary so it’s always worth asking. If you have credit concerns, start with a free credit review at AnnualCreditReport.com and consider working with a HUD-approved housing counselor before you apply anywhere.

Property Type and Location

The Progress Mortgage is available throughout Texas. Standard single-family homes are the primary target. If you’re asking about condos, townhomes, or new construction, get that answer directly from Frost before you get too far into the process. Call them at (877) 521-4011, Monday through Friday, 8am to 5pm CT, or start an application at frostbank.com/mortgage.

Owner-Occupied Primary Residence

This loan program is offered only for the home you live in. Investment properties and vacation homes are not eligible.

The Honest Comparison: Frost vs. Every Other $0 Down Option in Texas

I believe in giving you the full picture. The Frost Progress Mortgage is powerful, but it’s not the only path to zero-down homeownership in Texas. According to Dwellverse’s 2026 Texas zero-down guide, there are at least six distinct programs that can get a qualifying buyer to the closing table without a traditional down payment. Here’s how the major options stack up:

| Program | Down Payment | PMI / Fees | Income Limit | Who Qualifies | Closing Cost Help |

|---|---|---|---|---|---|

| Frost Progress Mortgage | $0 (100%) | No PMI | ≤80% AMI (or 80–110% in LMI tract) | Texas residents | Up to $4,000 lender credit |

| VA Loan | $0 | No PMI; funding fee applies | None | Veterans, active military, surviving spouses | Seller concessions allowed |

| USDA Loan | $0 | 1% upfront + 0.35%/yr | 115% AMI | Rural/suburban eligible areas | Seller concessions allowed |

| TDHCA My First Texas Home | Up to 5% DPA | Depends on loan type | Varies by county | First-time buyers & Texas veterans | DPA covers down payment + closing costs |

| TSAHC Home Sweet Texas | Up to 5% grant (non-repayable) | Depends on loan type | ≤80% AMI | All Texas buyers | Grant covers down payment + closing costs |

| SETH 5 Star Program | Up to 5% DPA (forgiven after 3 yrs) | Depends on loan type | 80% AMI | Southeast Texas eligible areas | DPA covers down payment + closing costs |

Sources: Texas State Affordable Housing Corporation (TSAHC), Southeast Texas Housing Finance Corporation (SETH), Texas Department of Housing and Community Affairs (TDHCA), reAlpha Zero-Down 2026 Guide

Here’s what the table doesn’t fully communicate: the Frost Progress Mortgage is unique in combining 100% financing, no PMI, and closing cost credits in a single product from a deposit-taking Texas bank. Most comparable programs either require PMI, attach a second lien, or carry higher ongoing guarantee fees. For buyers who qualify, the no-PMI structure alone can save more money over the first five years of the loan than the down payment assistance itself would be worth.

If you’re a veteran or active military, your first call is still a VA loan specialist, the VA benefit is unmatched. If you’re in an eligible rural or suburban area, USDA has its own advantages. But if you’re a working-income Texas buyer looking at the suburban DFW and Ellis County markets, the Frost Progress Mortgage deserves serious consideration as your primary option.

Real Numbers: What Does $0 Down Actually Look Like in North Texas?

Let me run a realistic scenario so you can see what this looks like on paper, not in theory.

Assume you’re purchasing a home in Waxahachie at $340,000, a realistic price point in southern Ellis County right now. Here’s what the numbers look like with the Frost Progress Mortgage:

- Down Payment: $0

- Loan Amount: $340,000

- PMI: $0 (waived by the program)

- Closing Cost Credit: Up to -$4,000 for qualifying borrowers

- Estimated Monthly Principal & Interest at 6.25%: approximately $2,093/month

- Texas Property Taxes (est. 2.2% annually): approximately $623/month

- Homeowners Insurance (est.): approximately $150/month

- Estimated Total Monthly PITI: approximately $2,866/month

Now compare that to what you’re paying in rent. Single-family rental homes in Ellis County are commanding $1,800 to $2,400 per month in 2026. At the high end of that range, you’re paying $2,400 per month to build exactly zero equity, for someone else.

With the Progress Mortgage at $2,866 per month, you’re paying roughly $466 more monthly. But you are building equity from day one in a market where Waxahachie has posted 124.48% appreciation over the past decade and an 8.42% average annual appreciation rate. The long-term wealth math is not close.

Important: The payment above is an illustrative estimate, not a commitment or guarantee. Frost Bank’s current posted rate for a 30-year fixed mortgage is 6.250% (APR 6.345%) as of publication. Actual rates, taxes, insurance, and fees will vary by borrower situation. Always work directly with a licensed mortgage professional for personalized figures.

The Real Talk: Honest Pros and Cons of a Zero-Down Mortgage

I’m not here to sell you a product. I’m here to give you the intelligence to make the right decision for your situation. So let’s be direct about both sides of this.

The Advantages

You can stop waiting and start owning. The traditional path to homeownership of save 3.5% to 5%, watch while watching rent outpace your savings, repeat — has kept millions of qualified buyers out of the market for years longer than necessary. The Progress Mortgage eliminates the down payment barrier entirely.

Your cash stays liquid. Your emergency fund, your reserves, your ability to handle a broken HVAC unit in the first year, all of it stays intact. You don’t drain your savings account at the closing table and then hold your breath hoping nothing breaks.

The no-PMI structure is genuinely rare. Every time you look at a conventional loan below 20% down, or an FHA loan, PMI is eating into your monthly budget. The Frost Progress Mortgage eliminates that line item. That matters every single month for the life of the loan, until your equity builds enough to remove it in other programs, which takes years.

And $4,000 toward closing costs for qualifying buyers means the total cash-to-close number can be remarkably small. Per Bankrate’s closing cost analysis, Texas closing costs typically run 2% to 5% of the loan amount. On a $340,000 loan, that’s $6,800 to $17,000 and with $4,000 off the top, it’s a meaningful reduction.

The Risks You Need to Understand

You start with zero equity. If the market declines in the first few years before you’ve built equity through monthly payments, you could find yourself temporarily underwater, owing more than the home is worth. This is a real risk in any market, but it’s particularly relevant in North Texas right now where some submarkets are still digesting post-pandemic price corrections.

You will pay more total interest over the life of the loan compared to putting money down. On a $340,000 loan versus a $323,000 loan (5% down), you’re financing $17,000 more and at 30 years, that adds up.

Texas property taxes are not optional and they are not small. At 2.0% to 2.5% annually, property taxes in North Texas communities typically add $400 to $700 per month to your housing costs. Budget for this before you fall in love with a payment that doesn’t include it.

You still need reserves. Zero-down does not mean zero financial readiness. Responsible homeownership requires an emergency fund. Plan for 1% to 2% of the home’s value annually for maintenance and repairs. If you have literally nothing saved after this purchase, that’s a risk management problem, not just a homeownership strategy.

The Bottom Line on Risk

For buyers with stable, verifiable income, a plan to stay in the home for a minimum of five to seven years, and a modest reserve fund intact after closing, the Frost Progress Mortgage is a responsible and powerful tool. For buyers in unstable employment, planning to relocate in 18 months, or with no financial cushion at all, the lack of starting equity makes this riskier than it looks on paper. Know which situation you’re in.

Why 2026 Is One of the Best Buyer Markets North Texas Has Seen Since 2012

I’ve been tracking this market for years, and I’ll tell you exactly what the data says, not what feels good to say.

The numbers are objectively favorable for buyers right now.

Active listings across DFW are up more than 22% year-over-year. You have real options. You’re not walking into a 40-offer situation and waiving inspections to compete. Homes are averaging 60 to 89 days on market across DFW. Sellers have been waiting, and they know it. Prices have corrected meaningfully from their 2022 peaks across multiple submarkets. And mortgage rates, while not back to the 3% anomaly of 2020 and 2021, have stabilized in the historically normal 6.0% to 6.3% range, exactly where Fannie Mae, NAR, and the Mortgage Bankers Association all project them to hold through most of 2026.

As I covered in my 2026 North Texas Housing Market Forecast, the convergence of these conditions; rising inventory, extended days on market, price softening, and rate stability is precisely the environment in which prepared buyers build wealth while unprepared buyers keep waiting.

The Fed’s March 2026 rate pause isn’t a warning signal. It’s a green light for buyers who understand what rate stability actually means for purchasing power and planning. As I wrote in my breakdown of the mortgage rate lock-in era finally ending, more sellers who were frozen by their low-rate mortgages are finally listing, which is adding supply and negotiating opportunity into a market that desperately needed both.

PricewaterhouseCoopers and the Urban Land Institute ranked DFW the number one market in the nation for buying, building, and financing property in 2026. That’s not sentiment. That reflects job growth, relative affordability compared to coastal markets, and the infrastructure of a region that continues to attract people and capital at a pace that virtually no other metro in the country can match.

The buyers who move in 2026 will look back on this the same way 2012 buyers do now.

Where to Buy in North Texas: The Best Communities for Progress Mortgage Buyers

The Frost Progress Mortgage is built for buyers at or below 80% AMI. In the DFW context, that means buyers who are targeting the $250,000 to $400,000 price range. Which is exactly where the North Texas value corridor lives. Here’s where I’d be looking right now if I were in that buyer profile:

Waxahachie

This is my home market and I’ll stand behind it without hesitation. With a median sale price running approximately $327,000 to $371,000 (Redfin/Zillow, February 2026) and a price per square foot of around $152, that makes it among the lowest in the entire South DFW corridor. Waxahachie consistently delivers the best value proposition within reasonable commuting distance of Dallas. Housing costs here run approximately 14% below the national average. As I detailed in my breakdown of Waxahachie’s long-term appreciation story, the city has posted 124% appreciation over the past decade while the approved Minto Communities development of 13,270+ homes signals the city’s trajectory is far from finished. Get in before the market figures that out completely.

Ennis

South of Waxahachie along I-45, Ennis offers small-town character with even more accessible price points for first-time buyers targeting the lower end of the Progress Mortgage range. Check the current Ennis market data page on this site for real-time stats.

DeSoto

Positioned at the intersection of I-35E, I-20, and US-67, DeSoto puts you within 15 minutes of downtown Dallas at price points that remain meaningfully below inner-ring suburbs. See the DeSoto market page for current numbers.

Red Oak, Midlothian, and Ferris

These southern Ellis County communities feature newer inventory, strong school districts, and price points well within Progress Mortgage qualifying territory. Red Oak in particular, sitting on the I-35E corridor, offers excellent access to Cedar Hill, Duncanville, and the southern Dallas employment base.

Relocating to North Texas From Out of State?

If you’re coming from California, Colorado, Arizona, or the Northeast, the math gets even more compelling. Texas has no state income tax. Combined with the Progress Mortgage’s zero-down structure, buyers relocating from high-cost states often experience a dramatic improvement in both monthly cash flow and long-term financial position on day one. I cover this in depth in my Relocating from California to Texas intelligence briefing.

How to Apply for the Frost Progress Mortgage: Step by Step

Step 1 — Verify Your AMI Eligibility First

Use the FFIEC Census Data tool to look up the 80% AMI figure for your specific county. Compare it to your household’s gross annual income before you do anything else. This step takes five minutes and tells you immediately whether the full benefit package applies to your situation.

Step 2 — Get Your Documents Together

You’ll need: two months of recent pay stubs, two years of W-2s, two years of tax returns, two to three months of bank statements, a government-issued ID, and your Social Security number. According to the DFW First-Time Homebuyer Guide, most lenders can issue a pre-approval within 24 to 48 hours once you submit a complete package. Get organized before you call.

Step 3 — Contact a Frost Mortgage Loan Advisor

Call (877) 521-4011, Monday through Friday, 8am to 5pm CT, or start online at frostbank.com/mortgage. Ask specifically about the Progress Mortgage and confirm current income limits, credit requirements, and eligible property types for your target area.

Step 4 — Understand Your Full Housing Budget

Your mortgage principal and interest is one number. In Texas, your full housing cost includes property taxes (2.0% to 2.5% annually), homeowners insurance, and any HOA fees. A responsible rule of thumb is to keep total housing costs, taxes and insurance included, under 28% to 30% of gross monthly income. Use the CFPB’s “Owning a Home” tool to stress-test your budget before you fall in love with a specific price point.

Step 5 — Consider Homebuyer Education

A HUD-approved homebuyer education course is required for many assistance programs and recommended for all first-time buyers regardless. It takes a few hours and gives you a framework for understanding the full cost of homeownership, not just the mortgage payment.

Step 6 — Work With a Local REALTOR® Who Knows the Market

Your lender handles the financing. Your REALTOR® handles everything else; pricing strategy, negotiation, inspection coordination, title issues, and closing logistics. Under the 2024 NAR Settlement, buyers are now required to sign a written buyer representation agreement before touring homes, with transparent disclosure of agent services and compensation. All commissions are fully negotiable. You deserve a REALTOR® who tells you the truth about a property, not just the version that moves the transaction forward. That’s the only kind of representation I provide.

Step 7 — Never Skip the Inspection

Even with $0 down. Especially with $0 down. In Texas, foundation condition, HVAC age, roof state, and drainage are critical variables that affect both your long-term cost of ownership and your insurance eligibility. Protect your investment from the beginning. And for why you should always include an elevation survey check out my article How Elevation Surveys Can Save You From A Bad Foundation

Can You Stack the Progress Mortgage With Other Assistance Programs?

This is one of the most common questions I’m already fielding, and I’m going to give you the straight answer: it depends on Frost’s specific underwriting guidelines and whether Frost is an approved lender for programs like TDHCA’s My First Texas Home or TSAHC’s Home Sweet Texas product.

Most Texas DPA programs are structured as second liens attached to first mortgages originated through participating lenders. Frost Bank must be on the approved lender list for a combination to work. As of publication, that confirmation is not publicly available. Contact both Frost and the relevant program administrator before you assume stacking is an option.

What is confirmed: if you don’t qualify for the Progress Mortgage’s income limits, or prefer a different structure, TSAHC’s Home Sweet Texas program provides up to 5% in non-repayable grant money for buyers at or below 80% AMI and is combinable with FHA, VA, USDA, or conventional loans through TSAHC-approved lenders. The TDHCA My First Texas Home program similarly provides up to 5% in deferred or forgivable down payment assistance statewide.

I broke down the broader Texas assistance landscape, including programs providing $15,000 to $50,000 or more in combined benefit for qualifying buyers, in my article Will Housing Actually Become Affordable in 2026?

The path to zero-out-of-pocket homeownership exists. It just requires knowing which door to walk through.

What This Means for the North Texas Market at Large

Beyond any individual buyer transaction, the re-entry of Frost Bank into the Texas mortgage market with a specifically designed community lending product, has meaningful implications for the housing ecosystem I track every day.

More first-time buyers will be able to enter the market. Buyers who were previously locked out by the down payment requirements can finally qualify. That expands the demand pool at entry-level price points across North Texas.

Sellers in the $250,000 to $400,000 range gain a new buyer audience. Homes that sat because buyers couldn’t assemble a down payment now have a qualified audience. For sellers in that price band, this is meaningful.

Lender competition benefits consumers. Frost’s aggressive market entry creates pressure on other Texas lenders to sharpen their community lending products. That competition ultimately produces better options for buyers across the board.

Long-term market stability improves. Programs that put income-verified, employment-stable buyers into homes, rather than speculative investors using creative financing, contribute to the kind of measured, sustainable market appreciation that compounds wealth for actual families over decades.

As I tracked in my analysis of mortgage rates dropping toward the 6% threshold, the convergence of moderating rates, rising inventory, and newly accessible lending products is creating a buyer environment we haven’t seen in this market since 2012. The Frost Progress Mortgage is one more piece of that convergence.

FAQs: The Most Common Questions About the Frost Progress Mortgage

Is the Frost Bank Progress Mortgage available everywhere in Texas?

Yes. The Frost Progress Mortgage is available statewide in Texas, exclusively. It is not offered in any other state. Frost operates over 206 financial centers across Texas with 80 dedicated mortgage loan officers deployed statewide.

What is the income limit to qualify?

You must earn no more than 80% of the Area Median Income (AMI) for your county, as defined by the FFIEC. Borrowers in low-to-moderate income census tracts earning between 80% and 110% of AMI are also eligible but receive a fee waiver rather than the $4,000 closing cost credit. AMI is updated annually so always verify your current number at the FFIEC Census App.

Do I really pay no PMI?

Correct. Unlike virtually every other low- or no-down-payment product on the market, the Frost Progress Mortgage does not require Private Mortgage Insurance. That saves you $100 to $300+ per month compared to comparable products that do carry PMI.

What credit score do I need?

Frost has not published a minimum publicly. Most community lending products in Texas look for scores at or above 620 as a general threshold. Contact Frost at (877) 521-4011 for the current underwriting criteria specific to your profile.

Can I use this for new construction?

Frost’s public materials don’t explicitly exclude new construction, but new construction purchases typically involve a different loan structure than existing home purchases. Confirm directly with a Frost Mortgage Loan Advisor before making any assumptions about new build eligibility. Often its better to use a new construction’s lender anyway, because of the incentives they offer.

What other zero-down options exist in Texas if I don’t qualify?

VA loans for veterans, USDA loans for eligible rural and suburban properties, TDHCA My First Texas Home, and TSAHC Home Sweet Texas all provide pathways to low- or no-out-of-pocket homeownership for qualifying Texas buyers. Each has distinct eligibility rules, geographic requirements, and fee structures. A qualified REALTOR® and a HUD-approved housing counselor can help you identify which program fits your situation.

Can I combine the Progress Mortgage with DPA programs?

The Progress Mortgage is already 100% financing so there’s no down payment to assist. The $4,000 in lender credits addresses closing costs. Whether you can layer additional Texas DPA programs on top depends on whether Frost is an approved lender for those programs and whether the combined structure satisfies all underwriting requirements. Confirm with both Frost and the relevant program administrator before you build your strategy around a combination.

What are Frost’s current mortgage rates?

As of publication(04/02/26), Frost’s standard 30-year fixed rate is 6.250% (APR 6.345%) and their 15-year fixed is 5.500% (APR 5.654%), per frostbank.com/mortgage. The Progress Mortgage rate is not listed separately on the public rate sheet. Contact Frost directly for a personalized rate quote. Keep in mind, rates adjust daily.

What do I generally need to qualify for a Texas home loan in 2026?

Credit score of 580 to 640+ (varies by program), documented stable employment and income, two months of pay stubs, two years of W-2s and tax returns, bank statements, government-issued ID, and Social Security number. Texas-specific planning should account for property taxes at 2.0% to 2.5% annually and the importance of foundation inspection given the state’s expansive clay soils. The CFPB’s homebuying preparation guide is a solid checklist resource.

Is right now actually a good time to buy in North Texas?

Based on current market data… yes, for buyers who are financially ready. Inventory is up 22%+ year-over-year. Days on market have extended significantly. Prices have softened in multiple submarkets. Mortgage rates are stable in the historically normal range. PricewaterhouseCoopers and the Urban Land Institute ranked DFW the number one market in the nation for buying, building, and financing in 2026. For the full data-backed analysis, read my 2026 North Texas Housing Market Forecast.

Ready to Make Your Move? Here’s Exactly What to Do Next

You’ve got the intelligence. Now comes the execution.

I’m Bobby Franklin, REALTOR® with the Leslie Majors Team at Legacy Realty Group. I cover the full corridor from South DFW through Ellis County and beyond, with a specific focus on buyer relocation, new construction strategy, first-time buyer navigation, and the kind of market data most agents aren’t pulling. If the Frost Progress Mortgage sounds like it might be your path to homeownership, here’s your next step:

Text or call me directly for a no-pressure strategy conversation. We’ll look at your income, your target price range, your timeline, and your specific situation. We’ll determine which program or combination of programs puts you in the best financial position. Sometimes that’s the Progress Mortgage. Sometimes it’s TSAHC. Sometimes it’s USDA. Sometimes it’s a combination we build together with one of my trusted lender partners:

- Denise Donoghue — The Mortgage Nerd | yourmortgagenerd.com

- Andrew Bryan — Miramar Mortgage | miramarmortgage.com

- Ethan Hester — Midtex Mortgage | mid-texmortgage.com

Explore my market intelligence — city-specific data pages, relocation guides, school district breakdowns, new construction buyer playbooks, and my weekly market analysis at NorthTexasMarketInsider.com.

Here’s what I want you to understand as we close this out.

Homeownership is the most powerful, most accessible wealth-building tool available to working families in America. It is not perfect. It carries risk. It requires discipline. But no other vehicle available to the average household; not a 401k, not a savings account, not any investment product a financial advisor will put in front of you can build generational wealth the way owning real estate in a growing market does over time.

Programs like the Frost Progress Mortgage exist because there is a gap between qualified buyers and accessible financing. Smart institutions with long term horizons are seeing an opportunity to close it responsibly. This is one of those rare moments when the policy environment, the market conditions, and the financing products are all pointing in the same direction for the buyers I work with every day.

The down payment is no longer the reason to wait.

Bobby Franklin, REALTOR® | Legacy Realty Group – Leslie Majors Team

📲 214-228-0003 | northtexasmarketinsider.com

Legal Disclosures: Bobby Franklin is a licensed Texas REALTOR® operating under Legacy Realty Group – Leslie Majors Team. All services are provided in compliance with the Texas Real Estate Commission (TREC), the NAR Code of Ethics, the Fair Housing Act, RESPA, and all applicable state and federal advertising regulations. Real estate commissions are fully negotiable; no rates are fixed or steered.

Buyer representation agreements are required prior to home tours in accordance with the August 2024 NAR Settlement. This blog post is original content created for informational purposes only and does not constitute legal, financial, or mortgage advice. Loan eligibility, rates, terms, and program availability are subject to change; always consult directly with a licensed lender for personalized guidance. All third-party programs described are subject to their own eligibility requirements and availability.