The Federal Reserve just held rates steady in March 2026. And I want to tell you something that most agents in this market are not going to say out loud:

This is the moment you’ve been waiting for and most sellers are going to miss it.

Not because the market is exploding. Not because rates dropped to 3%. Not because buyers are lining up around the block the way they were in 2021. The opportunity here is quieter than that, more strategic than that, and frankly more durable than anything we saw during the pandemic frenzy.

Here’s the Insider read: when the Fed holds rates steady after a period of volatility, something psychologically significant happens to the market. Buyers stop waiting for “the next shoe to drop.” Sellers stop holding their breath. And the people who understand what that psychological shift actually means, those who have been studying the data, watching the permit filings, tracking the demographic flows, those people position themselves before everyone else catches on.

That’s what this article is about. Not hope. Not hype. Intelligence.

If you own a home in North Texas, in Ellis County, in Waxahachie, Midlothian, Red Oak, Ennis, or anywhere along the south DFW corridor, I’m going to break down exactly what this Fed decision means for your equity, your timing, and your next move. Let’s go.

What the Fed Actually Did And Why It Matters More Than the Headlines Suggest

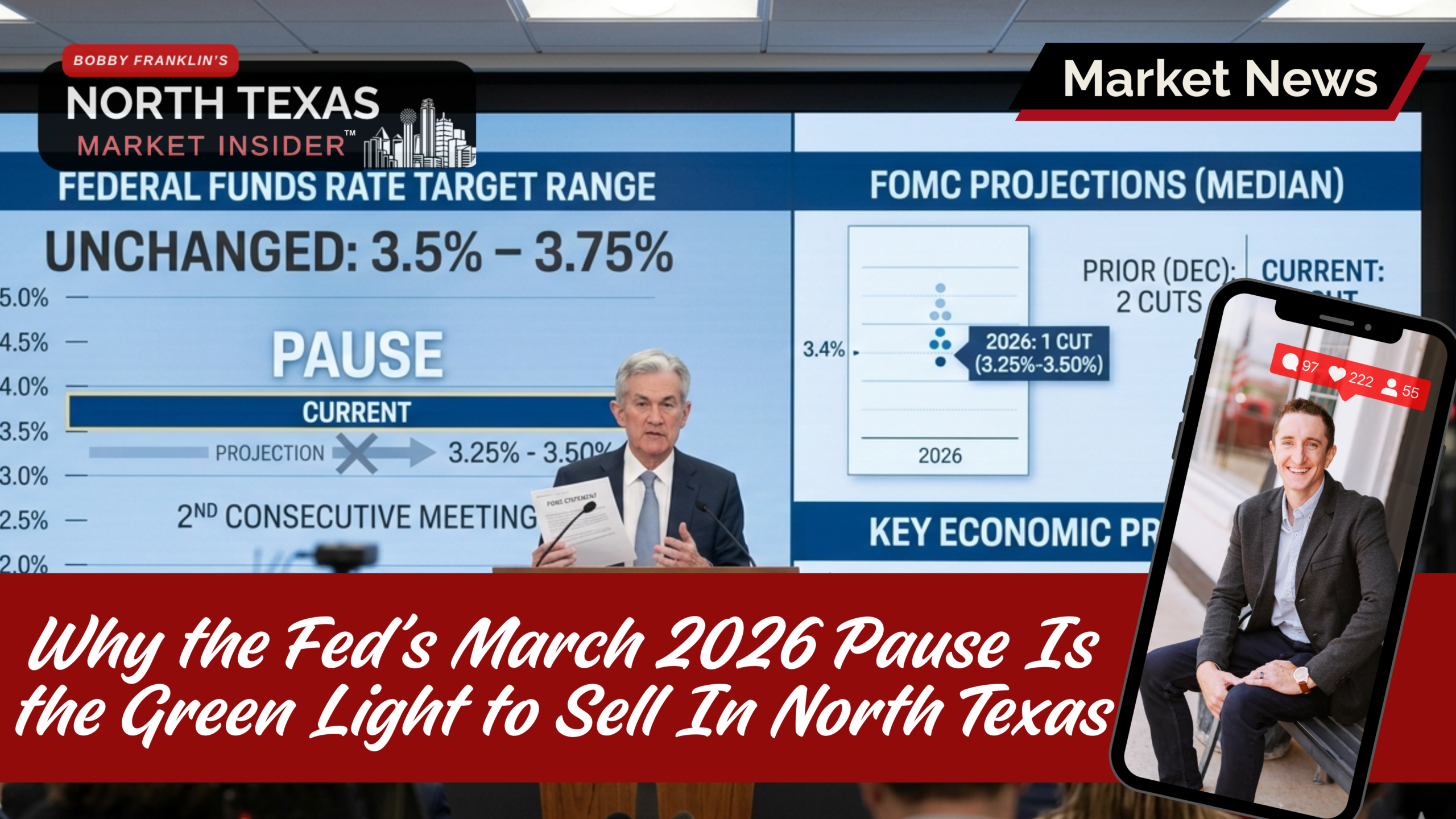

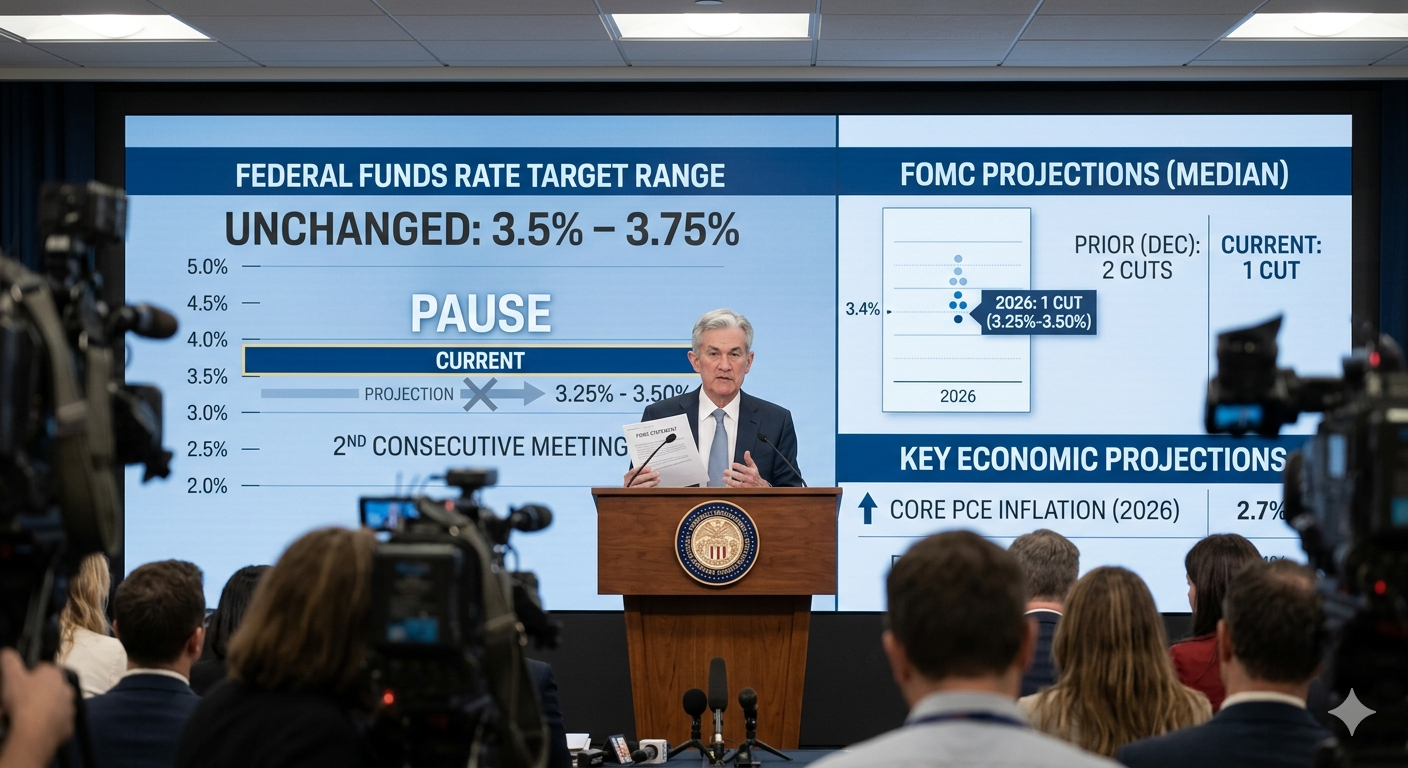

The Federal Reserve kept the federal funds rate in a target range of 3.5% to 3.75% at its March 2026 meeting. This was not a cut. It was not a hike. It was a deliberate pause, the Fed signaling that it wants to see more data before making another move.

Here’s what I need you to understand: the Fed does not set your mortgage rate. Let that sink in. The federal funds rate is what banks charge each other for overnight loans. Your 30-year fixed mortgage is priced off the 10-year Treasury yield, which moves based on bond market expectations, inflation data, and investor sentiment. The Fed influences all of that indirectly, powerfully, but indirectly.

What the March 2026 pause actually does is remove uncertainty. And uncertainty is the real enemy of real estate transactions.

When buyers believe rates might spike again next month, they freeze. When sellers think the market might shift dramatically in 90 days, they wait. But when the Fed telegraphs a stable, predictable rate environment, both sides of the transaction gain the confidence to move, not because the numbers changed dramatically, but because the fog cleared.

Most forecasters now expect 30-year fixed mortgage rates to float between 6.0% and 6.3% for the bulk of 2026. That’s higher than the pandemic lows. It’s also almost exactly in line with the long-term historical average going back 50 years. The buyers who understand that are already back in the market. The sellers who understand that are already positioning their homes.

The question is whether you’re one of them.

North Texas Is Not Playing by National Rules And That’s Your Advantage

Let me give you the national picture first, because you’re going to see these numbers everywhere and I want you to know how to read them.

Major forecasting platforms, Realtor.com, Redfin, Zillow, are projecting national home price growth somewhere in the range of 1% to 4% for 2026. Realtor.com specifically has penciled in mortgage rates near 6.3% and national price appreciation around 2.2%. That’s a far cry from the double-digit gains we saw in 2021 and 2022, and the market has largely already priced that in.

But North Texas is not a national average. It never has been.

DFW is projected to see price growth around 1.8% this year, with inventory moving toward, but still remaining below, pre-pandemic levels. Fort Worth is approaching a balanced market at roughly 3.9 months of supply, with median prices in the mid-$300,000s holding firm.

What does that combination actually mean for a seller? It means the panic-driven fire sale scenario is off the table. It also means the chaos of 2021, where you listed on Friday and had 40 offers by Sunday, is off the table too. What you have instead is a functional market where well-priced, well-marketed homes move at solid prices, with real buyers who are genuinely qualified and genuinely motivated.

That’s not a consolation prize. That’s a strategic operating environment.

For a comprehensive look at where prices are headed across Ellis County and the broader Metroplex, the full 2026 North Texas Housing Market Forecast breaks it all down.

The “High-Rate, High-Price” Market and Why North Texas Sellers Should Be Smiling

J.P. Morgan and several other major institutional analysts have described 2026 as a “high-price, high-rate” market, meaning elevated mortgage rates stay above 6%, but national prices flatten rather than collapse.

Here’s the strategic read that most agents won’t give you: that framing is actually good news for serious sellers.

Why? Because elevated rates act as a natural filter on the buyer pool. The speculative buyers, the people who were throwing offers on anything that moved in 2021 with the mentality of “I’ll flip it in 18 months”, those buyers are largely gone. What remains is a pool of buyers who genuinely need to move. Job relocations. Growing families. Retirement decisions. People who have done the math and determined that the right home at today’s rates still beats renting indefinitely or continuing to live in a space that no longer fits their life.

Those are the buyers who show up to showings prepared. Those are the buyers who don’t back out over minor inspection items. Those are the buyers who actually close.

Meanwhile, the national housing deficit, still estimated at roughly 1.2 million units, means meaningful oversupply isn’t coming anytime soon. The structural shortage that has defined this market since 2020 doesn’t evaporate because the Fed holds rates. It persists because building the inventory needed to satisfy demand takes years, not months.

The result for North Texas sellers in 2026: you’re not getting 2021 prices, and you’re not taking 2009 prices either. You’re operating in a stable, defensible market where strategic execution, pricing, marketing and timing are the variables that determines whether you win or leave money on the table.

Why Ellis County and the Southern DFW Corridor Are in a Class of Their Own

I want to spend real time here because this is where I live, where I work, and where I have data that nobody else is tracking at this level.

Ellis County, Waxahachie, Midlothian, Red Oak, Ennis, and the broader southern DFW corridor sit at a unique intersection in 2026. Median prices here remain meaningfully lower than Collin County, the Park Cities, or many northern suburbs. But the infrastructure story, the job growth story, and the demographic story are all pointing in the same direction… up.

The commute corridors into Dallas and Fort Worth are improving. School districts across Ellis County continue to attract families who want quality education without Allen ISD or Frisco ISD pricing. New construction is active, builders like Centre Living, Bloomfield Homes, Highland Homes, John Houston Homes, Graham Hart, and 8th & Main are all working in this market, but the resale inventory hasn’t caught up to demand at every price point.

Then there’s the development pipeline. The planned 5,200-acre South Creek Ranch project in Ferris represents the kind of catalyst that reshapes a submarket’s value trajectory. When major master-planned developments come online, bringing infrastructure, retail, employment, and a fresh wave of new residents, they don’t just benefit new construction, they lift the entire surrounding area. Existing homeowners who positioned themselves before that wave are the ones who capture the appreciation premium.

I’ll say it plainly: if you own in Ferris, in Ennis, or in the southern corridor between Dallas and Waxahachie, 2026 is not a “wait and see” moment. It’s a “decide before the market decides for you” moment.

For detailed city-level intelligence on what’s happening in your specific submarket, dig into the full 2026 forecast here.

Why DFW Continues to Outperform | The Fundamentals Nobody Is Questioning

Dallas-Fort Worth has ranked at or near the top of national emerging trends in real estate reports for years. That’s not an accident. It’s not momentum. It’s structure.

Job growth across finance, healthcare, logistics, and technology continues to bring major employers and their workforces into the region. The DFW economy does not depend on a single industry, which means it doesn’t collapse when any single sector hits a rough patch.

Population growth is being driven by both domestic migration and international immigration, which means new household formation is happening constantly. People need places to live. They’re moving here because Texas has no state income tax, because the cost of living relative to California, Colorado, Utah, and Arizona is dramatically lower, and because the job market here is genuinely one of the strongest in the country.

That steady inflow of buyers especially relocation buyers from the West Coast and Mountain West, is a primary reason DFW inventory remains tighter and prices more resilient than in markets like Austin or Houston, which over-built and are experiencing real correction pressure.

North Texas is not experiencing a correction. It is experiencing a normalization. There’s a significant difference.

The Lock-In Effect Is Thawing And That Changes Everything for Both Sides

For the last two years, the conversation in this market kept coming back to one thing: the lock-in effect. Homeowners who refinanced into 3% mortgages in 2020 and 2021 were psychologically, and financially, anchored to those rates. Moving meant trading a $1,400 monthly payment for a $2,200 monthly payment on the same dollar amount of home. For millions of homeowners, the math simply didn’t support moving, regardless of what life circumstances were evolving around them.

That’s changing in 2026. Not because rates dropped dramatically, they haven’t. But because life circumstances eventually override spreadsheet math.

New jobs happen. Families expand. Marriages end. Parents need care. Retirement decisions get made. The people who were frozen in 2023 and 2024 are starting to move in 2026, because the alternative, staying in a home that no longer fits their life while waiting for a rate that may never arrive, has become more costly than the rate differential itself.

Economists have been tracking this shift, and the data shows inventory gradually increasing as these “thawing” sellers enter the market. Here’s the strategic opportunity embedded in that trend: these sellers are entering a market that hasn’t yet been flooded with their supply. The equilibrium hasn’t been disrupted. You can still sell into a market where demand is meeting supply at a reasonable balance, before any significant surge in inventory tips the leverage back toward buyers.

If you’ve been waiting for the lock-in to lift as your signal to move, understand that the lift is already happening. You’re not ahead of the curve anymore. But you’re not behind it either. You have a window, and windows have a way of closing.

For a strategic framework on how to use your existing equity to execute a move-up or relocation in 2026’s balanced market, the full analysis is here.

Who Should Strongly Consider Listing in 2026

Let me be direct. Not everyone should sell right now. The Insider take is never “sell because the market is good.” It’s always “sell because your situation and the market align strategically.” Here’s who that is in 2026:

If you purchased before 2020 and your home no longer fits your life, you are sitting on equity that represents a genuine financial opportunity. The gap between what you owe and what you can sell for is real, and in 2026’s market, that equity gives you significant negotiating power on your next purchase, including the ability to make larger down payments that materially reduce the impact of a 6%-plus mortgage rate.

If you need to relocate for work, the math on waiting is often brutal. Every month you delay a relocation decision for “better rates” is a month of career opportunity cost, temporary housing expense, or dual-housing carrying costs. Execute the move, lock in today’s price, and refinance when rates drop, which every credible forecaster expects will eventually happen.

If you’re an investor holding property that no longer cash-flows at today’s tax and insurance levels, 2026 gives you an exit that doesn’t require a distressed sale. Prices are stable. Buyers exist at the right price point. The ability to re-deploy capital into higher-yield opportunities exists. Don’t let sentimental attachment to an asset turn a strategic decision into an emotional one.

If your family’s needs have outgrown your current home — school district access, home office space, proximity to aging parents, lifestyle changes, the cost of the “wrong house” compounds every year you stay. The rate environment matters. But so does living in a home that actually serves your life.

Who should NOT list right now: if you locked in below 3% recently, your home still fits your needs comfortably, and you have no financial pressure or life-event driving a move, there’s no urgency. Sit on your asset. Let the equity compound. The market will evolve, and your position will evolve with it.

For investors specifically, there’s detailed analysis of how current rates and inventory are affecting starter-home and rental dynamics in this market.

How to Execute a Listing Strategy in 2026’s Market – No 2021 Nostalgia Allowed

This is where agents get their clients into trouble. They anchor to what worked in 2021, price high, minimal marketing, take the first offer and they walk into 2026 with that same strategy. It fails every time. Here’s what actually works.

Price to sell in 30 to 45 days based on real comps. Not what your neighbor thought their house was worth in April 2022. Not the Zestimate that’s still inflated from pandemic-era algorithms. Real comps from the last 60 to 90 days in your specific zip code, adjusted for condition and features. If you price right, you attract serious buyers, generate real showing activity, and often end up at or above list anyway because legitimate competition forms naturally. Overprice, and you sit. Remember, days on market tells a story that compounds against you.

Marketing that goes beyond the MLS. In 2026, listing on MLS and praying is not a strategy. Professional photography is the entry point, not a differentiator. What moves homes in this market is hyperlocal digital targeting. Reaching the relocation buyers in California, Colorado, Utah, and Arizona who are already researching Ellis County before they’ve ever set foot in Texas. It’s creating content that tells the story of your neighborhood, your school district, your commute corridor in a way that makes a buyer in Denver feel like they already understand why Waxahachie or Midlothian is their answer.

Build a coordinated buy-sell plan before you list. The number one fear sellers have in 2026 is being homeless, selling their home and not having a landing pad for their next purchase. The solution is logistics, not luck. Extended closing timelines. Leaseback agreements that let you stay in your home after closing while your next purchase closes. Pre-approval letters that position you as a credible buyer even while you’re simultaneously a seller. The agents who can orchestrate that complexity are the ones worth hiring.

Leverage a balanced market’s negotiating tools. In 2021, buyers were waiving inspections, waiving appraisals, and throwing everything at sellers. The pendulum has moved. In 2026, sellers can negotiate concessions, rate buydowns, and flexible terms that simply weren’t available two years ago. A well-executed listing strategy includes knowing exactly which tools are on the table and how to use them to close the right buyer at the right number.

Browse current listings and marketing approaches at North Texas Market Insider to get a feel for how a data-driven listing strategy looks in practice in Ellis County and across the DFW Metroplex.

Your Lender Strategy Matters as Much as Your Listing Strategy

Here’s something most real estate content never tells you: who you choose as your lender has a direct impact on whether your transaction closes cleanly and on time. In a 2026 market where every day of carry costs money, that matters.

I work with three lender partners who operate at a level I can stake my reputation on and I’m required by RESPA to tell you that these are affiliated relationships that I disclose fully, and you are absolutely free to choose any lender you prefer. I do not receive anything from these referrals other than solid, well executed closings.

Denise Donoghue — The Mortgage Nerd brings a depth of product knowledge and borrower education that I’ve seen get complex transactions across the finish line when others would have fallen apart.

Andrew Bryan — Miramar Mortgage specializes in the kind of creative structuring like buy-down strategies, portfolio products and bridge loan scenarios. That becomes relevant when you’re executing a simultaneous buy-sell in today’s market.

Ethan Hester — Midtex Mortgage knows this specific corridor – Ellis County, southern DFW, the markets I serve daily. His reputation goes a long way when agents see his name on the pre-approval letter.

Talk to all three. Ask about rate buydown programs, about bridge financing, about what products make the most sense given your equity position and your timeline. The right lender for your transaction is the one whose product and communication style fit your situation and you’ll never know that without having the conversation.

A Word on How I Operate: Fair Housing, RESPA, and the 2026 NAR Landscape

I’m a REALTOR®, which means I operate under a Code of Ethics that goes beyond what the law requires. In 2026, with the NAR settlement changes still rippling through the industry, I think it’s worth being explicit about how I work.

Fair Housing is non-negotiable. Every recommendation I make on pricing, neighborhood analysis, buyer targeting and marketing approach is grounded in objective market data. I focus on features, condition, pricing, comparable sales and demographic trends. Never protected class characteristics. The Fair Housing Act prohibits discrimination based on race, color, religion, sex, disability, familial status, or national origin, and every piece of content and every client conversation I produce respects that absolutely.

RESPA means full disclosure, always. My lender partners are disclosed to you in writing. My affiliated relationships are transparent. You are never obligated to use any service provider I recommend — my job is to give you options and explain the trade-offs, not to steer you toward a kickback that benefits me at your expense. That’s not how I operate, and it’s not legal anyway.

The NAR settlement changes buyer-broker compensation transparency. As your listing agent, I will review your listing agreement with you line by line. You will understand exactly how cooperating buyer’s agents are being compensated, whether you’re offering any concessions toward buyer-side representation, and what your net proceeds look like under each scenario. No surprises. No fine print that changes the math after you’ve already committed.

TREC advertising rules govern everything I publish. My brokerage information – Legacy Realty Group, Leslie Majors Team – is clearly identified in all marketing materials. Performance claims are grounded in verifiable data. Every article and piece of content on North Texas Market Insider is original, written specifically for this market, and produced to give you actionable intelligence, not to hit search rankings with generic template content.

The Questions Everyone Is Actually Googling

Does the Fed holding rates steady actually lower my mortgage rate?

No, not directly. The federal funds rate influences bond markets, which influence mortgage pricing, but they don’t move in lockstep. What a stable Fed does is remove the volatility premium that spikes rates when investors are uncertain. In 2026, most forecasts have 30-year fixed rates floating between 6.0% and 6.3%, which is close to the long-term historical average regardless of what the Fed does next.

Is it a bad time to sell in North Texas because rates are still high?

No. Rates above 6% are historically normal, and the North Texas market has already absorbed and priced in that reality. You’re not selling into a 2009 market. You’re selling into one of the top-ranked housing markets in the country, with tight inventory, modest appreciation, and a steady inflow of relocation buyers from higher-cost states who view North Texas as a relative bargain even at today’s rates.

Will prices finally drop if the Fed doesn’t cut more?

No major forecaster is projecting a national price crash in 2026. The structural housing deficit which sits at an estimated 1.2 million units nationally, is the floor under prices. You don’t get a broad collapse when supply is still below pre-pandemic levels and household formation is still positive. DFW specifically is projected for mild appreciation and a transition toward balance, not reversal into deep discount territory.

I have a 3% mortgage. Does it ever make sense to move when rates are over 6%?

Yes, when life circumstances make staying more costly than moving. Your equity position matters. If you purchased before 2020, you may have enough equity to make a meaningful down payment on your next home, offsetting a significant portion of the rate differential. And in 2026’s balanced market, sellers can negotiate concessions, rate buydowns, and extended timelines that weren’t available in 2021 — tools that change the real cost-of-move calculation.

Should I wait for rates to drop below 5% before I sell or buy?

I’d strongly caution against building your entire strategy around a rate target that may not materialize on your timeline. Every major housing analyst has rates above 6% for the bulk of 2026. Meanwhile, waiting means continued rent payments, missed appreciation, delayed equity building, and the risk that when rates do drop, demand surges and the negotiating leverage you have right now as a buyer evaporates. For many households, the opportunity cost of waiting is larger than the savings they’re hoping for.

How does the 2026 market specifically affect sellers in Ellis County?

Ellis County is positioned for gradual inventory growth, stable-to-rising prices, and long-term catalysts that will materially affect value trajectories in the southern corridor. Because prices here remain lower than Collin County and many northern suburbs, buyer demand from value-conscious relocators stays strong. Well-located homes in Waxahachie, Midlothian, Red Oak, and Ennis are not sitting. They’re moving. See the neighborhood-level breakdown in the 2026 intelligence report.

Are investors still buying single-family homes with rates this high?

Yes, but the strategy has shifted, not disappeared. Large institutions have moved toward cash-flow-focused approaches rather than aggressive appreciation bets. Research from 2025 shows that investors created significantly more starter-home inventory by renovating existing stock than builders did through new construction. If your home fits the investor buy-box aka starter-home price point, solid location and manageable repairs, there’s a viable buyer segment beyond traditional owner-occupants. Full analysis here.

Is using AI to sell my house a real strategy in 2026?

AI tools are genuinely useful for marketing ideation, listing description drafts, and market data analysis. They are not licensed professionals. They cannot replace a fiduciary relationship, a pricing strategy grounded in real local comps, or the negotiation skills that protect your net proceeds when a deal gets complicated. The right answer is both: AI-assisted marketing combined with an agent who knows your specific market at a level no algorithm has yet replicated. For a full breakdown of where AI helps and where it fails in real estate, read this.

The Bottom Line: 2026 Is a “Plan Your Move” Market Not a “Wait for the Crash” Market

Here’s my Insider take, and I’m going to give it to you straight because that’s the only way this works.

The Federal Reserve’s March 2026 decision to hold rates steady did not create a market emergency. It created a market opportunity for the prepared. Buyers are gaining confidence. The lock-in effect is thawing. North Texas continues to attract population, employers, and investment at a pace that insulates it from the kind of inventory collapse that triggers real price declines. And the sellers who understand all of that, who make decisions based on intelligence rather than fear or nostalgia, are the ones who are going to execute strong transactions in 2026.

The sellers who are going to struggle are the ones waiting for the conditions of 2021 to return. Those conditions were an anomaly. They are not returning on any timeline that serves your goals. Meanwhile, the window you have right now, the one before the lock-in thaw floods the market with competing inventory, before South Creek Ranch and other major developments shift the supply equation in the southern corridor, before the next wave of rate uncertainty potentially tightens buyer psychology again… that window is real, and it is finite.

I track these markets every day. Permit filings. Demographic inflows. Builder incentive packages. MLS absorption rates. Census data. Fed policy implications at the neighborhood level. That is what separates intelligence from noise, and it’s what I bring to every listing and every consultation I do in North Texas.

If you’re thinking about selling in 2026 and want a data-backed pricing and timing strategy specific to your address, down to school-district trends, infrastructure pipeline, and buyer demand in your micro-neighborhood, let’s have that conversation. Reach me directly at 214-228-0003 or schedule a consultation.

You can also explore additional resources that inform smart decisions in this market:

- Tiny Homes vs. Manufactured Homes in North Texas

- How Elevation Surveys Can Save You From a Bad Foundation

- Can ChatGPT Really Sell Your Home?

The information in this article is provided for educational and informational purposes only and does not constitute legal, financial, or investment advice. All real estate transactions should be conducted in accordance with applicable federal and state laws, including the Fair Housing Act, RESPA, the NAR Code of Ethics, and TREC advertising standards. Compensation arrangements are always negotiable. Affiliated lender relationships are disclosed as required by law; consumers are under no obligation to use any referred service provider. Market data and projections referenced herein are sourced from publicly available forecasts and local MLS data and are subject to change.

Bobby Franklin, REALTOR® | Legacy Realty Group – Leslie Majors Team | 📲 214-228-0003 | northtexasmarketinsider.com

Join The Discussion